Income driven repayment, or IDR, is the term used by the government to describe five loan repayment plans. They are:

- Revised Pay As You Earn (REPAYE)

- Pay As You Earn (PAYE)

- Income Based Repayment (IBR)

- Income Based Repayment For Old Borrowers (Also IBR)

- Income Contingent Repayment (ICR)

Many websites have income driven repayment calculators. However, most are flawed because:

- They make it hard to compare options, and

- They don't allow you to look at the impact to a holistic financial plan.

We saw these flaws and fixed them. The result is:

- Our income driven repayment calculator that includes an IDR payment calculator and IDR tax bomb calculator. This calculator allows you to dive deep into the assumptions of IDR.

- Our financial planning technology that includes all the versions of income driven repayment plans. This option allows you to build an entire financial plan incorporating income-driven repayment plans.

Both of the above include all the calculations in one tool and they allow you to compare IDR plans to pay off strategies.

Before using our income driven repayment calculator, I highly recommend reading our IDR guide. If you'd like to watch a video version of this article, click the video image above.

Two Important Notes Before Starting

The Income Contingent Repayment plan is not part of our calculator or financial planning technology. The reason why is we believe there is absolutely no reason for you to use it. Therefore, we have excluded it.

The other item to note, we do not discuss public service loan forgiveness (PSLF) in this article. The reason is PSLF is not a repayment plan. It is a feature of the income driven repayment plans. Therefore, we have an entire article that is 100% dedicated to our PSLF calculator.

How To Use Our Income Driven Repayment Calculator

Below is a step by step guide to using our IDR calculator. If you have questions be sure to sign-up for our student loan webinar (The webinar schedule is coming out soon!).

Step 1: Building Your Profile

To use our income driven repayment calculator, sign-up for a FitBUX membership. Creating your profile is essential to getting customized results that are tailored to your situation.

The profile should only take 3 – 5 minutes to create. The more details you include the more accurate our tools will be.

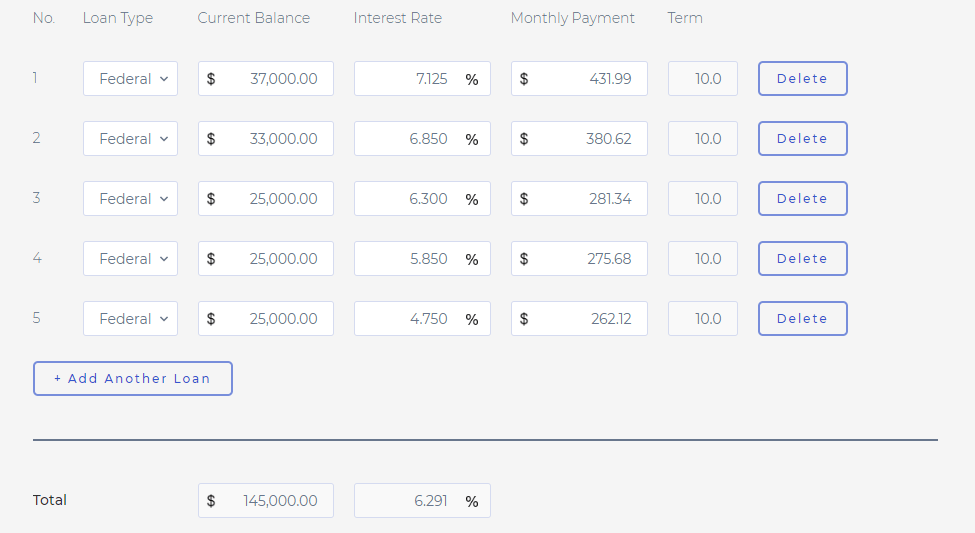

Step 2: Enter Your Student Loan Details

This is one way we customize our income driven repayment calculator to your situation.

It is extremely important because each loan you have has a different interest rate. Therefore, the interest charge varies for each loan.

Thus, the results will be different in the income drive repayment calculator if put all you loan details into your profile relative to if you just use one large estimate of the loan balance and interest rate.

To include all your loans, take the following steps:

- After you build your profile you will be taken to your FitBUX dashboard. Click My Profile from the menu on the left.

- Then choose Accounts.

- Under Debts, you’ll see your Federal loans from when you built your profile. Click Edit.

- If you did not enter your loans while building your profile, click Add Manual Account. If you have signed up for our premium membership you can link your loan accounts to FitBUX and the data will automatically update in your profile.

- You’ll see one loan currently on this screen. Delete it and enter all your loans.

Step 3: Accessing The Income Driven Repayment Calculator

On the left hand side of your profile, click the link that says Tools & Products.

Then select Student Loans. To enter our income drive repayment calculator, choose the option that says Income-Driven Repayment Plans & PSLF.

As previously mentioned, this tool includes:

- A REPAYE calculator

- A PAYE calculator

- An IBR calculator

- A PSLF calculator

- A method of comparing IDR to Paying off your loans.

