Retirement savings plans are an essential pillar of financial security. As we delve into the world of retirement planning, two terms often emerge at the forefront — Roth 401(k) and Roth IRA.

These vehicles for retirement savings share some similarities but also have distinctive characteristics that can significantly impact your financial future.

This article discusses these two types of retirement savings plans to help you make an informed decision for your retirement years. Let’s embark on this journey of understanding Roth 401(k) vs. Roth IRA and discover which might serve as the best fit for your unique retirement needs.

The Basics

Its a good idea to understand the basics before jumping in a comparison so that is where we will start.

Roth 401(k)

A Roth 401(k) is an employer-sponsored retirement savings plan. Roth 401(k) contributions are made with after-tax income.

Therefore, your contributions do not reduce your taxable income in the year of contribution. However, when you retire, your withdrawals are tax-free.

Roth IRA

Contributions to a Roth IRA are made with after-tax dollars just like a Roth 401(k) and withdrawals in retirement are tax-free as well.

The main differences between these types of accounts are discussed below.

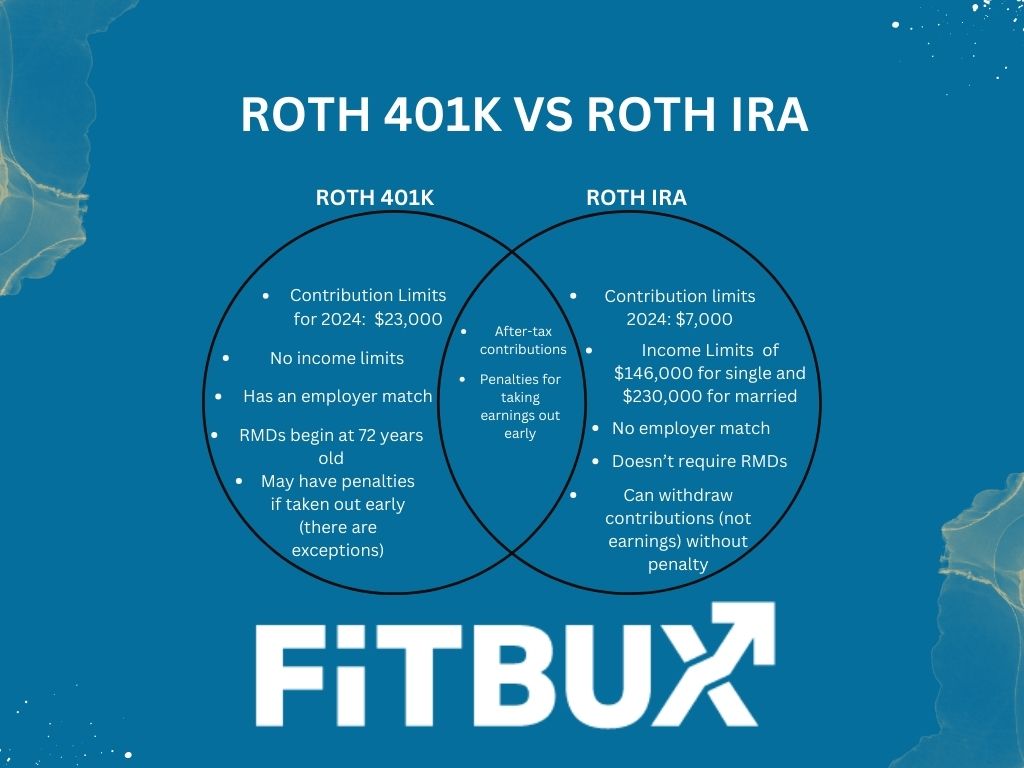

Contribution Limits & Income Restrictions

One major benefit the Roth 401(k) has over a Roth IRA is the annual contribution limit which is important for high-income earners.

The Roth 401(k) contribution limit for 2024 is $23,000, with an additional catch-up contribution of $7,500 available if you’re aged 50 or older. This is significantly higher than the Roth IRA limit, which is $7,000 for individuals under 50 and $8,000 for those aged 50 and older.

Also, Roth 401(k) and Roth IRA differ significantly when it comes to income restrictions. Roth 401(k) plans do not impose income limits, meaning you can contribute regardless of how high your income is.

