As a physician, you have the unique opportunity to qualify for a special type of physician home loan. These home loans offer some distinct advantages over traditional mortgages.

However, there are also some potential drawbacks to consider before taking out a physician home loan.

Physician Home Loan: What Is It and How Does It Differ from a Regular Mortgage?

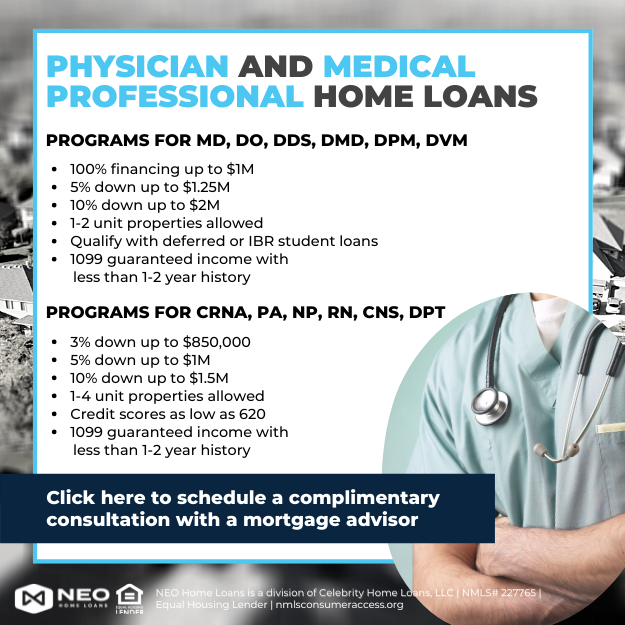

A Physician home loan is a mortgage that is specifically designed for doctors. Which type of doctor depends on the lender you go to. Below of the types of degrees we typically see qualify:

- M.D.

- D.O.

- D.D.S.

- D.M.D.

- D.P.M.

- D.V.M.

The terms and conditions of these loans are typically more favorable than those of regular mortgages, making them a good option for medical residents, fellows, and new medical professions who are looking to purchase a home.

Physician home loans often have lower interest rates and down payment requirements than conventional mortgages, making them easier to qualify for.

Side Note. Physician home loans and professional home loans are similar but they are not the same thing. New grads and even those in the real estate industry get them confused all the time. You can read more about professional home loans here.

The Pros and Cons of Taking Out a Physician Home Loan

Before making this decision, it is important to weigh the pros and cons of such a loan.

Pros

The main advantages of physician home loans are:

- Private Mortgage Insurance (PMI) is not needed: On typical first time home buyer loans and on mortgages with less than a 10% down payment, you have to pay for insurance. This is an added cost that you do not have to pay on a physician home loan.

- Higher Loan Amounts: These loans have higher loan limits than a conventional loan. Most lenders will allow you to borrow between $1 million and $2 million. Should you borrow that much for a house? I highly recommend developing a financial plan before taking out that much loan.

- Qualifying Is Easier If You Have Student Loans: Qualifying for a conventional loan when you have student loan debt is hard. These loans use different calculation techniques especially when you are on an income-driven repayment plan. Therefore, it is easier to qualify for them.

- Little or No Down Payment: New grads often think these loans are always have 0% down payments. That is not the case. It will depend primarily on your credit score and loan amounts. However, you can buy a house using these loans with 0% – 10% down.

- Buy A Home Before Starting Work: You typically can qualify for these loans 90 days before you start working. However, you typically have to have a contract in hand showing your income. Some allow you to qualify without a job but I highly suggest you do not do that.

- Buying Investments: Some lenders, such as Neo Home Loans, allow you to use these loans for investment properties. However, it is hard to cash flow on a property that is 100% financed. Therefore, I only recommend using them for investment properties in two circumstances:

- You are a real estate investor and really know what you are doing with your financing, or

- You are buying something like a duplex and plan on living in one side of it. This could be a great way to go for a new grad and is one of my favorite ways of building wealth.

Cons

However, there are some drawbacks to consider as well.

- Qualifying Isn’t Always Easier: Higher credit scores are required to qualify relative to conventional mortgages.

