5 Items To Know When Buying A House With Student Loans

In This Episode:

The dream of many, as well as the most common way for Americans to build wealth, is buying a home. That is becoming more and more of a dream for those graduating with massive student loan debt. This podcast discusses buying a house with student loan debt.

If you have student loans and are planning to buy a house, in the process, or have been denied a mortgage then this podcast is for you.

Topics In This Episode

- Why Its Hard To Get Help & Where To Get It

- Buying A House With Student Loan Debt: The Major Problem

- Not All Student Loans Are Treated Equal

- Buying A House When Using A Pay Off Strategy For Your Student Loans

- Buying A House When Using A Loan Forgiveness Strategy For Your Student Loans (IBR, PAYE, REPAYE, PSLF)

Why Its Hard To Get Help & Where To Get It

Big Box lenders and their employees often times make it really hard to get a loan. By "Big Box" I'm referring to lenders such as Bank Of America, Wells Fargo, etc...

Its hard to get a mortgage with these companies when you have student loans because these businesses process hundreds of thousands, if not millions of applications per year. They have cookie cutter models to determine if you qualify for a loan or not.

Simply put, they collect your data, plug it into a software, and an answer is spit out. When you get declined its hard for you to figure out how to get approved because 1) the employees are so busy processing applications they just want to move on to the next borrower (i.e. the "low hanging fruit" that is easy to get qualified) and 2) they aren't trained on things like student loans.

Therefore, they have no way of trying to help you manipulate the data to qualify (below in this article we discuss ways to manipulate numbers).

The solution, find a mortgage broker in your state that knows what they are doing. They are out there, you just have to dig a little bit.

High Student Debt and Buying A House: The Major Problem

According to CNBC, 83% of people ages 22-35 who haven’t bought a home blame their student loans. Due to student loans, many can’t qualify for a home loan. However, they don't know why.

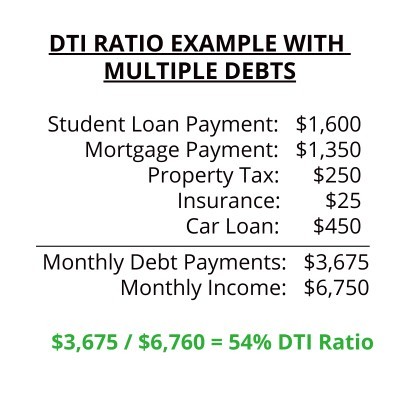

There are three primary items that determine qualifications for a mortgage: Credit (your FICO Score), LTV ratio (Loan-To-Value or how much mortgage you apply for relative to the value of the home), and your DTI ratio (Debt-To-Income).

The primary reason we see student loan borrowers not qualify for a mortgage is their debt-to-income ratio (DTI). Below is an example of why that is. Later in the article I explain a way to potentially help you qualify for a mortgage by “optimizing” your DTI ratio.

First things first though, what is DTI. It is your total debt obligation divided by total gross earnings. By total we mean all monthly payments on all debt... Student loans, auto loans, credit cards, etc... When you are buying a home, the lender includes the mortgage payment, property tax, home owners insurance and HOAs into this calculation.

To qualify for a mortgage your DTI ratio can not be more than 45% - 55%. Below is an example that illustrates the DTI calculation.

A Grad School Example

An individual with a graduate degree used to be an automatic to qualify for a mortgage. However, that has changed due to student loans.

For the following example, we will use actual data we have collected from FitBUX members.

Let’s assume a recent graduate is making $70,000 a year (i.e. $5,833/months). The graduate has $145,000 in student debt. Their monthly required payment under the standard 10 year student loan repayment plan $1,632. Let’s also assume that she has no other debt or source of income.

Her DTI ratio would then be 28% ($1,632/$5,833).

Let’s say she wants to buy the home of her dreams. We’ll assume lenders will not let our new graduate have a DTI ratio greater than 45%.

This means that her home mortgage, taxes, homeowners insurance, PMI, and HOA fees must be 17% of her income or less. (45%-28%= 17%).

Let's assume that she would use the full 17% just for her mortgage. Thus, 17% of her $70,000 salary is $11,900 per year. Therefore, the max her mortgage payment can be is $991 per month.

Assuming a 30-year mortgage (Principal and Interest) at 5%, she would only qualify for a mortgage of $185,000. Once you account for property taxes and homeowners insurance, that number will be even less of course.

Not All Student Loan Repayment Plans Are Treated Equal

Above I mention that Big Box Lenders aren't trained in student loans. Many mortgage brokers are not either which is why it may take you time to find one.

This is important because not all student loan plans are treated equally when you are trying to qualify for a mortgage. To simplify student loan plans at FitBUX, our student loan planners break them down into two strategies: Pay Off Strategies and Loan Forgiveness Strategies.

It is extremely important to know the differences between the two because they will greatly influence your DTI ratio.

In the next sections I will break down how to qualify for a mortgage for both strategies.

