Before using a student loan refinance calculator, you need to decide whether you’re doing a pay off strategy or whether you’re doing an Income Driven Repayment (IDR) plan.

If you’re going down the IDR route, then refinancing is not something you should be looking in to. Therefore, you shouldn’t use the student loan refinance calculator. You should use the IDR calculator.

If you’re doing a pay off strategy then refinancing is a service you may decide to do because it potentially saves thousands of dollars. However, the key is figuring out exactly how much it will actually save you.

One last item to note, if you haven’t read our student loan refinance guide I suggest doing that first before continuing on.

Avoid Bad Student Loan Refinance Calculators

There are two main flaws with most student loan refinance calculators on the web. I’ll touch on it briefly below. However, you can read more details on how to avoid the 3 largest refinance mistakes in this article.

Most student loan refinance calculators tell you how much refinancing saves you or cost you. However, it’s heavily skewed. For example, if its showing you savings these calculators will over estimate how much you will save.

The primary flaw in these student loan refinance calculators stems from an apples-to-oranges comparison.

For example, you currently may be in a 10 year loan but you get a refinance quote for a 5 year loan. They may show you saving something like $40,000.

However, the 5 year loan is going to have a much higher required payment. Therefore, most of the savings is due to you paying more each month not the lower interest rate.

Below I’m going to show you how to correct this mistake. I’ll be using FitBUX’s student loan refinance calculator to do so.

How To Use Our Student Loan Refinance Calculator

FitBUX’s student loan refinance calculator can be used to do two calculations:

- Helping you to decide if you should refinance your current loans by comparing your refinance options to your current loans

- If you are going to refinance, comparing your refinance offers

Below I detail both.

Refinancing Offer Vs Your Current Loans

Step 1

Create a FitBUX account and input all necessary information such as your student loans. FitBUX’s student loan refinance calculator is free to use but you will need to have an account so the results are customized to your situation.

