In the complex world of retirement planning, the right guidance can turn confusion into clarity. My name is Joseph Reinke, and I bring over 20 years of wealth management experience to the table.

I have assisted thousands of new graduates on their journey to financial independence, helping them navigate the retirement planning landscape with confidence.

This guide aims to provide guidance in using this strategy, delivering the knowledge you need directly to your fingertips. I’ll also unveil a game-changing trick that young professionals can leverage for substantial financial advantage.

Understanding the Roth IRA: Contributions, Tax Benefits, and Withdrawal Rules

A Roth Individual Retirement Account (IRA) is a particular type of retirement savings account that allows for tax-free growth and withdrawal of funds. The key characteristic that sets it apart is that contributions to a Roth IRA are made with after-tax dollars.

While you don’t receive any immediate tax deduction on the money you invest, the trade-off is that all future withdrawals in retirement are tax-free, provided certain conditions are met.

This contrasts with traditional IRAs and 401(k)s, where contributions are tax-deductible, but withdrawals in retirement are taxed as regular income.

The Concept of a Roth Conversion Ladder

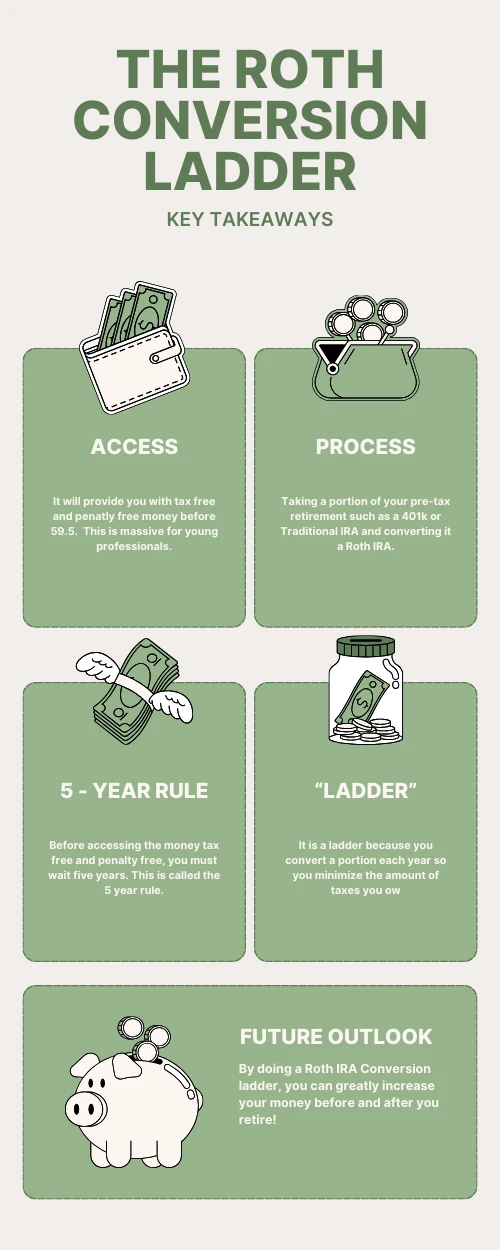

A Roth Conversion Ladder is an advanced retirement planning strategy, particularly useful for those keen on retiring early. It involves the systematic conversion of funds from a pre-tax retirement account such as a 401k or Traditional IRA to a Roth IRA. To put it simply, it’s a financial maneuver that allows you to access your retirement savings without incurring penalties before the typical retirement age of 59.5 years.

The first step is to convert a portion of your pre-tax retirement account into a Roth IRA. This entails a tax liability, as the converted amount is treated as ordinary income for tax purposes in the year of the conversion. However, you perform a conversion ladder which means you only convert a small amount each year. Therefore, you decrease your tax liability..

Once the conversion is made, the five-year clock starts. Thanks to the five-year rule for Roth IRA withdrawals, after a five-year waiting period, the converted amount can be withdrawn tax-free and penalty-free, even if you’re under 59.5.

