Home prices are at all time highs. Mortgage rates are climbing. To make things even more challenging, many young professionals are trying to buy a house with student loan debt.

Buying mortgage points may be your secret weapon to reducing the cost of your mortgage and saving a ton of money.

Below, I explain everything you need to know about mortgage points such as:

- How mortgage points can save you $1,000s;

- When you buy points…and when not to; and

- Multiple ways to determine whether paying mortgage points is right for you.

Understanding the contents in this article will empower you to use a mortgage point calculator to determine if paying points is right for you or not.

What Are Mortgage Points?

First things first. We need to define or explain what a mortgage point is.

The Federal government defines points as a way to “lower your interest rate in exchange for an upfront fee.”

Mortgage points are also referred to as ‘buying down the rate’ or ‘discount points.’

One point is equal to one percent of the starting loan balance.

I’ll explain using the following examples.

Let’s say you are buying your first house and the mortgage is $400,000. Buying one point on a $400,000 mortgage would cost you $4,000.

Finance people like to confuse you so mortgage points are are often referred to as “basis points”.

This terminology is important to know because lenders often times use it. For example, instead of saying the cost to lower your mortgage rate is .25 points, they will say that it costs 25 basis points. This means the cost is 0.25% of the mortgage. I.e. on a $400,000 mortgage, the cost would be $1,000.

How Many Points Can You Buy On A Mortgage

When I explain points to individuals, people get excited and want to buy down the rate as much as possible.

However, how much each mortgage point lowers the rate varies on a number of factors. The factors are:

- The lender: All lenders have different amounts each point lowers the interest rate

- The type of mortgage loan (Conforming loan, jumbo loan, etc…)

- The interest rate environment, i.e. are rates going up, down, flat, etc…

Points will be listed on your loan estimate document and the closing disclosure. You then pay them upfront, at the closing of the loan, and they are considered prepaid interest.

Being considered prepaid interest is important for tax deductibility which I touch on more in a later section.

Is It Better To Pay Mortgage Points Or Have A Higher Interest Rate?

Short answer, it depends. I will explain using a few scenarios below. However, there are three mistakes I want to explain first to help answer this question before even getting into the math side of things.

Mistake #1

People often make the wrong choice because they use what is called the Cost Method. This method unfortunately is the wrong method to determine whether one should buy points.

The Cost Method strictly looks at the cost of a mortgage over the life of the loan when you buy points and when you don’t. The problem is that this method doesn’t factor in time.

Since buying points up front reduces your monthly mortgage payment, the longer you stay in your home, the more you save relative to paying no points.

Therefore, in general the longer you are in your home, the more you save and the more it make since to pay points. Thus, if you use the cost method, you ignore the time factor.

I will discuss two methods you should use in a minute but first I want to point out two other mistakes people make.

Mistake #2

People who paid points often shy away from refinancing, even if they can get a better rate. In their mind, since they bought points, they want to keep “benefiting from their purchase.” In other words, they are looking in the rearview mirror.

This is absolutely the wrong way to look at refinancing. The points you paid in the past should be considered a sunk cost. You paid them already and you can’t change that.

The real question to answer is, “Does refinancing (with or without paying mortgage points) put me in a better position today relative to my current mortgage?”

Mistake #3

I’ve been seeing this advice a lot lately and it makes me cringe every single time. It goes something like this?

“Don’t pay mortgage points right now because rates have risen. Wait until rates come back down and refinance at that time instead. There is no point (pun intended) to pay mortgage points for no reason since you’re going to refinance anyway.”

Horrible, horrible, horrible!

Nobody knows what the future holds for interest rates. If they do go down, nobody can tell you when they are going down.

Therefore, you have to make your decision based on what you know today. When/if rates do go down, do the analysis explained next to determine whether you should refinance and pay mortgage points again.

Two Methods Used To Determine If You Should Pay Mortgage Points

There are two methods you should use when it comes to mortgage points that I explain below. They both answer:

- Whether you should pay mortgage points, and, if so:

- How much you should pay.

The two methods are:

- The Break-Even Method

- The Investment Method

The break-even method is most commonly used because it’s the easiest to calculate. However, I recommend using the investment method. I explain both methods below and detail why I favor the latter.

The Break-Even Method

When you pay mortgage points ou are reducing the interest rate. Therefore, you reduce your required monthly payment.

The difference between the monthly payment amounts is your ‘savings.’

For example, a no point loan has a monthly payment of $1,000. A loan paying one mortgage point has a monthly payment of $950. Your monthly savings is $50.