Step 2

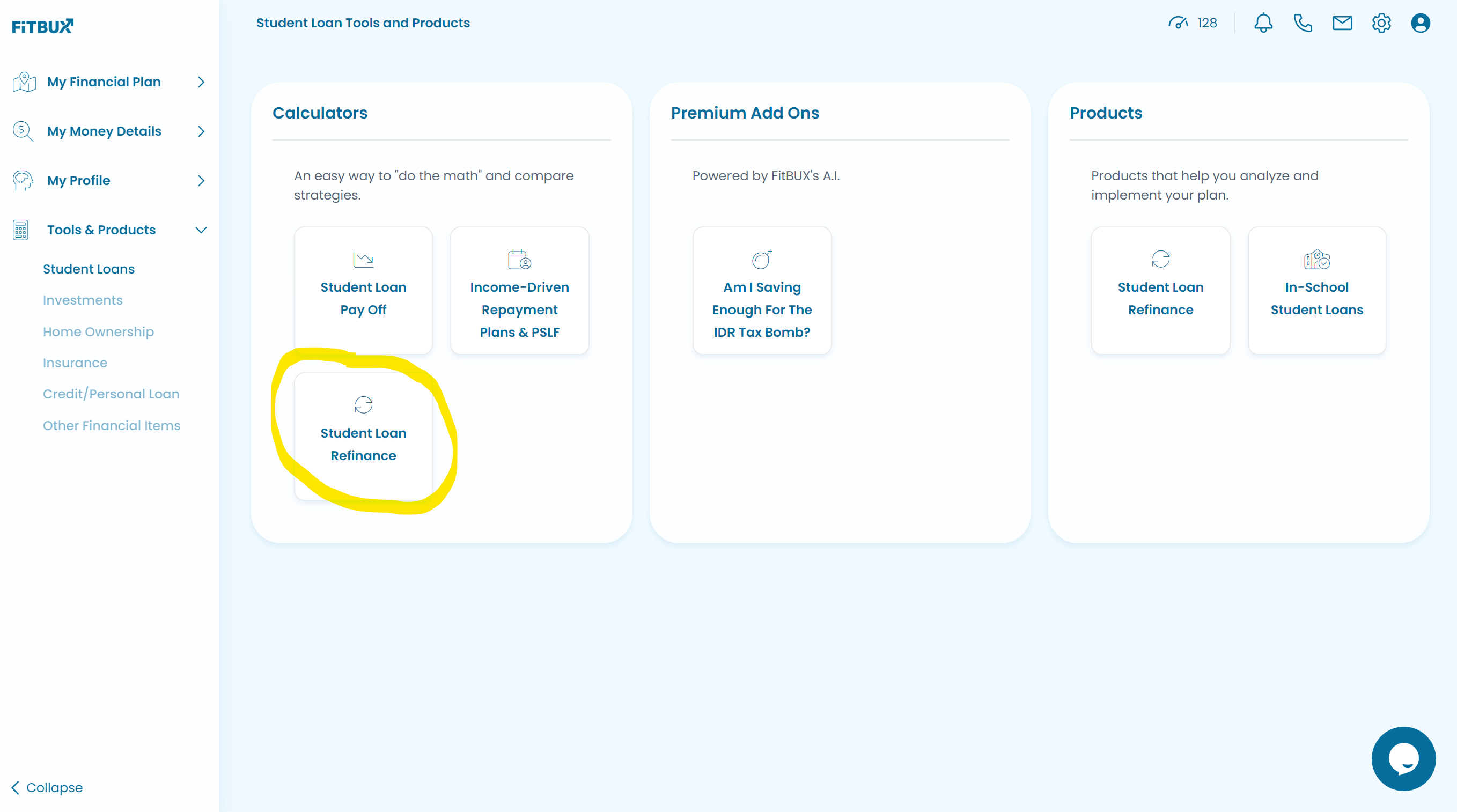

Once your account is created, go to the left side of the screen and click on ‘Tools & Products’ and select Student Loans

Under the calculators section click on ‘Student Loan Refinance’.

Sometimes people are confused and they select student loan refinance under the ‘Products’ section on this page. The section takes you to our partner student loan refinance companies. Some go there first so they can get rates then enter the information into our student loan refinance calculator.

If you need help checking rates and going through these calculations, be sure to check out our free student loan refinance service.

