Part of my research as a CFA Charterholder is to examine ways to reduce risk to investment holdings and financial plans. Over my 20 years of experience, I’ve found that using a Roth IRA is on of the best vehicles to invest in because of the tax benefits and the flexible withdraw rules which reduce risk to financial plans.

I’m not the only one in the finance world that understands how effective Roth IRAs are. For those that are interested, here is a good summary from a study T-Rowe Price conducted on the effectiveness of Roth IRAs.

Many young professionals we work with do not know what a Roth IRA is when they graduate. Therefore, I wrote this Roth IRA guide that answers the top questions we receive about them from FitBUX Members.

For those of you that would like to listen to a great podcast on this topic, I’ve included our Roth IRA for beginners podcast below.

What Is A Roth IRA Account?

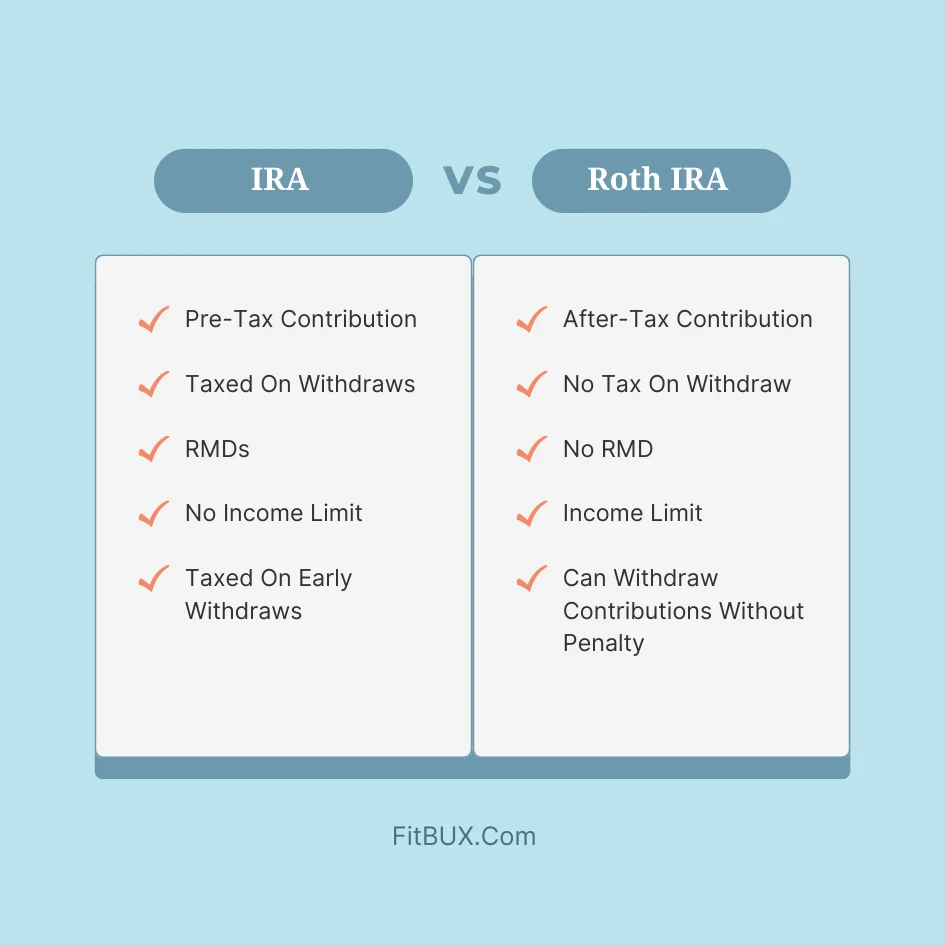

A Roth IRA is an individual retirement account. The money you put into is contributed after taxes, which means that you don’t get a tax deduction or tax credit in the year you contribute money to a Roth IRA account.

Then, while the account grows, you don’t pay taxes which means it is tax deferred. Once you reach 59.5 years old, you can withdraw the gains tax-free.