Then you simply divide the cost of the loan by the monthly savings. The result is how many months it would take for you to ‘break-even.’

Before diving into an example, let me explain a critical item first.

Critical Item You Need To Know

As I previously mentioned, you have to decide how long you are going to keep this specific mortgage. Notice I said “mortgage”, not “home.”

Many people make the mistake of comparing the break-even point to how long they will be in the house.

Using both terms interchangeably only makes sense if you are planning on selling the house say within five years. This is the case because you would get rid of both at the same time.

Now, here is the key statistic you need to know. The majority of mortgages (not necessarily the ownership of a given home) are ended within 10 years.

People often times refinance and get a new mortgage to save money. Sometimes they need money for something else like a medical emergency and do a “cash out” refinance. Other times people may pay off the loan in 10 – 15 years because they just don’t like debt etc.

With this number in mind, the rule of thumb is that you typically want to break-even within 6 years. Obviously, the sooner you break-even, the better.

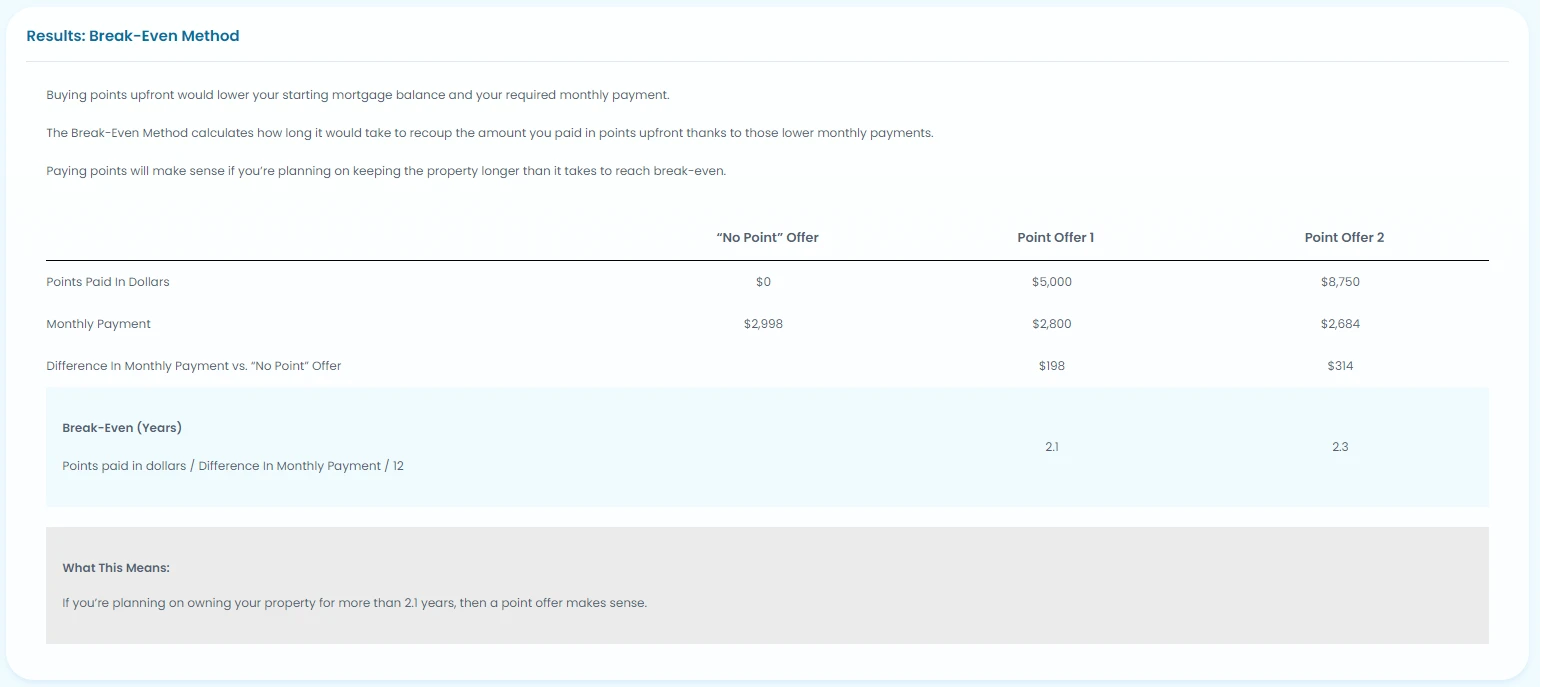

Example Of The Break-Even Method

Let’s say you have three offers for your $400,000 mortgage:

- Pay no mortgage points and get a 6% rate

- Pay one mortgage point (i.e 1%or $4,000) and get a 5.625% rate

- Pay two mortgage points (i.e. 2% or $8,000) and get a 5.375% rate

Below are the results from FitBUX’s mortgage point calculator. As you can see, your break-even for paying one mortgage point is 2.1 years. Therefore, if you foresee staying in your home (or holding that mortgage) for more than 2.1 years you would pay the mortgage point.