Buying A House When Using A Pay Off Strategy For Your Student Loans

You may “feel” that you can afford more house. Unfortunately, your lender won’t take your “feelings” into consideration. All they care about is what the "numbers" are so... let's figure out how to manipulate your "numbers."

One way to make your "numbers" look better is to reduce your required monthly payment on your student loan. You can do this by using the extended standard repayment plan on your Federal loans.

Taking the above actions will decrease your required monthly payment since you’ll be paying off your loans over a longer period of time.

Note: Using The extended standard repayment plan for Federal Loans would give you the same interest rate.

Using the same example in the previous section, extending all loans to 25 years while keeping the same interest rate would reduce the total required payment from $1,632 down to $962.

The new DTI ratio would then be 16% ($962/$5,833), with 29% available to secure a mortgage. All else being equal, our recent graduate would now qualify for a mortgage of $315,000.

One extra thing you can do is refinance your high interest rate loans into a 20 year private loan to save money and drop your required payment further.

If you have private loans, you can try refinancing them into a longer term (If you need help refinancing your student loans, check our our free student loan refinance service).

In short, the more you reduce your required monthly payment on your student loans, the easier it is to qualify for a mortgage and the more you can qualify for!

Bad News, Good news

One thing to keep in mind when considering extending loans is you could end up making payments for a long-time. Therefore, you end up repaying a lot more overall due to the longer term.

That’s the bad news. To neutralize this, it is important to build a strategy where you will make additional prepayments. This will help you repay your loans faster and pay less interest.

Buying A House When Using A Loan Forgiveness Strategy For Your Student Loans

First things first, the government classifies income-based repayment plans (IBR), pay as you earn (PAYE), revised pay as you earn (REPAYE), and public service loan forgiveness (PSLF) as loan forgiveness plans. Therefore, these are the strategies I'll be discussing in this section.

There are a few keys you need to know before dive deeper:

- You must know how Income-Driven Repayment plans work. Check out our IDR Guide to get a good understanding of these plans.

- The following discussion is about Fannie Mae, Freddie Mac, and FHA loans.

- The official language for mortgage qualifications refer to these as "Non-amortizing" student loans. This is key as it is different than "deferment" and "forbearance" (I discuss in detail below).

Your required payment on a student loan forgiveness strategy is based as percentage of your income. This required payment is then reported to the credit bureaus and is used in the DTI calculation for your mortgage qualification....sometimes.

FHA Loans do not use this payment. Instead they assume your monthly payment is 1% of your loan balance. For example, if I have a $300 monthly payment but my loan balance is $140,000, then for the purpose of my DTI calculation for the mortgage, the lender will use $1,400 as an assumed monthly payment.

The result is that I qualify for about $170,000 less in a mortgage than I would have if they used my actual payment. For example, had they used $300 as my required payment, I would qualify for a $300,000 mortgage. Since they use $1,400 instead, I only qualify for a mortgage of $130,000!

One trick would be to switch to a pay off strategy and use an extended 25 year student loan repayment option in the short-run. Once you have your mortgage, you can switch back to loan forgiveness.

One problem with this short-term strategy though. Once you switch the accrued interest is capitalized, i.e. it begins to compound interest on top of interest. Therefore, I highly suggest speaking with your FitBUX Coach to figure out if this is right for you or not.

For Fannie Mae and Freddie Mac, the required payment for your student loans is always used in the DTI calculation for your mortgage. This means if your student loan payment is $300 per month, they use amount for the DTI calculation.

But this is where they caveat comes in....Many people have a $0 required payment for their student loans because they just graduated, forbearance, or because of COVID. You have to differentiate between a $0 required payment and deferment/forbearance.

If you have a $0 monthly payment, then for Fannie Mae and Freddie Mac mortgages, the $0 payment will be used in the DTI ratio. When you are in deferment (such as being in your grace period) or in forbearance, you also have $0 due each month. HOWEVER, THIS IS DIFFERENT THAN HAVING A $0 REQUIRED PAYMENT. Because you are in deferment or forbearance, Fannie Mae and Freddie Mac will take 0.50% of your loan balance and assume that is your required monthly payment.

For example, if your loan balance is $140,000 then your assumed monthly payment for the DTI calculation will be $700.

The easy solution for people would be to apply for a Fannie Mae and Freddie Mac loan. However, its not that simple... These mortgage programs require much higher down payments than the FHA loan program.

Conclusion

To sum it up, if you are using a pay off strategy for your student loans, home buying is more straight forward. Try to reduce your required payment and it will be easier to qualify.

If you are on a loan forgiveness student loan strategy, there is more leg work you have to do in order to qualify.

Resources Discussed In The Episode

Resources Discussed In The Episode

Watch The Video Version Below

Podcast Episodes You May Like

FitBUX, Inc. is helping Young Professionals manage and eliminate over $950 million in student loan debt. We're on a mission to help everyone manage their money smarter!

Copyright © 2015 - 2021 Fitbux, Inc.