Step 3

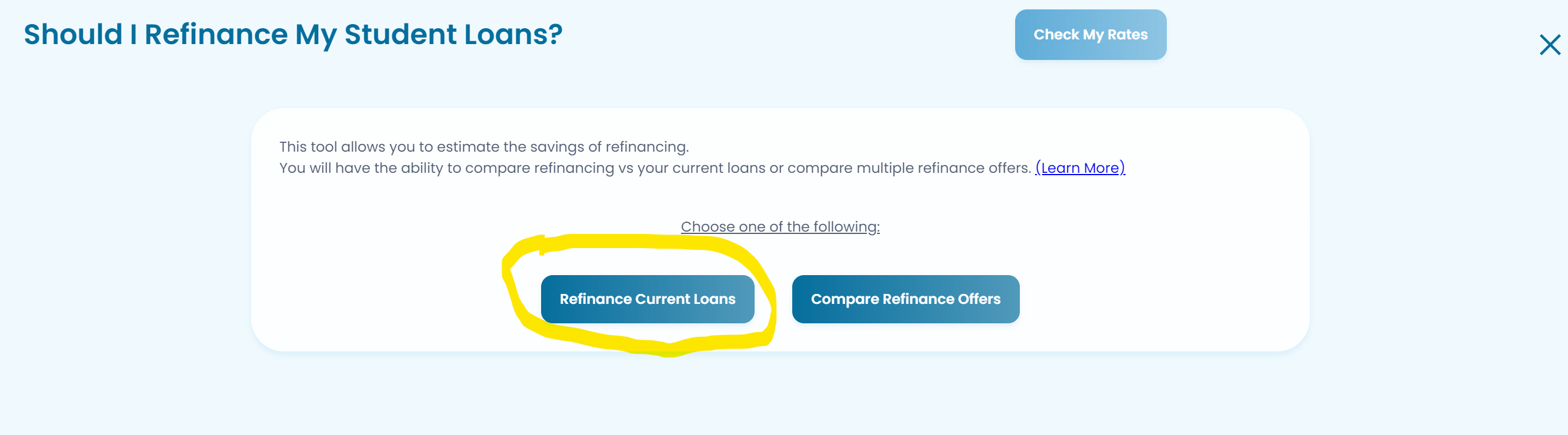

You will be given two options on the next screen: ‘Refinance Current Loans’ or to ‘Compare Refinance Offers’.

Click on the ‘Refinance Current Loans’ option.