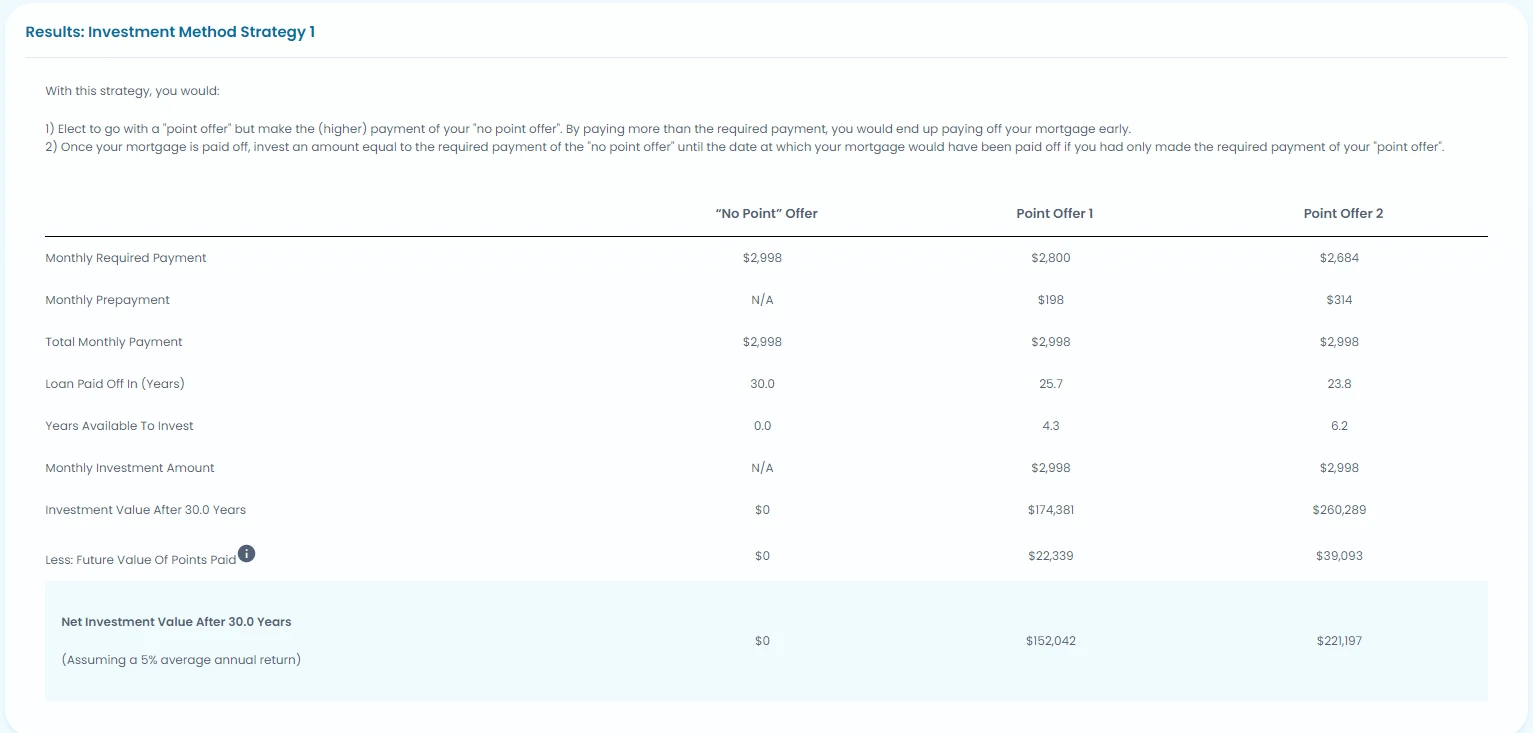

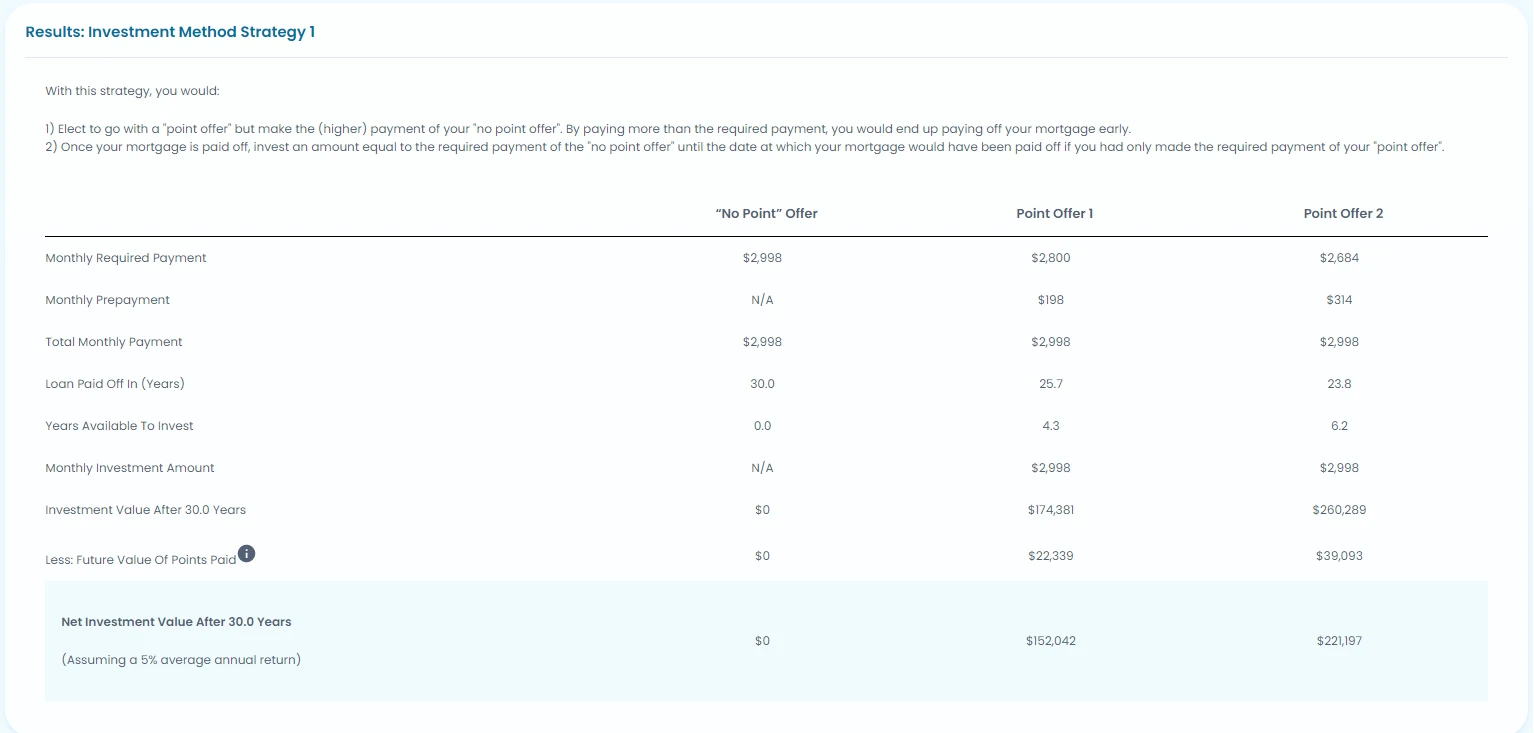

The Investment Method

I mentioned earlier that the investment method is the best method to use. The reasons are:

- It will show you the true value of paying mortgage points over time

- It will help you maximize your financial plan

As I’ve explained previously, paying mortgage points reduces your monthly payments. From there, you have three ways to deploy the money you’ve saved each month. You can:

- Spend it

- Use it to prepay the mortgage and pay off your mortgage early

- Invest it

If you are going to spend it, then the break-even method will work for you. Simple.

However, if you’re considering investing or paying off debt, the investment method is the way to go.

The investment method calculations are complex. This is why FitBUX has built a mortgage point calculator (available in our free membership) which does the heavy lifting for you.

Example of the Investment Method #1

I will explain the investment method using the same figures I used in the break-even method.

Option 1: Pay one mortgage point and use the savings to prepay the mortgage.

