Refinancing student loans is always a hot topic. We’ve helped over 30,000 new grads that have more than $2.6 billion in student loans explore refinancing. Since we get no education on money growing up, most are extremely confused about student loan refinancing. Therefore I developed this extensive guide.

As a side note before we dive into the article, you don’t need to be overwhelmed. We have a student loan refinance service whereby you speak with an expert student loan planner and they walk you through all of this.

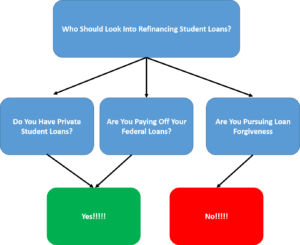

Who Should Look Into Refinancing Student Loans?

The first place to start is to figure out if you should refinance your student loans at all.

There are three scenarios you need to evaluate. Answering these questions can make your decision really easy:

- Do you have private student loans?

- Do you have Federal student loans and are you going to pay them off?

- Do you have Federal student loans and are you going to pursue loan forgiveness? (Note: These are also known as IDR or income-driven repayment plans)

If you have private student loans, the decision is easy. You will look into refinancing and most likely do it.

If you are pursuing Federal student loan forgiveness then stop reading. You do not want to refinance because you will lose the loan forgiveness benefit. This applies to public service loan forgiveness and income-driven repayment plan forgiveness.

What Exactly Is Student Loan Refinancing?

Refinancing in general (this includes any type of refinancing such as home, auto, and credit card consolidation) means that you are replacing one loan with a brand new loan at a new company. This means you will have a brand new rate and term (term means length, i.e. how many years).

This is especially important to understand if you are thinking of refinancing your Federal student loans. Federal student loans have a handful of benefits that private student loans do not include.

For example, you can change your Federal student loan repayment plan whenever you’d like to. Once you refinance your student loans, the only way to change it is to refinance again.

This is important because of “worst case scenarios”. Let’s say something happened to you and your credit score falls below 650. You would not be able to refinance again. If you kept your Federal student loans it would be easier to request deferment, forbearance, or enter and Income-Driven repayment plan.

Here is an article that specifically discusses the pros and cons of refinancing Federal student loans if you’d like to read more.

Why Would A Lender Give Me A Lower Interest Rate?

This is a question we constantly receive from new graduates.

New grads are confused because they are comparing their old rate to the new rate after they refinance their student loans. They are thinking “Why would someone accept less money from me?”

However, you have to look at it from the student loan refinance companies’ point of view. They are investors and have a huge pool of money. This money is sitting there not earning any interest.

The refinance company looks at risk and how much they are rewarded for taking that risk. The reward for risk is the interest rate they charge you.

Therefore, the student loan refinance company has one of two choices: 1) Don’t give you the money and have it sit there earning nothing. 2) Invest in you by refinancing your old loans and collect interest.

Thus, student loan refinance companies do not care what your old rate is….they aren’t collecting the money you pay on the loan you currently have.

This concept of why a refinance company would give you money is important to understand. It will help you realize what their incentives are.

Refinancing Vs. Consolidation

As we discussed above, student loan refinancing is replacing one loan with a brand new loan. Student loan consolidation is simply combining two or more loans into one loan. I’m not going to go into a lot of detail about consolidation because we do so here: Student Loan Consolidation – 4 Things To Know.

You can also check out this video to learn the differences between refinancing and consolidation.

However, there are two points I need to make.

First, when we refinance student loans, sometimes we also consolidate them. For example, we might take multiple student loans, refinance them, and consolidate them into one new loan.

Second, if you are paying off your loans and you decide not to refinance your Federal loans, DO NOT CONSOLIDATE THEM. To find out why, make sure to read the Student Loan Consolidation article mentioned above.

The Four Student Loan Refinance Decisions

Now that you have a high-level understanding of refinancing, its time to make four decisions. We detail each of these decisions below.

Decision #1: What Term Do I Use?

When you refinance your student loans, you have to decide the term you want to use. The term simply means how long you have to repay it if you only make the minimum monthly required payment. It sounds simple but choosing the wrong term is one of the top 3 mistakes we see borrowers make when refinancing.

There are two important concepts you must understand when choosing the term:

- The shorter the term the lower the interest rate.

- The shorter the term the higher the required monthly payment.

This is important to understand because the shorter term loan (i.e. a 5-year loan vs a 20-year loan) has a much lower interest rate. However, refinancing student loans is more than just savings. You have to look at how it impacts your budget as well and factor in items such as cost of living.

One last important point to make. All the student loan refinance companies we partner with have zero prepayment penalty. This means you can go into a longer-term loan and make payments greater than the required monthly payment.