Step 4

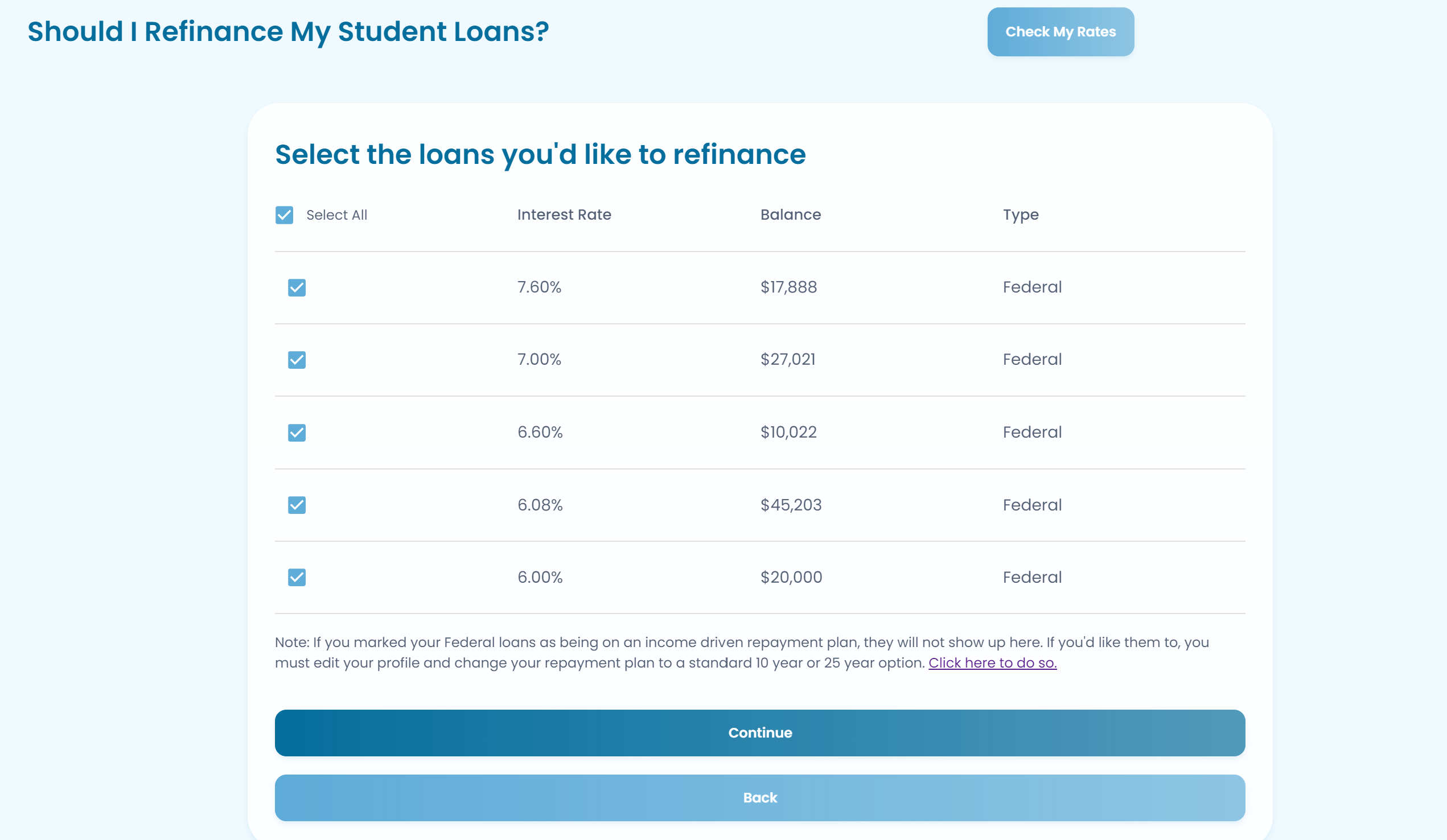

From here, you get to pick which loans that you want to refinance. If for example, if you just want to refinance your three highest interest rate loans, you would only choose those 3 . Click ‘Continue’ when done.

Step 5

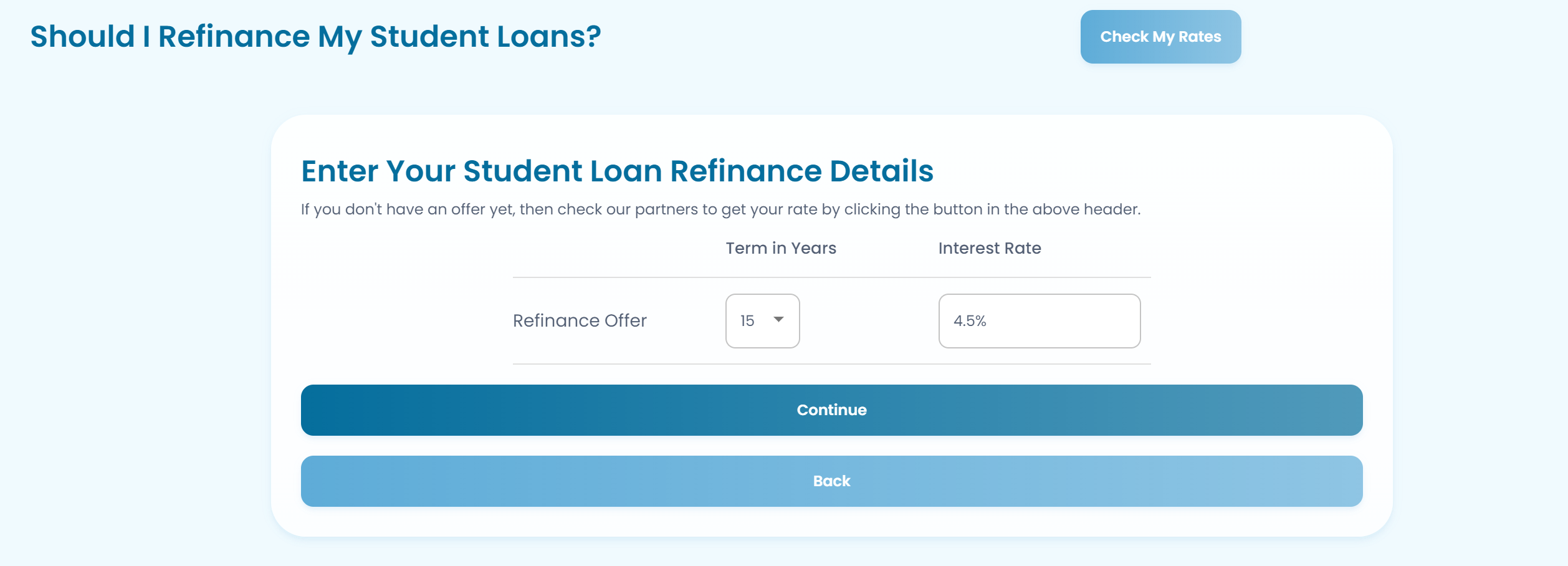

Enter in a refinance offer that you wanted to compare. If you haven’t checked rates, do so using one of the nine best refinance companies.

