We’ve helped new grads manage and eliminate over $1.4 billion in student loans and one topic that always stirs up a lot of confusion is Pay As You Earn (PAYE) and Revised Pay As You Earn (REPAYE).

If you try to go to the governments site, things get confusing very fast. President Biden also recently announced revisions to REPAYE that make them even more confusing.

Therefore, to make the two choices easy to understand, I break down the 5 primary differences in this article so you can compare PAYE vs REPAYE.

I’ve also included the revision President Biden announced. They aren’t law yet but they have a good chance of becoming law.

Also, I’ve included a suggestion for when you should use PAYE vs REPAYE.

Note: The Biden administration announced that REPAYE is no longer going to be an option. Instead the new plan will be called SAVE. Therefore, you should read our guide on the NEW Save Student Loan Repayment Plan and compare it against PAYE/IBR.

Summary Of Similarities

Before diving into the differences, let’s briefly summarize the similarities between PAYE and REPAYE:

- Both are income-driven student loan repayment plans;

- Your payments are capped at 10% of your discretionary income (One of Biden’s revisions to REPAYE is to decrease this to 5% for undergrad loans);

- They only apply to Federal student loans;

- Each forgives the amount you owe after a given period of time; and

- For both PAYE and REPAYE, the forgiven amount is treated as regular income and taxed as such.

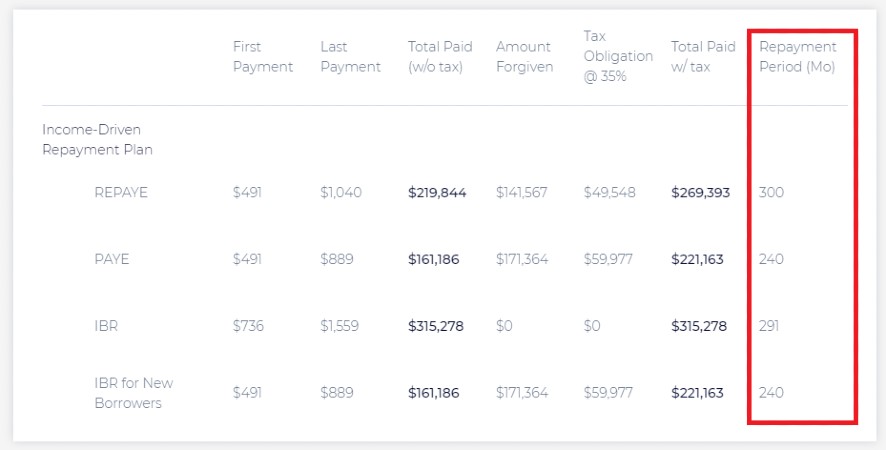

Below is a summary comparison chart:

Note: If you are using either of these strategies, you do not want to refinance your student loans. If you do, then you will not qualify to use these plans.

Difference #1: Term

PAYE is 20 years long for both undergrad and graduate loans. This means if you are on this plan for 20 years, all loans are forgiven and the remaining balance is taxed.

REPAYE is 20 years long if you only have undergraduate loans. If any of your loans are from graduate school, the term is 25 years. This would apply to all your loans, i.e. your undergrad and graduate school loans would be on a 25 year term.

This is an extremely important when comparing PAYE vs REPAYE because the extra 5 years can cost you a lot. I will discuss the cost later on in the article.

Below is a screen shot of our Income-based repayment calculator that automatically detects if your loan term is 20 or 25 years based on how you complete your profile.

