Understanding the pros and cons of refinancing student loans is an extremely important topic. At FitBUX, we speak to people daily who got bombarded with mailers about refinancing their Federal student loans after they graduated. They didn’t know any better and decided to refinance. Now they are finding out they should have never done it.

This article discusses refinancing pros and cons. To be clear, we are discussing going from your Federal loans to private loans. If you are already in private loans, always look into refinancing and most likely do it. If you need addition help, be sure to read our Student Loan Refinancing Ultimate Guide and check out our Free Student Loan Refinance Service.

Table Of Contents

3 Refinancing Student Loan Pros

Save Money

The #1 one reason to refinance student loans is to drop your interest rate and save money. How much you save depends on the term you choose, the type of loan (fixed vs variable rate student loans), and how you make payments

One key item to remember is the first myth from our 8 myths of student loan refinancing article. You don’t have to refinance all your loans. In fact, most people, especially graduate students, will not want to refinance all loans depending on the rates and/or terms of some of their existing loans.

Also, savings is just one of two items you need to look at when refinancing your student loans. Budget flexibility is the second (See below for details about this).

Lastly, before refinancing, make sure you’re 100% committed to paying off your loans as effectively as possible and as quickly as possible to maximize your savings.

Potentially Lower Monthly Payment

This is a secondary goal of refinancing and, in my opinion, shouldn’t be the primary reason for doing a refinance in most cases.

When you refinance, your interest rate drops. So all else equal to your Federal loans, your required monthly payment will drop. This translates into improved budget flexibility since you could dedicate more funds to other financial needs (saving for a house, paying off credit cards, etc.)

The reason why I say this is secondary to savings is regardless of what your required payment is, you’ll most likely be making prepayments to maximize your savings.

Therefore, the budget flexibility of a lower monthly payment is good but saving the most money is still your #1 priority. Refinancing into a lower rate does save you in and of itself, making prepayments in addition will save you even more of course.

Payments Applied Correctly, Optimizing Your Savings

Prepayments on Federal student loans are often times applied incorrectly. There is often multiple loans with different terms and rates and student loan servicers sometimes don’t bother considering this when applying prepayment. For instance, they may not apply your prepayment to the highest interest rate loan.

This cost borrowers millions of dollars per year. We’ve caught mistakes on roughly 60% – 65% for FitBUX Members using the FitBUX Solution. Government data also shows that servicers make mistakes approximately 60% of the time.

We’ve seen numerous occasions whereby borrowers get so annoyed at their Federal loan servicer they refinance simply so they don’t have to deal with them anymore. Once you refinance, you only have one loan to deal with and private loan servicers typically apply payments correctly. People that refinance for this reason are looking for simplicity and accuracy.

5 Refinancing Student Loan Cons

Losing Budget Flexibility

Many borrowers are enticed to use shorter-term loans because they have lower interest rates relative to longer term loans. However, shorter term loans mean a higher monthly payment, all else being equal.

In fact, most of the savings on a shorter-term loan are a result of the higher monthly payment not the lower interest rate.

For recent graduates who are just getting started in “life”, our general recommendation is to prioritize budget flexibility initially and refinance into a longer term loan until things settle. Then once you have been working a while and understand your budget, you should look into refinancing again into a shorter term loan to maximize your savings.

If you want help analyzing the trade-off between the shorter term loans and longer term loans, i.e. savings vs budget flexibility, then be sure to sign-up and use our free student loan refinancing service.

In addition to losing budget flexibility, refinancing into a short-term loan may make it harder to qualify for a mortgage if buying a house is a priority. When home lenders consider a mortgage application, they will look at your debt-to-income ratio as a key variable. Your DTI ratio is calculated by comparing your monthly gross income and your monthly debt obligations.

Thus, refinancing into a short-term loan hurts you in regards to purchasing a house. This happens because you will be increasing your debt-to-income ratio. Check out this article about buying a house with student loan debt for more information.

No Loan Forgiveness Opportunities

This is one of the biggest mistakes we see new grads make. When you refinance your Federal student loans, you go from a Federal loan to a private loan. This means you no longer qualify for loan forgiveness.

Many individuals that come to us wanted to pursue loan forgiveness via an income-driven repayment plan.

With an income-driven repayment plan, payments are based on your percentage of one’s income which means lower payments. However, the forgiven amount is treated as taxable income at the end of the plan.

So some folks wanting to go on IDR think they should refinancing and secure a lower rate. They believe it will drop their tax obligation when the loan is forgiven.

However, one can not use an income-driven repayment plan for private loans. Therefore, if you refinance to a private loan, you will be “stuck” into a traditional repayment plan and your monthly payments are going to shoot up.

