We all wish we could snap our fingers and be out of debt. Unfortunately, that can’t happen for most of us.

Therefore, we search on Google ways to pay off student loans fast. Instead of getting good recommendations we instead get results like ‘become a dog walker.’

These articles aren’t bad but center more on ways to increase income. They should really be titled how to creatively pay off student loans.

This article is different than the others. I detail below nine real ways to pay off your student loans fast.

I will also debunk two myths that many websites tell you to do which are garbage recommendations and cost you a lot of money!

The good news is we can develop a good plan. With a good plan and the tips below, you’ll be seeing the light at the end of the tunnel.

I’ve included an infographic and video below that summarizes the 9 ways below.

Infographic: Pay Off Student Loans Fast

1. Organizing Will Save You Thousands

How to pay off student loans fast starts with organization!

Most of you will have between 5 and 20 Federal loans and maybe some private loans. They all have different interest rates and loan amounts.

You’ll want to organize these either in a computer program like Excel or in an online software such as your FitBUX profile. (Note: The benefit of doing it using an online software like FitBUX is having the data automatically feed into our student loan pay off calculator. Whereas, if you do it via Excel you’d have to create the calculators yourself.)

Organizing your loans gets you prepared to do two things:

- Decide if you’d like to pay off the highest interest rate loans first or the low balance loan.

- Know which loans to potentially refinance.

I discuss both of these topics in detail next.

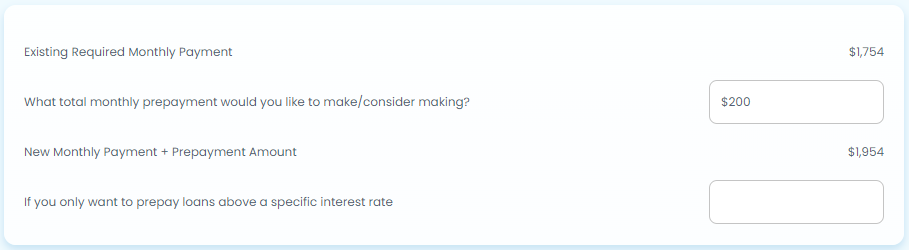

2. Know The Difference Between Required Payments & Prepayments

This is a must-know when it comes to paying off student loans fast!

Required Payment

Each month you have a required payment. Keys to understanding the required payment are:

- You have to pay this every month;

- You have no say on the amount; and

- Most importantly you have no say on how the money is allocated. For example, if you want to pay off the highest interest rate loans first, you can’t do that with your required payment.

Prepayments

This is an amount you pay in addition to your required payment. The purpose of prepayments is to pay off student loans faster and save money.

The cool thing about the prepayment is you decide:

- When you do it;

- How much you do; and which loan it goes to. Therefore, if you want to use your prepayment to pay off the highest interest rate loan first, you can!

Two items that we see people get confused on that are worth noting here:

- Interest must be paid first before targeting principal. Therefore, if you make a prepayment, the interest that is accrued on all your loans must be paid first then what is remaining can be directed at the loan of your choice.

- A prepayment does not replace your required payment. Let’s say your required payment is $500 a month. We constantly see people make a $1,000 prepayment and think since they paid $1,000 they don’t have to pay the $500 required payment. That is incorrect. You still have to pay the $500!

3. The Biggest Trick + Prepayments

Now that you have your loans organized and you know the difference between required payments and prepayments the fun can begin.

This is one of the biggest tricks to pay off your student loans fast.

Let’s keep it simple. When it comes to payments, required payments I don’t like. Prepayments I do like.

Therefore, is there a way to drop my required payment on my Federal loans so I can free up money to make prepayments? The answer is yes!

Most of the time when you compare a long-term loan to a short-term loan the interest rate is higher. For example, a 30 year mortgage has a higher interest rate than a 15 year mortgage.

With Federal student loans, that isn’t the case. This blunder by the government allows you the borrow to save money!

Instead of using the standard 10 year repayment plan, you can extend the loans to 25 years if you owe more than 30k. If you do not owe more than 30k you can do this same trick using the graduated repayment plan or potentially an income-driven repayment plan.

When you extend your loans to 25 years, your required payment drops. This frees up more money to make prepayments which you can use to target your highest interest rate loans.

The best strategy to do this with is REPAYE. However, its also extremely complex. If you want to look more into that, I detail exactly how to use the REPAYE interest subsidy to your advantage and pay off your student loans faster in this article.

4. Prepay Often

Many people make prepayments at the same time as their required payment. However, interest is charged and accrued daily.

Therefore, the longer you wait the more of your payment goes to interest instead of reducing how much you owe.

It can be frustrating when you first start. It will feel like you are making no progress. The amount you owe will appear as though its not decreasing. However, that is just a function of how loans work.

The balance does not drop in a linear fashion over time. In the beginning, it will slowly drop. Then you will see it drop faster and faster as you make more payments payments you make.

The moral of the story is the more often you make prepayments and the bigger they are, the sooner you’ll see meaningful decreases in how much you owe. If you’d like to learn more, check out this video on how a loan works.