Decision #2: What Type Of Loan Do I Use?

There are three types of student loans that refinance companies offer:

- Fixed Rate Loans

- Variable Rate Loans

- Specialty Loans

Fixed rate loans have the same interest rate for the entire term of the loan. If you are trying to keep your student loan plan simple then I highly suggest sticking to fixed-rate loans.

Variable rate loans have interest rates that can change monthly. Sounds awful, right? So why are people enticed to use these loans?

Variable rate loans have lower starting interest rates than fixed-rate loans and depending on your strategy can be useful. When to use variable rate loans is a complex topic so we created this Variable Student Loan Refinance Video Guide for those that are interested in learning more.

Specialty loans are infrequently used so we won’t go into too much detail in this guide. However, for your reference, they have special features.

For example, one of FitBUX’s lending partners offers an interest only loan whereby you pay only interest on the loan for a given period of time.

Another one of our lending partners offers a Hybrid loan. This loan has a fixed rate for the first five years then has a variable rate thereafter.

In short, if you are trying to save money and keep it simple, stick to fixed-rate loans and move on to the next decision.

Decision #3: Which Loans Do You Want To Refinance?

When one of our FitBUX Members is refinancing we always ask if they’ve checked rates already. One answer we often time receive is, “Yes. However, I didn’t refinance because they offered me a rate in the 5% range and I have loans that are 3% and 4%.”

Guess what? You don’t have to refinance all your Federal loans. If some of your Federal loans are in the 3% or 4% range and the new refinance offer is at 5%….don’t refinance them.

To do so, you’ll most likely need to get a document called the Payoff Statement. The problem is that your current loan servicers don’t always make this easy for you to get.

We are constantly getting on the phone with Members of FitBUX and calling loan servicers to get this information. Approximately 80% of the time we have to get a manager on the phone to get it.

Sometimes it’s worse. Fed Loans won’t give you one but don’t worry. There are workarounds for this problem. Let your FitBUX Expert know if you are struggling to get the payoff statement. We’ll jump on a call to help you as part of our student loan refinance service.

Decision #4: Choosing The Right Student Loan Refinance Company

In this guide, I want to concentrate on items you need to know about. These items influence who will give you a loan, what rate they will give you, and if you should refinance your student loans or not. The following is a list with details of each item.

(Note: Companies publicize some of this data but not all of it. They do not publish it because they consider it proprietary.

We’ve helped so many new grads refinance that we have a good feel of who will give you the best loan based on your circumstances. Our lending partners do not have a problem with our Finance Experts advising people based on what we’ve found. However, they have asked us not to put together a guide detailing our observations and we’ve signed agreements forbidding it. This is why we do not name specific companies and examples in the Refinance Student Loan Guide or our student loan refinance company reviews.)

Profession

This is extremely important. Often times we hear from FitBUX Members that work in health care. They tell us about a co-worker who referred them to a certain lender, they checked rates and it was horrible.

For example, MDs will get really good rates at 3 of our lending partners. The physical therapist they work with can go to the same lender and have the same qualifying figures (i.e. the same credit score and same debt-to-income ratio) and they don’t get anywhere near the same rate.

This is the number one reason why we hear people say they didn’t refinance. That is, they heard from a co-worker that they should check XYZ company so they did. It was such a bad rate they figured all the companies would be the same. Therefore, they decided not to refinance their student loans. Thus, costing themselves money in the long run.

When Did You Graduate

This is important because newer companies look at different items to qualify you than “archaic” companies (FYI: we use the term archaic to describe companies who use traditional industry metrics when qualifying you for a loan. They tend to be banks and credit unions).

The companies that use these archaic qualifications are typically better for borrowers that have been out of school for more than a year and a half. This is the case because you have payment history (i.e. you’ve already started making payments on your loans).

Newer companies have developed underwriting criteria that are geared towards new grads. Those companies will give you better rates and should be the ones you focus on if you recently graduated and are refinancing student loans.

Type Of Income

Are you salaried, hourly with fluctuating hours, are you self-employed, or have specialty type of income? This can make a major difference in getting a loan.

Salary is the easiest for lenders to predict. If you are a salaried employee then you don’t have much to think about.

When you are self-employed or you are an independent contractor you will have to show two years of tax returns to qualify. The only way around that is to have a co-signer. However, there are exceptions to this.

For example, if you are a 1099 employee (a.k.a. an independent contractor), lenders require two years of tax returns. One company we work with doesn’t need two years as long as you work in health care!

This is the most thorough student loan refinance information I’ve found. Thank you for putting it together.