- 100% Financing: I was in the mortgage industry back in 2007. Trust me and about 3 million other people when I say 100% financing isn’t always the best for your financial plan. Do not feel the need to rush in and buy a house just because you can. In fact, I speak to physicians on a weekly basis that are living pay check to pay check because they bought too much house. Do not do this to yourself.

- Interest Rate: Interest rates on these loans are competitive. However, since you can get 100% financing and there is no PMI, they tend to have a slightly higher interest rate. You have to get different offers and compare them. Also, most physicians use these loans to purchase the house with the intent of refinancing down the road when the time is right. Doing so will allow you to take advantage of lower interest rates in the future. But… you can’t always depend on that because interest rates might go up and you may never get a chance to refinance.

How to Get the Best Terms on Your Physician Home Loan

As a physician, you’re used to being in high demand. Your skills are in high demand, and that means you have your pick of job offers.

Lenders also want your business because of the historically low default rates on mortgages by physicians. That is why they offer these loans to begin with.

However, the better you make yourself look to the lender, the better terms you’ll receive.

If you’re looking for tips on how to get the best terms on your physician home loan, here are a few things to keep in mind:

1) Have a Strong Credit Score – The Higher Your Credit Score Is, the Better Interest Rate You’ll Qualify for from Lenders.

Most lenders will allow you to qualify for a physician home loan with a 680 credit score. However, the higher that number is the lower your rate will be.

Therefore, you should do two things immediately:

- Know what your credit score is. I use CreditKarma because its free. Its great because I can easily see my score. However, I personally think the rest of CreditKarma’s platform sucks and is basically there to push ads. Therefore, if you use CreditKarma, get your score and leave. Don’t get sucked into the ads.

- Start working on improving your credit score. The best way to do this is by manipulating your credit optimization ratio.

2) Shop Around – Don’t Just Go with the First Lender Who Gives You an Offer.

Talk to multiple lenders and compare rates before making a decision. And don’t forget about online lenders!

They often have lower rates than traditional brick-and-mortar institutions. When shopping around, make sure to ask each lender what kind of fees they charge (e.g. Origination fee, application fee, etc.) so there aren’t any surprises down the road.

As I mentioned, few lenders offer physician home loans. Therefore, don’t be surprised if a lender you speak to does not know what you are talking about.

Two good lenders that FitBUX has partnered with and that you should check out are Neo Home Loans and Movement Mortgage.

3) Are Points Good – See If You Can Get A Lower Rate

Paying points on a mortgage can get you a lower interest rate. However, you have to make sure you are using them correctly so you can maximize your net wealth. Ask your lender for various point offers.

Then I highly recommend using FitBUX’s mortgage point calculator to figure out if you should use them or not. Points can literally save you $100,000s over the life of the mortgage if you use them correctly.

FAQs in Relation to Physician Home Loan

Do doctors get better mortgage rates?

The answer may vary depending on the financial institution, but in general, doctors do receive better mortgage rates than the average person.

One of the reasons for this is that lenders view physicians as low-risk borrowers because they have a stable income and employment.

Additionally, most doctors are able to make larger down payments on their homes than the average person, which further lowers their risk in the eyes of lenders.

What credit score is needed for a physician loan?

There is no one definitive answer to this question as credit requirements can vary depending on the lender. However, most physician loans typically require a minimum credit score of 680-700.

Do Physician loans have higher interest rates?

There is no definitive answer to this question as interest rates on physician loans can vary depending on the lender and other factors. However, some sources suggest that physician loans may have higher interest rates than conventional mortgages.

This is likely because physician loans are considered to be higher risk than other types of loans. As such, lenders may charge higher interest rates to offset this risk.

Ultimately, it is important to shop around and compare interest rates from different lenders before deciding on a loan.

Is a physician loan the same as a conventional loan?

A physician loan is typically offered by banks or lending institutions to physicians and other medical professionals with special terms and conditions.

These loans often have lower interest rates than conventional loans, and may also offer deferred payments or forgiveness of principal in certain cases.

Conclusion

Physician home loans offer some distinct advantages over traditional mortgages, but there are also some potential drawbacks to consider before taking out one of these loans.

If you’re looking for information on home ownership and fitting a home into your financial plan, then look no further! Our coaches and technology can provide you with all the resources you need to make informed decisions on your journey to financial freedom. Become a Member of FitBUX today to get started!

By Joseph Reinke, CFA