If you did this, your estimated net investment value in 30 years would be $70k.

Now, let’s look at it from an investment standpoint:

“I make a $4,000 investment today, it will grow to approximately $70,000 over the next 30 years. Is that worth it to me based on my own situation?”

If the answer is yes, pay the mortgage point.

Example of the Investment Method #2

Option 2: Use your savings and invest it immediately instead of paying off the mortgage early.

If you did this, your estimated net investment value in 30 years would grow to $61.5k.

Do you believe a $4,000 investment is worth $61.5k over 30 years? If yes, then pay one mortgage point.

The Investment Method Is The Way To Maximizing Your Financial Plan

The great thing about the Investment Method is that it’s a key calculation when you build your financial plan

If you use option 1 and use the savings to pay off your mortgage early, your net investment value will grow to $70k.

If you use option 2 and invest the savings instead, your net investment value will grow to $61.5k.

Therefore, to maximize your finances, you’d want to use option 1 as your investment will grow more over 30 years. Use the savings to pay off the mortgage faster since the net investment value is more than option 2.

Seller-Paid Points Interest Rate Buy Down Strategy

Yes, it’s a mouth full. It basically means that the *seller* will pay for points to help get a deal done. I explain in more details below.

A seller’s market is where sellers set the terms due to lack of housing supply. Conversely, a buyer’s market is when buyers set the terms due to an oversupply of housing.

Currently, many real estate markets across the country are shifting from a severe seller’s market to a balanced/buyer’s market. This means sellers are seeing less potential buyers, and homes are also staying on the market longer.

Therefore, sellers get motivated to offer concessions such as price reductions or seller-paid closing costs.

When contemplating a transaction, buyers want to focus on reducing their monthly payments and make the home as affordable as possible. Therefore, in a buyer’s market, many will put in an offer at a reduced price.

However, sellers may still be reluctant to drop the price. If the seller is stuck on a given price, buyers should consider asking the seller to contribute towards the buy-down of their mortgage rate as opposed to reducing the sales price. In effect, the seller is buying points on behalf of the seller.

In fact, a seller contribution can be two to three hundred percent more effective to reduce the monthly payment than a direct price reduction. Let’s look at an example.

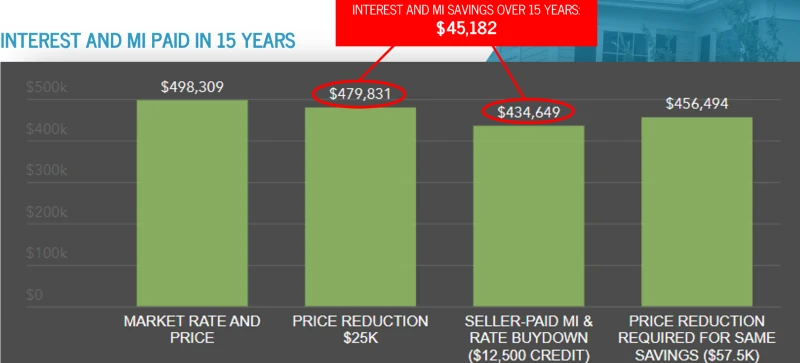

Example Of Seller-Paid Points

Here’s an illustrative explanation of how powerful this seller concession can be.

In the example, we use seller-paid points to buyout mortgage insurance and reduce the interest rate.

The first column below is the Market Rate And Price. You will see a market rate for an average credit score borrower and the monthly payment. The monthly payment includes principal, interest, taxes, insurance, and mortgage insurance.

The second column assumes the borrower negotiates a $25k price reduction. Therefore, the monthly payment is reduced by $139.55.

The third column assumes the buyer does not want to negotiate a price reduction. Instead the buyer was able to negotiate a seller concession of $12.5k. The seller concession was then used to first buyout the mortgage insurance for $4.3k. Then the seller concession was used to permanently buy down the interest rate with the additional $8.2k.

This strategy resulted in an interest rate reduction of .626%, the elimination of the monthly mortgage insurance premium, and a monthly payment savings of $316.60.

The fourth column compares the monthly savings of a price reduction relative to using the seller concession to pay points. In order to get the same savings, the seller would have to agree to a sales price reduction of $57.5k!

Obviously as a buyer, you want to negotiate as much of a sales price reduction and seller concessions as possible. However, many markets are still decently competitive. Therefore, it’s much more likely you will be able to negotiate a $12.5K seller concession than a $57.5k price reduction.