In contrast, a Roth IRA does have income limits. It’s crucial to check the current restrictions on the IRS website here to ensure you’re eligible to contribute. However, regardless of income, you can still contribute to a Roth IRA via a back-door Roth IRA. It’s just a little more difficult if you are above the income threshold.

Key Points

- The Roth 401(k) contribution limit for 2024 is $23,000, increasing to $30,500 if you’re aged 50 or older.

- The Roth IRA limit for 2024 is significantly lower, at $7,000 for individuals under 50 and $8,000 for those 50 or older.

- Roth 401(k) plans have no income limits, allowing high earners to contribute regardless of their income level.

- Roth IRA does impose income limits, but individuals over the income threshold can still contribute via a back-door Roth IRA.

Tax Advantages and Withdrawal Rules

Roth 401(k) and Roth IRA accounts offer tax-free retirement income.

However, the rules regarding early withdrawal vary between Roth 401(k) and Roth IRA. With a Roth 401(k), if you withdraw your contributions before the account is at least five years old or before you reach age 59½, you may face taxes and penalties.

A Roth IRA offers more flexibility, allowing you to withdraw your contributions at any time without penalty. Note: There is an exception to this if the Roth IRA is from a Roth conversion. If it is, then the 5-year rule is applied.

These differences become particularly important if you leave your employer. Rolling over your Roth 401(k) to a Roth IRA can provide better access to your funds. In addition, Roth 401(k)s are subject to required minimum distributions (RMDs), Roth IRAs are not.

Key Points

- Roth 401(k) and Roth IRA accounts offer tax-free retirement income.

- Early withdrawal rules vary between Roth 401(k) and Roth IRA.

- Roth 401(k) can incur taxes and penalties for early withdrawal unless certain conditions are met.

- Roth IRA offers more flexibility, allowing penalty-free withdrawal of contributions at any time, with a notable exception for Roth conversions.

- Rolling over your Roth 401(k) to a Roth IRA upon leaving your employer can provide better access to your funds.

- Unlike Roth 401(k)s, Roth IRAs are not subject to required minimum distributions (RMDs).

Employer Contributions and Investment Options

Employer matching contributions in a Roth 401(k) offer a significant advantage to employees looking to augment their retirement savings. Under the new federal law, employers are allowed to match the employees’ contributions to their 401(k) accounts using after-tax dollars, similar to a Roth 401(k) mechanism.

This provides a unique opportunity for employees to choose whether their contributions are made with pre-tax or after-tax dollars based on their individual financial circumstances and retirement goals.

When comparing the investment options for retirement, Roth 401(k) and Roth IRA present distinct opportunities. The Roth 401(k) plan typically offers a limited assortment of investment options.

Conversely, Roth IRA delivers a far greater range of investment alternatives, providing the flexibility to tailor the portfolio according to the investor’s risk tolerance and market perspective. Moreover, Roth IRAs can potentially be more cost-effective due to the ability to manage investments yourself, or by leveraging new-age technologies.

Key Points

- Employer matching contributions in a Roth 401(k) significantly enhance retirement savings.

- Under new federal law, employers can match 401(k) contributions with after-tax dollars, mimicking the Roth 401(k) mechanism.

- Employees can choose whether to make contributions with pre-tax or after-tax dollars, depending on their financial situation and retirement objectives.

- Roth 401(k) plans offer a limited range of investment options, whereas Roth IRA offers a wide assortment of investment opportunities.

Financial Expert Opinions

I’m A CFA Charterholder with 20 years of financial management experience. Roth Accounts are awesome because of their benefits. The new law allowing employers matching to go directly to a Roth 401k is a game changer.

It fundamentally alters the retirement landscape by allowing employees to amplify their after-tax contributions significantly. The impact of these changes over a typical working career can be astounding.

Case Study

Let us envision a scenario where a 30-year-old individual starts investing $6,000 annually in their Roth 401(k), with their employer matching their contributions. Under the old law, their employer’s match would go into a taxable account. After 30 years, assuming a 7% average annual return, their retirement nest egg would amount to approximately $800,000 after taxes.

However, the new law allowing Roth 401(k) employer match to be made with after-tax dollars paints a different picture. Now, at retirement, the individual’s nest egg would swell to approximately $950,000 – all of it tax-free. This is a staggering increase of $150,000, a true testament to the power of tax-free growth.