Click ‘Continue’ once done.

Step 6

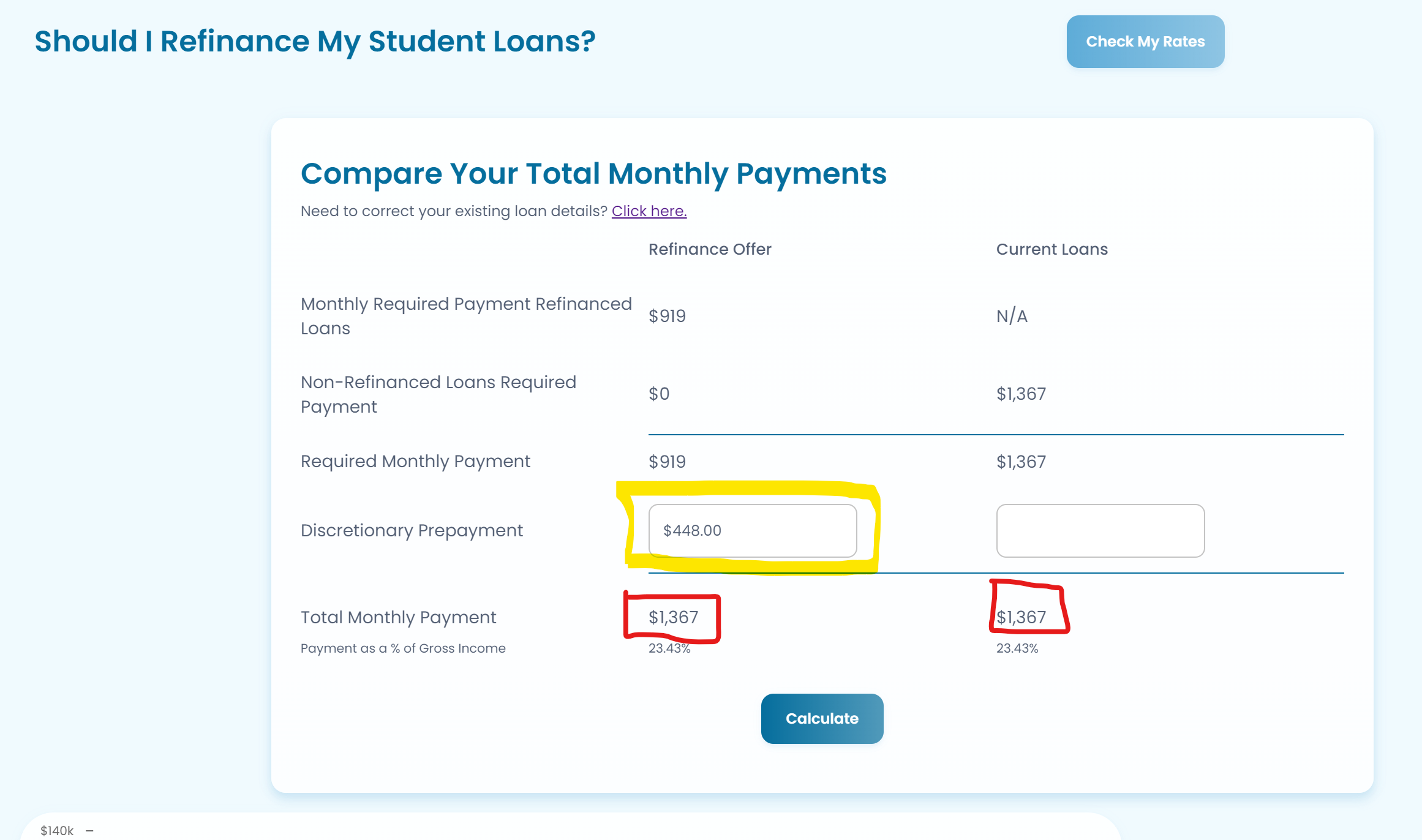

This next screen is where you’ll be able to compare the offers. To do it correctly, you’ll need to make it an apples-to-apples comparison.

