For the past six years, FitBUX has been helping new grad occupational therapist navigate student loans and build financial plans to achieve their lifestyle goals.

The following article provides data that we’ve collected for occupational therapist salaries and student loan debt. In addition, it analyzes the real life impact that education costs have on the bigger financial picture for occupational therapist.

We also analyze the impact of getting your OTD/MOT relative to your income. The purpose is to answer the question: Is the OTD/MOT worth it?

The occupational therapy salary and student loan data is based on over 1,000 OTs throughout the country that our FitBUX Coaches have helped.

What Is The Entry Level Occupational Therapist Salary?

The average new grad occupational therapist salary on FitBUX is $64,450. The 75th percentile occupational therapist salary is $73,000 and the 25th percentile is $59,500.

We consider new grads as anyone who graduated within the past 5 years.

What Is The Average Occupational Therapist Student Loan Debt?

The average for Occupational therapist on FitBUX is $134,000.

The average interest rate on this debt is 5.68%. Using the standard 10-year repayment plan, the required monthly payment with a balance of $134,000 would be $1,466.

Is It Worth Being A Occupational Therapist? The Traditional Way Of Answering This Question

I’ll start with the traditional way of analyzing this question. It is a flawed method because it doesn’t take into account income characteristics.

However, I start here because this is where most people start. Its good to see this method and its flaws so you can make a good decision or be confident in the decision you’ve already made.

This method starts by analyzing being an OT in isolation of other professions. Then I combine that with various levels of student loan debt to analyze the impact to an Occupational therapist’s financial outlook. For example, what is the impact on things such as retirement and buying a home with student loan debt.

To perform this analysis, we ran six simulations using our new financial planning technology. Below are the results of those simulations as well as explanations.

Simulation Inputs

For each of the simulations we used the following assumptions:

- Average age of a new grad Occupational therapist on FitBUX is 28 years old. Therefore, we started our simulation at 28 and assumed a retirement age of 65 years old.

- We ran three simulations assuming individuals are pursuing a student loan pay-off strategy and three simulations that they are pursuing loan forgiveness via an income-based repayment plan.

- For each of the simulations, we assumed an occupational therapist salary of $64,450

- Starting student loan levels were $64,450, $134,000, and $193,000. The later two amounts represent the mean and 75th percentile of debt from FitBUX. $64,450 is the “optimal” amount of debt. Traditionally, in the finance world the optimal amount of debt is to graduate with a 1:1 ratio of total student loan debt to annual income or less. Thus, the average salary of $64,450 a year yields an optimal total student loan debt amount of $64,450.

- The simulations ran assumed the Occupational therapist was not married.

- On average, we see that unmarried Occupational therapist can designate 30% of their gross income to a combination of building assets (investments) or paying off debt.

- For the pay-off simulations, we assumed 27% of gross income would be used to pay-off student loans and 3% towards retirement investments.

- For the income-based repayment simulations, we assumed the minimum required payment was made on student loans (7.0%), 10% going towards retirement investments (401k and Roth IRA combination), and 13% invested in taxable asset investments.

- We assumed a 3% matching contribution for retirement funds. This is the average matching contribution that we’ve observed for Occupational therapist. We also assumed an annual investment rate of return of 5%.

- We assumed the individual is following the FitBUX financial planning method whereby as their income increases the amount contributed increases to assets and debt based on allocating 30% of their gross income to these categories. We assumed a 3% gross income increase per year.

Results Of Simulations – Pay Off

Below is a summary if you tried to pay off your student loans:

$64,450 in student loans: You could have $3.375 million at retirement, 99% probability of retiring without running out of money, and $233k in assets in 10 years.

$134,000 in student loans: You could have $2.840 million at retirement, 95% probability of retiring without running out of money, and $93k in assets in 10 years.

$193,000 in student loans: You could have $2.395 million at retirement, 72% probability of retiring without running out of money, and $66k in assets in 10 years.

All three simulations result in a significant amount of assets at retirement age. They all have result in the ability to have over a 70% probability of not running out of money in retirement.

However, the only simulation that would give Occupational therapist the ability to pay off student loans quickly, save for retirement, and potentially save for a larger purchase such as a home is the $64,450 in student loan scenario.

The other two scenarios result in having between $93k and $66k in assets after 10 years. However, most of those assets would be in the form of retirement assets and include the retirement match.

Thus, you would have to make a choice between saving for retirement and getting your retirement match or saving for a down payment on a house.

In addition, even if you saved for a house, it would be hard to afford a mortgage payment and a student loan required payment.

Therefore, if you have $134,000 or more in loans it would be extremely hard to afford a house in the 1st 10 years post-graduation and pay off your student loans.

Results Of Simulation – Income-Based Repayment

Income-based repayment plans limit your required monthly payment to a percentage of your income. Long story short, for most people these required payments will be lower than pay-off strategies. Therefore, you can save more money from your pay check today.

The long-run effect of IBR relative to pay-off strategies is that they have the potential to give you more assets especially as you increase the amount of student loan debt you have. They also give you much more money in the short-run.

Therefore, one can buy a house and save for retirement sooner but the trade-off is having student loans for the next 20 years.

$64,450 in student loans: You could have $2.99 million at retirement, 98% probability of retiring without running out of money, and $245k in assets in 10 years.