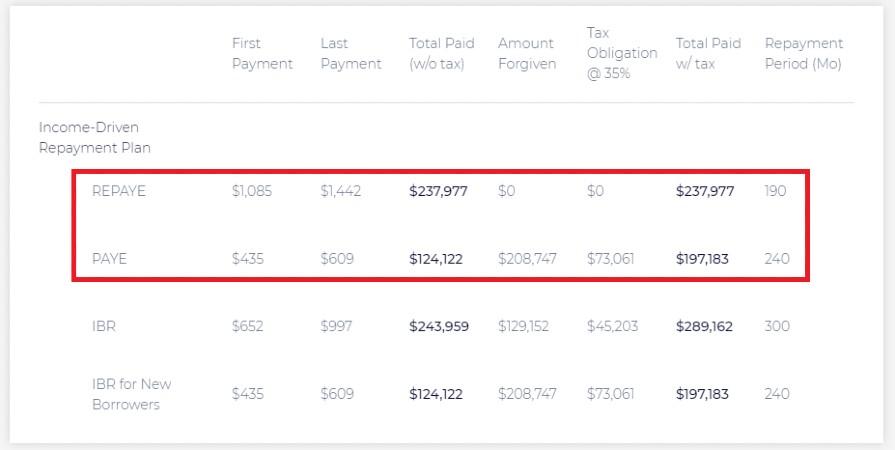

Difference #2: Marriage

When you are married, you may choose to file your taxes separately or jointly.

If you are on PAYE and file separately, then your monthly payment is only based on your income and your amount of Federal loans. If you file jointly however, your monthly payment is based on your combined income and Federal loans.

On REPAYE, currently your tax filing status doesn’t matter. When you are married, your required payments are based on your combined incomes and Federal debt levels.

When deciding on PAYE vs REPAYE, taking into account your spouses’ or future spouses’ financial situation is a must. We often see people who know they are going to get married within a year or two. However, they fail to take into account their spouses’ financial situation. Such a mistake may cost a couple thousands of dollars over time.

In the following example, I assume I’m making $78,000 per year and my spouse is also making that much. As you can see, having to take into account my spouses’ income could cost me an additional $40,000 using REPAYE vs using PAYE.

My monthly payment more than doubles using REPAYE. This would also happen on PAYE if I filed my taxes jointly. However, PAYE gives me the choice whereas REPAYE does not.

The exact amount your monthly payment increases also factors in how much Federal Student loan debt your spouse has. The calculation is complex but for those you you that want to deeper dive into it, here is a great article doing so.

Note: This is the way REPAYE currently works. Under Biden’s proposal, you’d be able to file separately and have your payment be based only on your income just like PAYE.

Difference #3: Interest Deferral

In our income-based repayment guide, we discuss how the difference between your interest charge and the required monthly payment is deferred onto the loan. Therefore, most will be deferring interest when they are on PAYE and REPAYE.

On PAYE, you defer 100% of the interest for unsubsidized loans. For subsidized loans, the government pays the deferred interest for you for 3 years. Thereafter, you defer 100% of the interest on subsidized loans as well.

On REPAYE, the government pays 100% of the deferred interest on subsidized loans for the first three years just like PAYE. However, the unsubsidized deferred interest is treated separately. This is referred to as the REPAYE interest subsidy.

On REPAYE the government pays 50% of the deferred interest each month for unsubsidized loans. After 3 years, they do the same for subsidized loans. (Biden’s proposal changes this to 100% no matter the type of loan or length of time)

To illustrate the difference of PAYE vs REPAYE, I’ll use the following example:

- Your interest charge is $700 per month,

- Your required monthly payment on both PAYE and REPAYE is $300 per month (if you need help figuring out what your payment would be check out our IDR calculator).

On PAYE you would differ $400 of interest per month ($700 – $300).

On REPAYE you would defer $200 because the government pays 50% of the deferred interest each month ($700 – $300 = $400 *.50 = $200).

You can take advantage of the REPAYE interest subsidy if you are paying off your loans. If you are interested in doing so, check out how to take advantage of the interest subsidy.

Difference #4: Capped Monthly Payments

On PAYE, your required monthly payments are capped. This cap is based on the original amount that you owed and what your payment would be on the Standard 10 year plan. Since the payments are capped, you must qualify for partial financial hardship to qualify for PAYE.

For example, if when you entered repayment your required payment would have been $1,000 on a standard 10 year plan, then that is the highest your monthly payment would be on PAYE. This holds true regardless of how high your income goes up.

On REPAYE there is no cap. Therefore, if your income increases significantly your monthly payments will as well.