To do so, you’ll make the monthly payment equal to each other.

In my example here, I compared a 15 year loan at 4.5%. In the picture below, you’ll notice I took the difference in the 15 and 10 year loan and made that as an extra payment, also known as a prepayment.

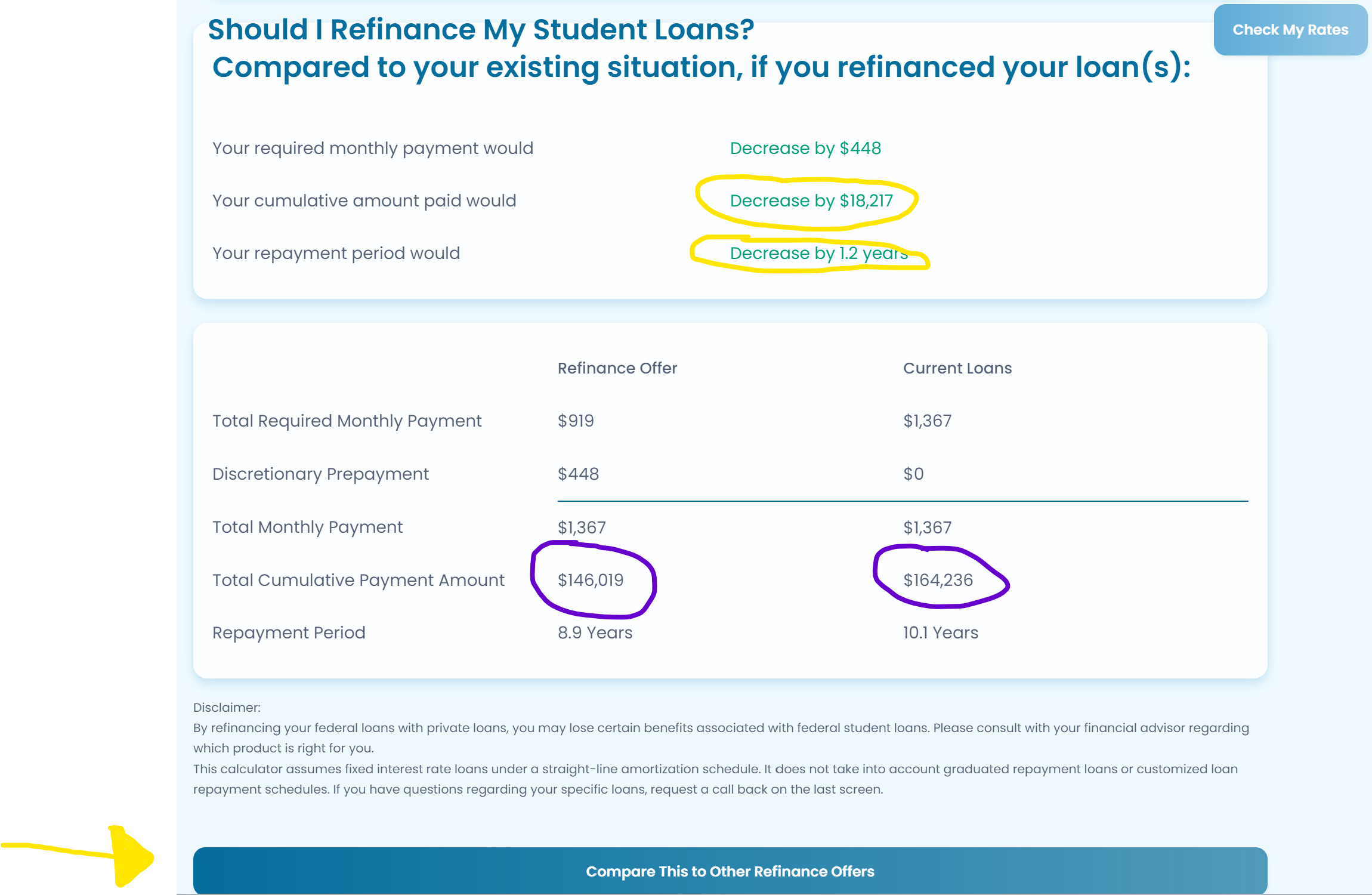

Step 7

Hit ‘Calculate’ and scroll down. You’ll see what exactly how much you’d save along with how quickly it’s paid off.