The “ladder” part of the strategy comes into play as you continue this process year after year, creating a series of conversions (or “rungs”) that become available for penalty-free withdrawal on a rolling basis after their respective five-year periods are complete.

Later in the article, I will illustrate via examples how you can take advantage of “laddering” your withdraws.

The Five-Year Rule and Its Implications

The Five-Year Rule in the context of a Roth IRA refers to a waiting period for tax-free withdrawals. Specifically, you must have owned your Roth IRA for at least five years before you can withdraw your earnings tax-free. This rule applies regardless of your age, ensuring that the tax benefits associated with a Roth IRA are primarily accessible to those who use the account for long-term retirement savings.

The implications of the Five-Year Rule can be significant. For instance, if you’re planning to retire early and access your Roth IRA funds, you need to consider this rule as part of your retirement strategy. That’s where a Roth Conversion Ladder can come into play, where you convert parts of your traditional IRA into a Roth IRA each year, creating a stream of tax-free income five years later. This strategy allows you to access retirement funds early without penalties, but it requires careful planning due to the Five-Year Rule.

The Five-Year Rule, while ensuring long-term benefit from a Roth IRA, also imposes certain restrictions on withdrawal strategies. The implications of this rule are particularly significant when you’re considering early retirement. A misunderstanding of this rule can lead to unexpected tax liabilities and penalties, undermining the efficiency of your retirement strategy.

For instance, if you opt to withdraw your Roth IRA earnings before the five-year period has passed, those earnings will be subject to taxes and potentially a 10% penalty if you’re under 59.5 years of age. This makes it imperative to consider the timing of your Roth IRA establishment and the consequential withdrawals.

On the other hand, for those planning to retire early, a Roth Conversion Ladder can help navigate the constraints of the Five-Year Rule. By converting portions of a traditional IRA to a Roth IRA annually, the five-year waiting period starts anew with each conversion. This strategy provides a yearly stream of tax and penalty-free income after the initial five years, granting more flexibility in withdrawal strategies. Understanding the nuances of the Five-Year Rule is critical in effectively leveraging a Roth Conversion Ladder and ensuring a smooth transition into early retirement.

Strategic Planning

Strategic planning is crucial and should take into account your current age, potential income trajectory, and retirement goals. These factors impact the timing and amount of conversions, which in turn affect the taxes paid and the benefits reaped.

For younger individuals in the early stages of their careers converting traditional IRA funds to a Roth IRA can be a smart move. Tax rates are likely lower now than they will be in the future, making it a cost-effective strategy. Furthermore, the long time horizon until retirement allows the Roth IRA to grow tax-free, maximizing the benefits of compounding. You could be in a place to take advantage of this with an old company 401k when you roll it over.

If you’re in your peak earning years, careful consideration is needed. Converting a large traditional IRA to a Roth IRA will increase your taxable income for that year, potentially pushing you into a higher tax bracket. However, a series of smaller, strategic conversions over several years can spread out the tax impact while still allowing you to build a significant Roth IRA balance for tax-free withdrawals in retirement.

Also, some people recommend doing Roth Conversion when the market is down. However, I typically say this is a minor detail and doesn’t benefit you enough to worry about it. The reality is your income level is way more important than the market level.

Examples Of Roth Conversion Ladder in Different Situations

Let’s explore how the Roth Conversion Ladder might apply to three specific situations: a student, a stay-at-home individual, and someone on an Income-Driven Repayment (IDR) Plan.

The Student

Let’s say you worked for four years after completing her undergrad, have a 401k, and are now going back to graduate school

As a student she will be in a lower tax bracket. Converting your old company 401k to a Roth IRA means you could pay no taxes and have full access to the money in 5 years without penalty. To make sure you don’t pay taxes now, you could split the conversion.

For example, if you have $40k in a 401k you could convert $20,000 during your first year of studying and $20,000 the second year. Doing half in one year and half in the next is the laddering portion of the conversion.