This may have a significant impact for married couples. As we mentioned earlier, if you are married or you know you will be married relatively soon, you want to factor your spouse’s income and Federal student loan debt into the equation before deciding which plan to select.

Below is a summary of the first 4 differences between PAYE and REPAYE:

Difference #5: Calculating The Cost Difference Between PAYE and REPAYE

It is tricky to calculate the true cost difference between PAYE and REPAYE. The reason is one is a 20 year repayment plan the other is a 25 year plan. (Note: This problem only exists for Grad students. For undergrads they are both 20 year plans.)

Many are enticed to use REPAYE because of the 50% interest subsidy mentioned previously. However, because REPAYE is 5 years longer, it can become much more expensive when doing an “apple to apple” comparison. Not only does it cost you in regards to having to make a payment for an extra 60 months, you could be investing that money instead in retirement accounts such as 401(k)s and Roth IRAs. That is the true cost of REPAYE vs PAYE, i.e. the monthly payment plus how much you are giving up by not having that money to invest.

To see how to calculate the true cost difference be sure to check out our article detailing how to use our Income Driven Repayment Plan calculator.

PAYE vs REPAYE: How To Decide Which One To Use

Choosing PAYE vs REPAYE can be a hard decision to make.

Most of the time PAYE is the better option. It has a shorter term and cost less in the long-run. Most importantly, it also gives you options should you get married when it comes to selecting your tax filing status. The more options you give yourself financially the better you’ll be in the long-run.

This generalization may change if Biden’s REPAYE proposal is adopted into law. However, in our early simulations we are seeing that PAYE would still be a better option for graduate students because of the extra 5 years of payments.

Lastly, if you are pursuing PSLF, you should definitely try to use PAYE.

However, unlike above, if the new REPAYE revisions go into law and you are pursuing PSLF then REPAYE would most likely be the best option. For more information as to why, be sure to read our Public Service Loan Forgiveness guide.

When Would REPAYE Be Better?

There are 3 specific circumstances were REPAYE has a major advantage:

- If you are only going to be using a loan forgiveness plan in the short-run:

- Even if you’re paying off your loans, you may find yourself in a situation where you need to use an IDR plan temporarily to benefit from lower monthly payments. For example, you may be doing a residency or may be on maternity leave and only need short-term payment relief. Then once your income increases you plan on making aggressive payments and paying the loans off.

- In this situation, REPAYE would be a major benefit because the government is paying half the deferred interest while your income is low.

- If you can’t afford the recommended minimum tax savings amount on PAYE to cover your tax liability at the end of your IDR plan. Switching to REPAYE would extend the timeline from 20 to 25 years, you an extra 5 years to save.

- Are you pursuing public service loan forgiveness but might stop working at a non-profit then REPAYE may be the right choice for you. This would be the case if you stop working at the non-profit and know you’d choose to switch plans and pay off your loans. Make sure to consult our comprehensive PSLF Resource page to learn more.

Rapid Fire FAQ

Is PAYE or REPAYE Better?

A super majority of the time, PAYE is better because it cost less and gives you flexibility when you are married than can lower your monthly payment.

What is the difference between REPAYE & PAYE?

PAYE is 20 years for all borrowers and can have a lower monthly payment when you are married. REPAYE may be 25 years long and has an interest subsidy.

Can you switch from REPAYE to PAYE?

Yes. However, when you do so any interest that has accrued is capitalized which increases your tax liability when the loans are forgiven.

PAYE VS REPAYE Conclusion

As I mentioned previous, choosing PAYE vs REPAYE is a hard decision.

Its difficult because you have to consider the impact today, over the next few years, and long into the future. Think about it, this choice can have an impact on you 25 years from today!

If you need help deciding between PAYE and REPAYE, FitBUX is here for you. Our financial planning software is designed specifically to help young professionals make this decision as well as many others.

Plus, you can always schedule a call with one of our FitBUX Coaches and get your questions answered.

Wow thank you so much! This was so clear and I, for once, finished reading an article about student loans and felt LESS confused rather than more. Thank you!!

Glad to help out.