Comparing Refinance Offers

Below details how to use FitBUX’s student loan refinance calculator to compare two offers.

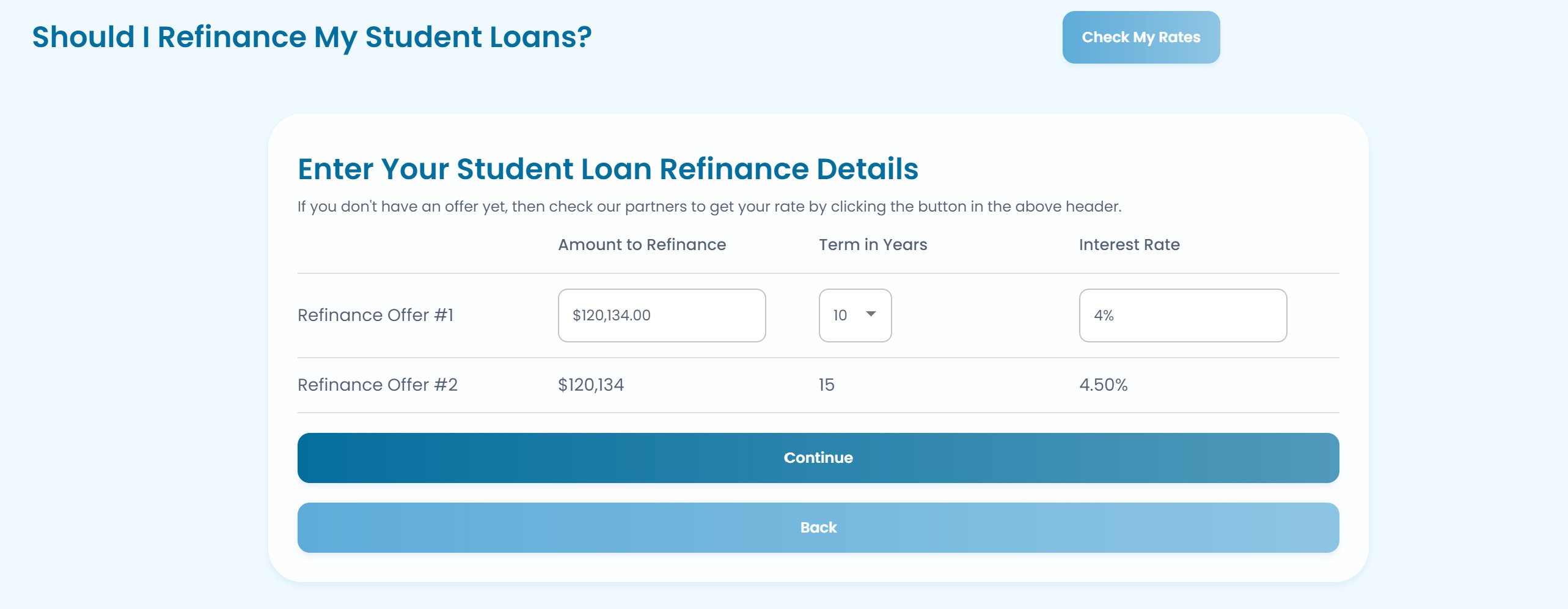

Step 1

On step 3 above you choose ‘Refinance Current Loans.’ To compare refinance offers, instead choose ‘Compare Refinance Offers.’

Step 2

Again, you’ll need to make them apples-to-apples. To do so, you’ll make the monthly payment equal to each other just like you did in step 6 above.