The Long-Term Benefits Of Seller Paid Points

This strategy is powerful for maximizing monthly affordability. It also compounds for massive long-term savings.

Over 15 years, the seller paid mortgage insurance and rate buydown strategy saves $45,182 more than a $25k price reduction strategy.

In summary, negotiating seller paid concessions to permanently buydown the rate of your mortgage and buying out the mortgage insurance are strategies that maximize homebuyer affordability. They are much more effective at reducing the mortgage costs than are purchase price reductions alone.

Mortgage Point Tax Deductibility

Good news. Mortgage points are prepaid interest. Therefore, they are tax deductible.

If you have a property purchased prior to December 2017, you can deduct the points if your mortgage was less than $750,000. If you bought a house after December 2017, you can deduct them if the mortgage was less than $1,000,000.

You do not get to deduct all the points in the same tax year however. Each year, you can deduct only the amount of interest that applies as mortgage interest for that year.

However, there is one primary exception when you refinance your mortgage or sell your house. In this situation, the amount of mortgage points you haven’t deducted can all be deducted in the tax year the house was sold.

For example, let’s say you paid $3,000 in mortgage points. After x years you have already deducted $1,000 and sell your house. Then you can deduct $2,000 in that tax year.

Temporary vs Permanent Interest Rate Buydowns

To this point, everything I’ve discussed is related to paying mortgage points in order to permanently reduce your interest rate.

There is another way to reduce or buydown your interest rate that is less popular. Never the less, you may find it beneficial. Therefore, I explain what a temporary buydown of interest rate means below.

Temporary Buydown

A temporary decrease in your mortgage interest rate during the first 1 to 3 years is referred to as a 2/1 buydown or a 3/2/1 buydown.

After the temporary buydown period ends, the interest rate will return to the original rate you were eligible for.

For example, if you qualified for a mortgage at a 7% rate today, you could use a 2/1 buydown to reduce your rate to 5% for the first year and 6% for the second year. After year two, your rate would go back to the 7% you originally qualified for.

Items To Know About Temporary Buydowns

There a a few major differences between temporary buydowns and the permanent buydown I explained earlier in this article:

- The funds for a temporary buydown must come from the seller in the form of seller concessions. In short, you cannot use your own money.

- You must be able to qualify for the mortgage at the permanent rate.

- If you decide to refinance your loan prior to the temporary buydown period ending, the remaining funds in your escrow account used for the buydown will go toward principal payments on the existing mortgage.

When To Choose A Temporary Rate Buydown

As I previously mentioned, paying points to reduce your interest is mostly done on a permanent basis. However, there is one time that I’ve seen that makes since to use a temporary buydown strategy.

You anticipate a large salary increase in the future. Therefore, you want a some savings in the short-term before your income goes up.

Frequently Asked Questions

How many mortgage points can I buy?

Technically, you can buy as many as you want. However, the more you buy the more they cost and the less the interest rate drops. For example, one point might drop the rate by .25%. 2points might only drop it another .15%. Therefore, the longer your break-even point becomes.

Why do lenders offer points?

Money today is more valuable than money tomorrow. Therefore, lenders do a calculation whereby they are indifferent as to receiving the interest up front or over time. That is how they calculate the cost and interest rate decrease when buying points.

How do mortgage points work with ARM Loans?

Mortgage points on an adjustable rate mortgage (ARM) work exactly the same as fixed rate mortgages. However, most ARMs adjust in five or seven years. This is important because ARMs are most of the time refinanced. If they aren’t refinanced, then the points aren’t applied once the loan starts adjusting. The lower interest rate only applies to the fixed rate time period. The fixed interest rate period is typically five to seven years. Therefore, it is really important to calculate the break-even points. However, most of the time it makes no since to pay points on an ARM.

Can you negotiate points on a mortgage?

You can negotiate origination points but these are different that points to reduce the interest rate. When it comes to negotiating paying points to reduce the interest rate, the answer is no!

Conclusion

Mortgage points are often overlooked by many home buyers. However, once mortgage points are explained you can see how powerful they are in regards to saving money.

This is one of the biggest hidden gems in the finance world and I hope you take advantage of it.

If you need help, be sure to use FitBUX’s mortgage point calculator.

If you need help determining how much home you can afford or developing a sound financial plan FitBUX can help. Become a member and use their financial planning technology. You can also schedule a call with one of our FitBUX Coaches to get your questions answered.

By Joseph Reinke, CFA and Josh Mettle, Neo Home Loans