5. Don’t Let Loan Servicers Screw You

Its no secret, loan servicers suck. We see them make two huge mistakes that can cost you thousands. Not only that, but these mistakes prevent you from paying off your student loans faster.

Loan Servicer Mistake #1

The first item I told you to do was organize your loans. As a refresher, most of you will have between 5 and 20 loans.

Your loan servicer tells you what your required payment is. What they don’t explicitly tell you is each one of your loans has a required payment.

The required payment they show you is a summation of each of the individual loans required payments.

This is extremely important to know because when you pay off one of your loans, that required payment is gone.

Therefore, your overall required payment drops. This in turn frees up more money for you to prepay each month to the next loan you are targeting.

However, most loan servicers do not automatically drop the required payment. You have to call and tell them to do it.

Yes, its a pain to call. However, it will help you pay off your student loans a lot faster!

Loan Servicer Mistake #2

You are doing the right thing making prepayments. Even though you tell your loan servicer which loan to prepay, they don’t always do it.

Often times, they take the prepayment and apply it to all your loans. You want the prepayment going to a specific loan.

This happens so frequently that we’ve included a new technology in FitBUX’s premium membership. Members can now make prepayments directly from their FitBUX profile to the loan servicer. The biggest part is that the technology makes sure they are applying the money correctly!

6. Do Not Consolidate Your Federal Loans

If you are staying in your Federal loans, do not consolidate them. If you do, you can no longer target specific loans and take advantage of the aforementioned tricks. Again, if you are trying to pay off your student loans fast, consolidating will slow you down.

Two items to note:

- Consolidation is not the same thing as refinancing. Sometimes when you refinance you also consolidate. I discuss this more below.

- The only time you want to consolidate is if you have to in order to take advantage of a new repayment plan. However, this only makes since to do for a small number of borrowers.

7. Setting Up Auto-Pay

One of your goals of paying off student loans fast is to save as much money as possible…obviously…

On all Federal student loans and most private loans, you can hook up your bank account to automatically make your payments each month. This is called auto-pay and you’ll get a 0.25% discount for doing it… Take advantage of that!

What you’ll want to do is set up auto-pay for the required monthly payment each month. Then when you’re ready to make a prepayment, log into your loan servicer’s website and make the extra payment. As I previously mentioned, you can also sign up for FitBUX’s premium membership and make the prepayments straight from your FitBUX profile.

8. Refinancing

Refinancing is when you go to a private lender and ask them if they will give you a lower interest rate on your loans. If they say yes, then you are replacing your old loan with a new loan. The whole point is to save money and pay off your student loans faster.

However, when it comes to paying off your loans faster, you may not want to refinance or you may not want to refinance all your loans.

When you go from a Federal loan to a private loan you will give up some benefits. You must weigh the savings versus what you are giving up. One of the biggest mistakes people make is not calculating the appropriate amount of savings from refinancing. Thus, you end up making a major mistake.

If you want more info about refinancing, here are additional resources:

- FitBUX’s free student loan refinance service

- Our student loan refinance guide

- 10 best student loan refinance companies

9. Avoid Horrible Advice From Other Sites

There are two recommendations to paying off student loans fast that I see other sites make. These absolutely make me cringe.

Pay Off Capitalized Interest

No, no, no…. Capitalized interest is assigned to each loan it accrues. If you are going to make a prepayment still target one loan. If you are in this situation, such as being a new grad, I dig much deeper into how you should pay off capitalized interest in this article.

Stick To The Standard Repayment Plan

I detailed above why this makes no since to do. Its very clear the people writing this articles for finance blogs are hired individuals that don’t know very much about money.

With that said, there is only one time where it makes since to stay on the standard plan with Federal loans. Behavior. If you drop your required payments and you know you aren’t going to make prepayments, then don’t use the tricks I mentioned above.

#1 Mistake To Avoid

You must decide if you are going to pay off your loans or go for loan forgiveness via income-based repayment plans. We see people all the time make the mistake of choosing one then realizing they need to switch plans. This cost thousands of dollars.

For example, let’s say you owe $150,000 and decided to pay $1,000 per month. Over the first year of repayment, you figured out that your loan balance wasn’t going down. Therefore, you decided that paying $1,000 a month was a waste of money because it wasn’t doing anything so you switched to a loan forgiveness plan.

If you had started on the loan forgiveness plan, your monthly payments would’ve been $400 a month for example. That means in the first year, you could’ve been paying $600 less a month.

In other words, if you would’ve gone on the right plan from the beginning, you would have $7,200 more in your pocket at the end of the first year.

Sadly, people often times don’t realize they made a mistake in the first 12 months. It may be 3, 4, or 5 years before you realize it! The amount you would cost yourself adds up quickly.

I know it can be overwhelming trying to decide if you should pay off student loans or go for forgiveness. However, I wanted to make you are aware of our free FitBUX Membership whereby you can build a profile and speak to an expert student loan planner. We’ve helped 1,000 make the decision. We can help you too.

Would this strategy also apply if we are seeking forgiveness or would that be a different approach?

It would be a different approach because you are seeking forgiveness.

This is perfect. I can’t believe how many bad articles I had to read before I found this one. It actually has tangible things I can do. Thank you.

The amount of garbage out there is amazing.