$134,000 in student loans: You could have $2.81 million at retirement, 94% probability of retiring without running out of money, and $245k in assets in 10 years.

$193,000 in student loans: You could have $2.73 million at retirement, 93% probability of retiring without running out of money, and $245k in assets in 10 years.

Is It Worth It To Be A Occupational Therapist? The Optimal Way Of Answering The Question

The above method of answering the question looked at dollars and cents. However, it is flawed because it doesn’t include the risk of your income.

For example, an Occupational therapists salary has a lot less risk than a real estate agent or someone with only an undergrad degree.

Therefore, the proper way to do an analysis is to factor in risk. The way we do that in finance is to look at human capital.

In short, your human capital is how much your future income is worth today and the analysis of human capital factors in risk to your income.

Thus, we can look at the value of your human capital with your OTD/MOT vs other options. For example, you can compare it to just being an undergrad or relative to another profession such as an DPT, SLP, PA, etc…

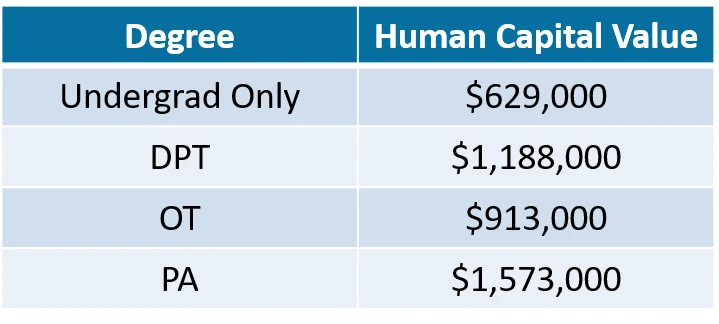

Below is a chart of human capital by profession:

How To Interpret This Analysis – Advanced vs No Advanced Degree

This analysis incorporates everything, i.e. Occupational therapist salary, the risk to that salary, etc… We’ll first compare it to not having an advanced degree then we’ll compare it to other advanced degree options.

After getting a MOT/OTD, the average Occupational therapists will have a human capital value of $913k. An average undergrad only has a human capital value of approximately $629k.

From a finance perspective, you would say that the OTD/MOT is worth it as long as you don’t have to spend more than $343k to get it ($343k is the difference between the human capital values).

However, we always want to see a return on investment. Therefore, let’s say our target is to get a 3x return on the time we invest into getting the OTD/MOT.

You should be willing to pay approximately $114k for your degree ($343k divided by 3). A few big keys to this analysis:

- $114k is not the amount of debt you would be willing to get. Instead it represents the cost you would pay. Debt is just one way to pay and is not an explicit cost.

- The $114k does not include the cost of getting an undergrad degree because you’ve already attained that.

- The cost that do go into the $114k are:

- Tuition

- Books

- Interest on debt

Debt Is Not A Cost

Notice we didn’t say debt is a cost, simply the interest. The reason for this is that you borrow money for tuition and books. Therefore, we’ve already incorporated tuition and books. Plus you could pay cash for tuition and books without taking out debt.

You’ll also notice we don’t include items like rent and food. The reason being is that you would be eating and renting regardless of going to school or not.

The only thing you may be forgoing while in school is a job. Therefore, interest you are charged on the money you borrow to cover living expenses is the true “cost” of forgoing income now to get your OTD/MOT.

In summary, most OTD/MOT programs cost less than $114k. Therefore, when you look at the level of income you receive (i.e. Occupational therapist salary both today and growing over time) and the lower risk to that income relative to just having an undergrad degree, then yes in our opinion is absolutely worth it.

The key for you to determine if it’s worth it is to say what type of return do you want on your investment. If you love being a OT and wouldn’t want to do anything else, then maybe a 2x return would be worth it which means you’d be willing to pay $172k.

How To Interpret This Analysis – Advanced vs Advanced Degree

In reality, all OTs are extremely smart. Very few people that we meet and are thinking of getting their OTD/MOT are saying to themselves, “I’m going to get my OTD/MOT or I’m not going to get anything at all.”

Instead, you have many options such as becoming a DPT, SLP, MD, PA, NP, etc…

Every one of these professions takes longer or shorter to complete, has different levels of income, different employment levels, etc…

In addition, you can’t say “Is a MOT/OTD worth it?” when comparing it to other advanced degrees.

Instead, you’d have to say which degree from a financial standpoint increases my human capital the most and gives me the biggest return on my investment.

In the chart from the previous section, we only included two other professions as examples. As you can see the DPT is better from a financial perspective than an MOT/OTD. This is because most OTs are about the same age as DPTs when they graduate but receive lower average salaries and employment opportunities.

On the flip side of that, PAs create a tremendous amount of human capital. Although employment is slightly worse than MOT/OTDs, it is offset by other factors such as taking less time to graduate (this means PAs are earning income sooner than OTs) and they also have much higher starting salaries.

Conclusion

In all, OTs are in the middle of the pack when it comes to being compared to other degrees.

If you’d like to see the value of your human capital, join FitBUX at https://www.fitbux.com. Once you complete your profile, click the net wealth option on the left hand menu.

By Joseph Reinke, CFA