This is even worse for those seeking forgiveness via Public Service Loan Forgiveness (PSLF). We’ve worked with a number of people at non-profits who refinanced not realizing it would disqualify them PSLF. If you’d like to learn more about PSLF, be sure to check out our Public Service Loan Forgiveness guide.

Less Flexibility For Hardship

This is similar to the student loan refinance con above. However, it deals with unforeseen events such as losing your job.

When you are in a Federal loan, you have more flexibility. For example, if you lose your job and have no income, you can switch repayment plans and enter an income-driven repayment plan. Your required payment would go to $0 per month and you wouldn’t be considered in default. You could also go into forbearance.

Once you refinance, you lose the ability to do the aforementioned. Each student loan refinance company has their own parameters. For example, if you lose your job, you may be able to defer your loan payment for 6 months. Each company is different so be sure to check out our student loan refinance company reviews to see what deferment feature each company offers.

In short, if a majority of your income is unstable (such as commissions or bonuses) then refinancing is probably not for you.

One Big Loan

Above, we mentioned some people refinance because they want to have one loan in one place and don’t want to deal with their Federal loan servicer anymore. That convenience comes at a price though.

When you are in your Federal loans, each time you pay off a loan your required monthly payment drops. This gives you more budget flexibility (Note: This is true with every servicer except Great Lakes. You have to manually drop it. For more information about making payments with Great Lakes, check out this Great Lakes Guide).

When you refinance, you are also consolidating your loans. This means you go from having multiple loans to one large loan. Therefore, your required monthly payment will stay the same until you either pay off your loan completely or refinance again into another loan.

If you are unfamiliar with the difference between refinancing and consolidating, I recommend you check out our 4 Things To Know About Student Loan Consolidation article.

Variable Rates Go Up

Another major mistake we see is borrowers who have used variable rate loans. Most shouldn’t use them especially right now because we are in an increasing variable rate environment.

This can be a costly mistake. Those who do not have the ability to repay their loans quickly are most hurt by this mistake. The appeal of variable rate loans is that have an *initial” rate which is lower than fixed rate loans. It’s a “teaser” rate as many borrowers named it.

If you are thinking of refinancing with a variable rate loan, I highly recommend checking out our variable rate student loan refinance guide.

Summary

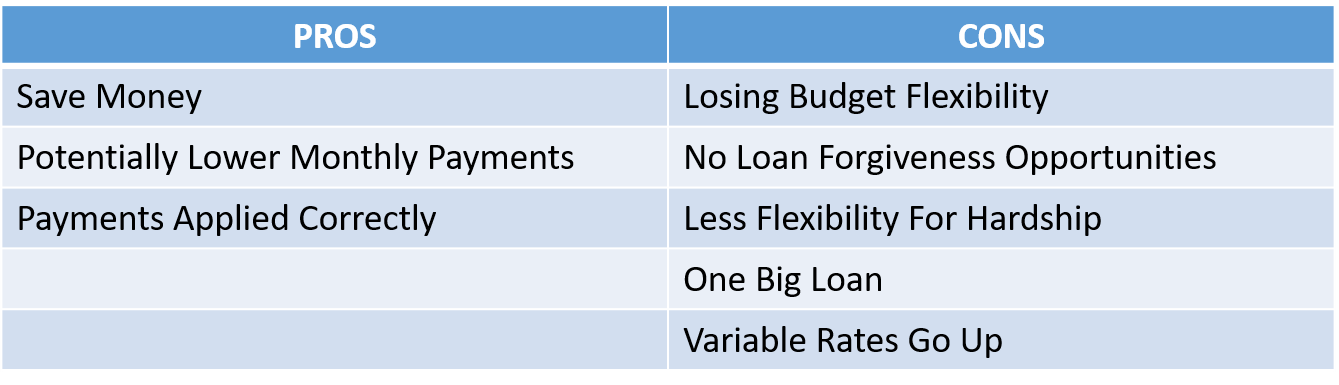

Below is a table summarizing the refinancing student loans pros and cons discussed in this article. If you’d like more articles about money, check out our blog page.

Article By Joseph Reinke, CFA. Joseph Reinke is a Chartered Financial Analyst (CFA) and founder of FitBUX. He holds a degree in finance with an investment concentration. He’s been personal investing since he was 12 years old. Joseph has experience in mortgages, wealth management, investment banking, valuation, and stock and option trading.FitBUX.

We know student loan planners are hard to find.

Our FREE student loan planners have helped thousands of Young Professionals manage and eliminate over $950 million in student loans. We help you develop your plan for free because planning your financial future should not cost you your financial future.

If you would like free expert help deciding if student loan refinancing is right for you, check out FitBUX’s free student loan refinance service.