How Does A Roth IRA Differ From A Traditional IRA?

A Traditional IRA is made with pre-tax contributions which reduces your tax bill this year. However, when you take the money out in retirement you are taxed on the withdraw.

Traditional IRAs also force you to withdraw a required amount once you hit a certain age. This can lead to increased taxes at inopportune times. These mandatory withdraw is called a Required Minimum Distribution (RMD).

Roth IRAs do not have an RMD.

How Does A Roth IRA Work?

The biggest misunderstanding we see is people think a Roth IRA is an investment. It’s not. It is simply a holding account with a special tax treatment. Once you deposit money in a Roth IRA, you then have to decide how to invest it.

Should You Have A 401(k) and a Roth IRA?

If you can afford both and are eligible for both, then yes! At a minimum, if your employer offers a 401(k) with a match, you should contribute the amount needed to get 100% of your employer’s match. In addition, we recommend contributing $50 a month to a Roth IRA. This will provide you with retirement income diversification as each account has different tax benefits and may allow you to invest in different securities and other financial products.

Once you put the minimum into both accounts, it largely depends on your income as to which one makes since to contribute to. The key is to making this decision is by setting up your financial plan wisely. Check out this financial planning example to see how to do this.

Where To Open A Roth IRA?

There are 4 primary places to open a Roth IRA: RIAs, Robo Advisors, Do-It-Yourself, and a hybrid of the above.

1- RIAs are Registered Investment Advisors. RIAs typically charge you 1% – 2% of the assets you have invested with them and in my opinion don’t provide you the value you think you’re getting from those fees.

2- Robo Advisors are cheaper, typically .25% – .50%. Unfortunately, they only look at a subset of your financial picture which may leads to incorrect decisions.

3- Because of the costs of RIAs and the silo’ed approach of robo advisors, many end up taking matter into their own hands. This may be the cheapest way to invest in a ROTH IRA. However, it may also be the most time intensive.

How Much Should I Put In My Roth IRA?

Based on the FitBUX financial planning method, we recommend contributing at least $50 per month and using a dollar cost averaging approach to do so. The ultimate amount you should put in depends on your financial situation and your goals. The maximum you can put in as of 2024 is $7,000 a year and $8,000 if you are older than 50.

How Should I Contribute To My Roth IRA?

The best way to contribute is on a regular basis. This is referred to as Dollar Cost Averaging.

The more frequent you contribute the better. For example, contributing to your Roth IRA every two weeks when you receive your paycheck. You can also choose to do it monthly or annually. Most investment companies give you the ability to easily set up these contributions.

What I highly recommend not doing is to make a lump sum contribution one time then either never do it again or wait years before making another contribution.

Can I Withdraw My Roth IRA Contribution Without Penalty?

Roth IRAs have special features that other retirement accounts such as Traditional IRAs do not have. In most retirement accounts, if you take the money out before 59.5 years old you are penalized.

Roth IRAs have a special IRS tax law that says, you can take out the contribution anytime you’d like without penalties.

For example, if you contribute $5,000 a year for 4 years into your Roth IRA, you can access the $20,000 anytime you need to without penalty. This feature reduces risk to your financial plan and gives you flexibility. For example, this allows you to use the Roth IRA to save for the IDR tax bomb on student loans.

Also, you can take money out of your Roth IRA for other events as well. For example, you can withdraw $10,000 of gains without penalty if you use the money for a down payment on a house.

Note: There are certain limitations on withdrawing contributions from your Roth IRA based on various circumstances. This limitation is called the 5-year rule.

Are Roth IRAs Safe?

Most are asking this question because they are afraid of losing money on their investments. As stated earlier, a Roth IRA is not an investment but simply is an account that houses investments. Therefore, the risk comes from the different positions in this account. This is why our approach is so critical in order to understand and take a risk-based approach.

What Are The Income Limits For Contributing To A Roth IRA?

