A professional mortgage loan is a type of loan that is specifically designed for health care professionals and medical doctors. This is important to understand because many people confuse them with physician loans. Therefore, many health care professionals do not think they can qualify for them… but you can!

Below you’ll learn what a professional mortgage loan is, how to qualify for one, and the pros/cons of them.

Note: Physician mortgage loans and professional mortgage loans are often referred to as the same thing. However, they are different. If you are a physician, be sure to read about the details of a physician home loan.

What Is a Professional Mortgage Loan?

A Professional mortgage loan is a type of home loan that is typically used by medical professionals, lawyers, and dentists. This loan offers special benefits such as a relaxed qualification standards (I detail the qualification standards below).

You can get this type of loan through many different lenders, but they all typically have the same basic requirements. To qualify you will usually need to have a strong credit score and a steady income.

You will also need to be employed in a professional field, such as medicine, law, or dentistry. Below I detail which professions will qualify for a professional home loan.

Who Can Qualify for a Professional Mortgage Loan?

To qualify for a professional mortgage loan, you’ll need to meet the following criteria:

- You must be employed in one of the eligible professions.

- You must have a good credit history.

- You must have a steady income.

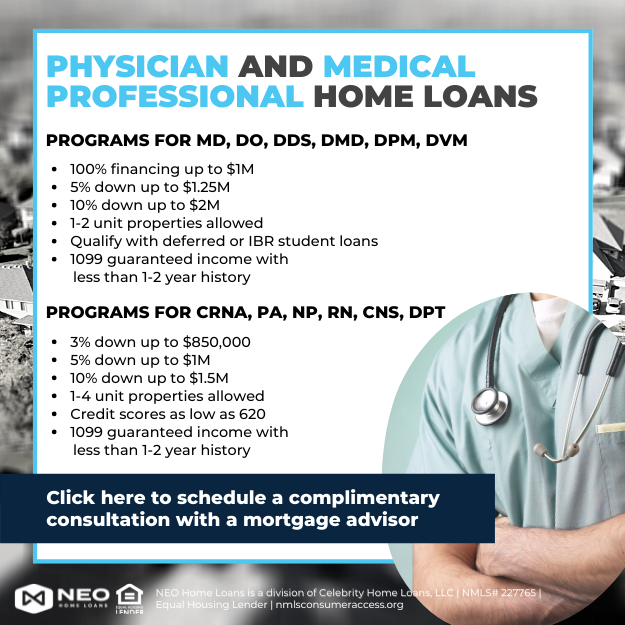

Eligible professions very by lender. However, below are professions that qualify through FitBUX’s mortgage partner Neo Home Loans:

- MD

- DO

- DDS

- DMD

- DPM

- DVM

- CRNA

- PA

- NP

- RN

- CNS

- DPT

What Are the Benefits?

One of the biggest benefits is being able to purchase a home sooner than if you were to use traditional mortgage. Below are additional benefits:

- Professional mortgages typically have slightly higher rates but may still pay less over the life of your loan relative to a conventional loan because of no PMI. I also recommend asking your lender about paying mortgage points. The combination of a professional mortgage loan and paying points can save you $10,000s over time.

- Many offer 100% financing options meaning you don’t have to have a down payment. For example, Neo Home Loans offers financing up to $1 million dollars with no down payment.

- You can buy multi-unit properties.

- If you are on an income-driven repayment plan with your student loans you can qualify. Read more here about buying a house with student loans.

- You can use 1099 income with less than 2 years history.

- Residents and Fellows qualify.

- Credit scores can be as low as 620.

- They typically do not require mortgage insurance (PMI) like an FHA loan does.

Are There Any Drawbacks ?

While there are many benefits to getting a professional mortgage loan, there are also some drawbacks.

One of the biggest drawbacks is that you may end up paying more interest over the life of the loan. Professional mortgage loans typically have higher interest rates than standard home loans, so you’ll need to factor that into your budget.

However, most individuals that use these loans have a specific strategy. They use the loans to purchase the house and they intend to refinance to a lower interest rate once they have enough equity in the house to do so.

Another potential drawback is that not all lenders offer them, so it may be harder to find a good deal. However, both Neo Home Loans and Movement Mortgage are two lenders that typically have competitive rates.

Before you decide to get a professional mortgage loan, be sure to weigh the pros and cons carefully to ensure that it’s the right decision for you.

How Do You Get a Professional Mortgage Loan?

Before getting a mortgage, I always recommend building your financial plan and knowing exactly how much home you can afford and when you should be buying it.

Once you know this information, then applying for a professional mortgage loan is similar to other loans. Below are the typical steps to take:

- Decide how much home you can afford. If you need help with this FitBUX has awesome home ownership tools that customize solutions for you.

- Complete a lenders online questionnaire.

- Schedule a call and discuss your situation with a loan officer.

- Submit the application.

- The loan typically closes in 15 – 45 days.

Conclusion

If you are a health care professional or medical doctor, a professional mortgage loan may be the right choice for you. A professional mortgage loan offers many benefits and can get you in a home sooner.

If you’re looking for a professional mortgage loan and want help building your financial plan, then look no further!

FitBUX can help get you with our one of a kind financial planning technology. We’ve helped young professionals manage over $2.2 billion in assets and debt so we know we can help you too!

By Joseph Reinke, CFA