Moreover, upon retirement, one can roll over the Roth 401(k) into a Roth IRA, circumventing the mandatory annual withdrawals that come with a 401(k). This allows the funds to continue growing tax-free, providing a cushion of financial security in the golden years. This practical example underscores the game-changing potential of the new law and the strategic use of Roth accounts in retirement planning.

Which Plan Suits You?

Choosing between a Roth 401(k) and a Roth IRA is a highly personal decision that should consider your current financial situation and long-term retirement goals. Good news though. You can contribute to both a Roth 401(k) and a Roth IRA.

The bigger question is how you should divide up your pre-tax contributions vs your Roth Contributions.

If maximizing retirement savings is your primary objective, contributing to both plans can reap substantial rewards, as it allows you to diversify your retirement income and take advantage of the unique benefits of each especially if you are also offered a Health Savings Account.

This is why you need to make the decision based on your entire financial plan.

For example, if you’re on an income-driven student loan repayment plan, it might be more beneficial to prioritize your pre-tax accounts because it reduces your monthly payments.

On the other hand, if you anticipate being in a higher tax bracket in retirement or foresee significant income from other sources, consider focusing more on your Roth accounts. The tax-free withdrawals in retirement can provide a significant boon, as you won’t be subject to the potentially higher future tax rates.

The decision between a Roth 401(k) and a Roth IRA isn’t a one-time choice, but rather one that should be revisited periodically. As your income, financial obligations, and retirement goals evolve, so too should your retirement savings strategy to ensure it remains optimally aligned with your changing needs and circumstances.

Key Points

- Choosing between a Roth 401(k) and a Roth IRA depends on your personal financial situation and retirement goals. Both plans can be contributed to simultaneously.

- The decision on how to split your pre-tax and Roth contributions should be based on your comprehensive financial plan.

- Income-driven student loan repayment plans may benefit from a focus on pre-tax accounts to reduce monthly payments.

- If you anticipate a higher tax bracket in retirement or expect significant income from other sources, Roth accounts may be more beneficial due to their tax-free withdrawals.

- The choice between Roth 401(k) and Roth IRA is not a one-time decision; it should be revisited and adjusted as your income, financial obligations, and retirement goals evolve over time.

Comparative Analysis

Below is a summary of the pros and cons for each type of account.

Roth 401(k)

Pros:

- Higher Contribution Limits: Allows for larger annual contributions compared to a Roth IRA.

- No Income Restrictions: Accessible to high earners without income limits.

- Employer Match: Potential for employer matching contributions (though in a pre-tax account).

- Automatic Payroll Deductions: Convenient contribution method through employer payroll.

Cons:

- Limited Investment Options: Typically restricted to the choices offered by the employer’s plan.

- Required Minimum Distributions (RMDs): Subject to RMDs, although this is changing in 2024.

- Less Flexibility for Early Withdrawals: More restrictions on early withdrawals compared to a Roth IRA.

Roth IRA

Pros:

- Tax-Free Growth and Withdrawals: Contributions and earnings grow tax-free, with tax-free withdrawals in retirement.

- No RMDs: No required minimum distributions, offering more flexibility in retirement.

- More Investment Choices: Access to a broader range of investment options than a Roth 401(k).

- Withdraw Contributions Anytime: Ability to withdraw contributions (not earnings) at any time without penalty.

Cons:

- Lower Contribution Limits: Annual contribution limits are significantly lower than for a Roth 401(k).

- Income Restrictions: Contribution limits phase out at higher income levels.

- No Employer Match: Contributions are solely from the individual, with no employer matching.

Conclusion

In conclusion, the choice between Roth 401(k) and Roth IRA is multifaceted, with each offering unique advantages based on your personal financial situation and retirement goals. The new law enabling Roth 401(k) employer matches presents an exciting opportunity for amplified, tax-free retirement savings.

However, the Roth IRA offers more flexibility in investment options and potential cost-effectiveness.

Balancing your contributions between pre-tax and Roth accounts will diversify retirement income. The importance of making an informed and personalized decision in choosing the right plan cannot be overstated. Adjustments to your retirement savings strategy should be made periodically, as your financial circumstances evolve.