To contribute to a Roth IRA, single tax filers must have a modified adjusted gross income (MAGI) of less than $153,000 in 2023. In 2024, the threshold rises to $161,000. If married and filing jointly, your joint MAGI must be under $228,000 in 2023. In 2024, the threshold rises to $240,000.

Roth IRA For High-Income Earners

If you find yourself above the aforementioned income thresholds, don’t worry. You can still contribute to a Roth IRA. You just have to take a few extra steps.

This process is called a Back Door Roth IRA. I recommend checking out the link to learn more.

What Are Roth IRA Interest Rates?

Here again, a Roth IRA is simply a structure, not an investment and as such, do not pay interest. However, the investments that you hold within your IRA may pay interest.

What Are The Best Investment Options Within A Roth IRA?

You can invest in anything, i.e. stocks, bonds, ETFs, real estate, etc…

However, for most people the best way to invest is via ETF. ETFs combine a number of investments so you get the benefits of diversification, i.e. you lower your risk, and they are cheap.

What Are Roth IRA Contribution Limits In 2024?

Contributions are $7,000 a year per person. If you are older than 50 you can contribute $8,000 per year.

What Is A Roth IRA Conversion?

A Roth IRA conversion is the process by which you move funds from a Traditional IRA, 401k, 403b, or other qualified employer plan to a Roth IRA.

Because you will. have to pay income taxes when you convert to a Roth IRA, you will want to try and make the conversion in years where you have a low(er) income and therefore pay taxes at a lower rate (or better yet, don’t have to pay taxes at all).

One of the key advantage of a conversion is that while you pay taxes “up front”, you will enjoy tax-free withdrawals in retirement.

Also, a form of conversion maybe called a backdoor Roth IRA. If your income is high or you are married filing separately you’ll want to check those out.

What Is A Rollover Roth IRA?

If you have a Roth 401k with your old employer, you can roll it over to a Roth IRA. This is considered a rollover Roth IRA. Also, you may rollover a traditional 401k to a Rollover Roth IRA as well. However, there are taxes implications. Learn more about 401k rollovers here.

Use Case Scenarios

Below are a handful of examples to illustrate when and how to use a Roth IRA.

Maximizing Retirement Savings in Your 20s with a Roth IRA

Emily, a 28-year-old physical therapist, has just started her career and is earning $75,000 a year. She’s interested in starting to save for retirement but is unsure about the best approach.

After discussing her situation with a financial expert, Emily decides to open a Roth IRA due to its tax-free growth potential. She contributes $3,000 annually, choosing a mix of stocks and bonds suitable for her long-term growth objectives.

By the time Emily reaches retirement age, her contributions would be worth an estimated $350,000, providing her with a good supplemental retirement account to go along with her other savings.

Switching to a Roth IRA Mid-Career for Tax Diversification

John is 40 years old and has been contributing to a traditional IRA for 15 years. However, after a promotion, he’s now in a higher tax bracket and starts exploring more tax-efficient retirement strategies.

John decides to open a Roth IRA while continuing his traditional IRA contributions. With the help of his designated FitBUX financial expert, he converts a portion of his traditional IRA to a Roth IRA each year via a conversion ladder, understanding that he’ll pay taxes now for tax-free benefits later.

At retirement, John has a diversified tax strategy, allowing him to manage his withdrawals from both accounts to minimize taxes.

Conclusion: Navigating the Path to Retirement with Roth IRAs

In this article, we’ve explored the essential aspects of Roth IRAs, a pivotal tool in the journey towards a secure retirement. I discussed the intricacies of Roth IRAs, contrasting them with Traditional IRAs, and illuminating their unique benefits, such as tax-free growth and flexible withdrawal rules.

Key takeaways include understanding the distinct nature of Roth IRAs as holding accounts with special tax treatments, the advantages of combining a 401(k) with a Roth IRA for diversified retirement income, and the strategic approach to contributions and withdrawals. The article also addresses critical questions about safety, investment options, and income limits, providing a clear roadmap for both beginners and seasoned investors.