Student Loan Borrowers Using An Income-Driven Repayment (IDR) Plan

If you’re on an IDR plan and you are married you can potentially take advantage of a Roth IRA conversion ladder.

The conversion of traditional IRA funds into a Roth IRA increases your taxable income for the year, which could potentially influence your monthly IDR payments. However, if you are not going to be working in a given year or have a low amount of taxable income

The Stay-At-Home Individual

Stay-at-home individuals often have lower taxable incomes, which makes the Roth IRA conversion less tax-heavy.

Starting a Roth Conversion Ladder might prove beneficial in preparing for retirement, even without a regular income.

It’s an opportunity to convert existing traditional IRA funds into a Roth IRA at a lower tax rate, and let the money grow and be available for future penalty-free and tax-free withdrawals.

Tax Implications

A Roth Conversion Ladder has significant tax implications. When you convert funds from a pre-tax account to a Roth IRA, the amount you convert is counted as taxable income for that year. However, once the money is inside a Roth IRA, it grows tax-free and can be withdrawn tax-free in retirement.

This is a strategic advantage of the Roth Conversion Ladder. The key to optimizing this strategy is to convert amounts that keep you within your current tax bracket, thus avoiding a higher tax bill in the year of conversion.

A Roth Conversion Ladder is to make conversions during years of low income. This ensures that the income generated through conversion stays within lower tax brackets.

Additionally, converting smaller amounts over a longer period can spread out the tax liability, instead of incurring a large tax bill from a single large conversion.

Common Mistakes and How to Avoid Them

In the rush to maximize the benefits of a Roth Conversion Ladder, individuals often make some common mistakes. One of these is not considering the five-year rule. Each conversion has its own five-year period before the converted amount can be withdrawn tax-free. A hasty withdrawal before this period lapses can lead to a significant tax penalty. To avoid this, always ensure that you plan your conversions and withdrawals meticulously, keeping the five-year rule in mind.

Another common error is ignoring the effect of conversions on your tax bracket. Converting too much in a single year could potentially push you into a higher tax bracket, leading to a higher tax bill. A smart way to avoid this is to convert smaller amounts over many years, ensuring that the converted amount does not push you into a higher tax bracket.

Not considering the impact of market conditions is another common pitfall. Converting during a market high means you’ll pay more tax on the conversion, while converting during a market low reduces your tax liability. Be patient and try to time your conversions to coincide with market downturns.

Lastly, not seeking professional advice can lead to missteps. The rules surrounding Roth Conversion Ladders can be complex and individual circumstances can vary widely. If you have any questions, feel reach out to FitBUX by creating an account and scheduling a call.

By being aware of these common mistakes and taking steps to avoid them, you can optimize your Roth Conversion Ladder strategy and enhance your financial future.

Conclusion

In conclusion, there are several key points to remember when considering a Roth Conversion Ladder:

- A Roth Conversion Ladder involves gradually converting portions of a traditional IRA to a Roth IRA. This approach can offer tax advantages, particularly during years of lower income or market downturns.

- Each conversion is subject to a five-year rule, meaning you must wait five years before withdrawing the converted funds to avoid any tax penalties.

- It’s important to avoid converting too much at once, as this can push you into a higher tax bracket and increase your tax liability. Instead, it’s advisable to convert smaller amounts consistently over a longer period of time.

- Seeking professional advice is crucial as the rules surrounding Roth Conversion Ladders are complex and individual circumstances may vary. Consulting with a tax or financial advisor is always a wise decision to ensure you make the most effective choices for your personal situation.

Additional Resources

For a deeper understanding of Roth Conversion Ladders, consider exploring the following resources:

- Internal Revenue Service (IRS): The official IRS website offers a wealth of information on Roth IRAs, including detailed rules on conversions. Visit IRS Roth IRAs and IRS Retirement Topics – IRA Contribution Limits

If you need further assistance or have any questions, do not hesitate to reach out to our team at FitBUX.