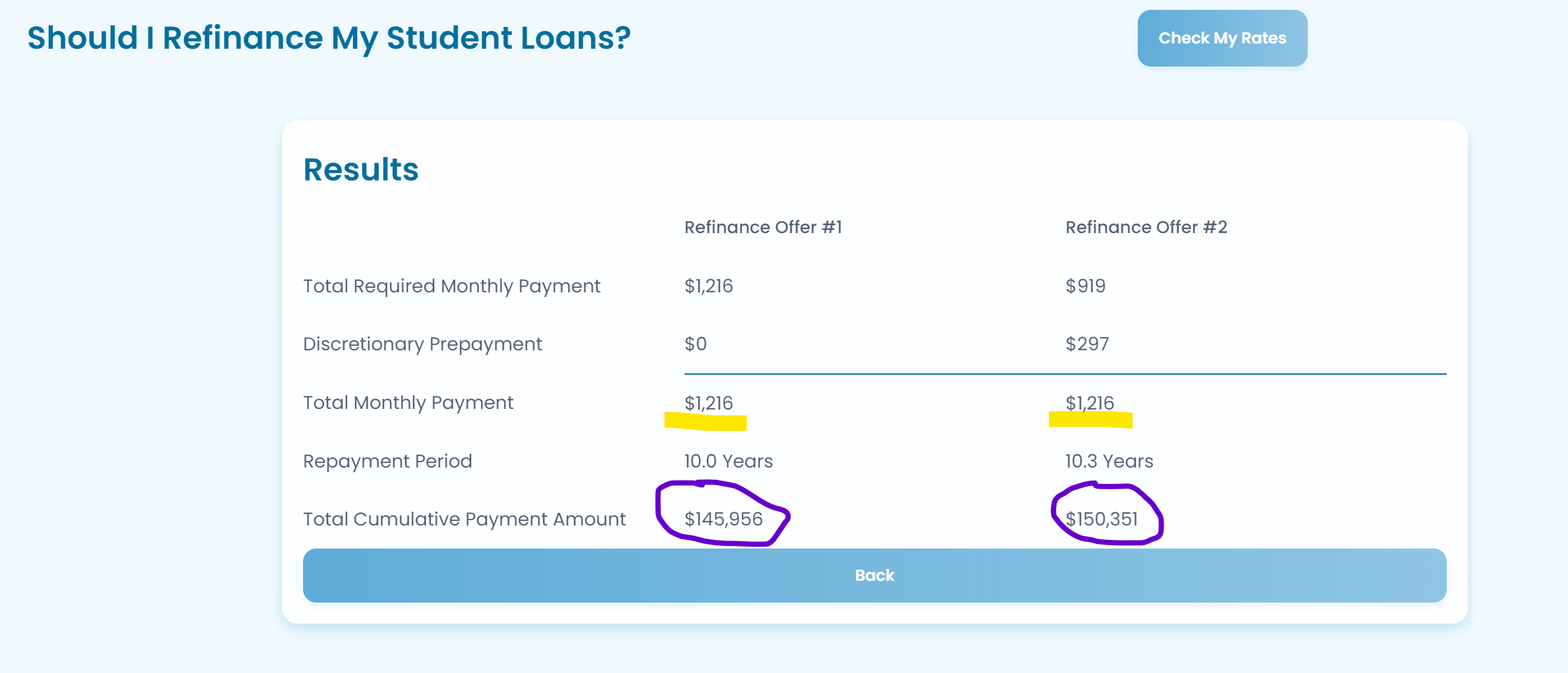

In the example, you’d save about $5,000 for picking the 10 year loan at 4%.

How FitBUX Helps You

Refinancing is a process we’d love to walk you through. We know it can be overwhelming which is why we have our free student loan refinance service.

I also mentioned above you need to determine if you should pay off your loans or go on loan forgiveness before looking into refinancing. We have expert student loan planners you can talk to for free. We call them FitBUX’s Coaches and they will go beyond student loans to help you build an entire financial plan!

By David Hughes and review by Joseph Reinke, CFA