- An IDR payment calculator whereby you can estimate what your monthly payment will be

- An IDR tax bomb calculator to estimate what you tax liability will be when your loan is forgiven.

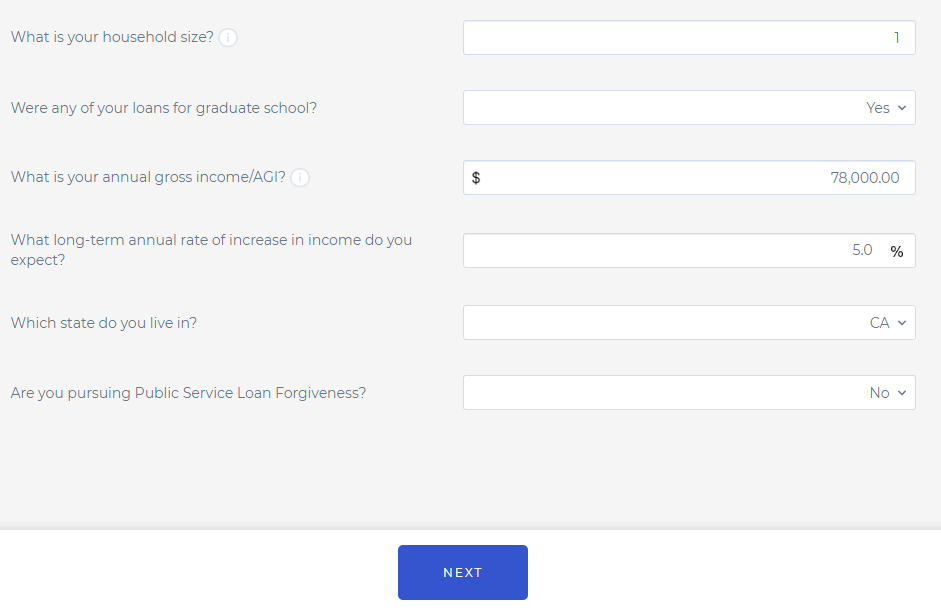

Step 4: Entering Assumptions

Once you open the income drive repayment calculator, you’ll be asked to complete a list of assumptions. These assumptions are extremely important.

The reason they are so important is that they have a big impact on your monthly payment and how much interest you defer. This will impact the IDR payment calculator and the IDR tax bomb calculator. In fact, these inputs have a tremendous impact on your estimated tax liability.

Your household size includes you, your spouse, and children.

For the question, “What is your annual gross income/AGI?” you can use one of two numbers:

- Gross income: This is how much money you make before deductions. Using this number will result in a lower estimated tax liability relative to choice 2 below. You would want to use this figure in the income drive repayment calculator if you are trying to keep it simple and deciding if you’d like to pursue loan forgiveness or do a pay-off strategy instead.

- Adjusted Gross Income (AGI): Using AGI will result in a more accurate estimation of the tax liability relative to option 1 above. The reason being is the government actually uses your AGI in the calculations for your monthly payment, not your gross income. AGI is also called discretionary income.

For your expected long-term annual rate of increase in income, we default to 5%. We do this because the Federal government’s calculator defaults to that. However, 5% is a horrible assumption for most professions.

We recommend reducing the rate of increase assumption to 3%. This will result in a higher expected tax estimation on the IDR tax calculator which is a more conservative approach. We like conservative so there are fewer surprises in your financial journey.

Public service loan forgiveness is a feature of income driven repayment plans. If you work full-time at a non-profit you can select Yes. You can read our public service loan forgiveness guide for more information. Also, we have a special article detailing our public service loan forgiveness calculator that you can check out.

After you input these assumption click the “Next” button.

Step 5: Understanding The Results

Our income drive repayment calculator displays customized figures on the 4 income driven repayment plans. The figures are customized from the information on your FitBUX profile and the assumptions you entered into the calculator on step 4.

The first column represents your estimated monthly payment as of today. The second column is what your estimated monthly payment would be in the last year of your plan. Column one and two represent our IDR payment calculator.

The first column represents your estimated monthly payment as of today. The second column is what your estimated monthly payment would be in the last year of your plan. Column one and two represent our IDR payment calculator.

The third column, Total Paid, is all your monthly payments added up over the entire repayment period. This is where the government’s calculator stops and this is why so many people make the mistake of going on income driven repayment plans to begin with.

The mistake is that they compare the cost displayed under the Total Paid column to the total cost of a pay off strategy (a standard 10 year or 25 year repayment plan). For most, the cost will be significantly lower for the income driven repayment plan if you stop here.

However, you have to 1) factor in the tax and 2) compare the proper time period.

To estimate your tax obligation, you first have to estimate what amount of loans you will have forgiven. Our income driven repayment calculator provides that estimate for you under the Amount Forgiven column.

We then assume a 35% tax bracket. As a side note, our premium members can change the estimated tax obligation once they begin tracking their financial plan.

The next column is how much you would pay in total. This column adds the Total Paid Without Tax column and the Tax Obligation column together.

Note: Many have asked us if our calculator takes into account the REPAYE interest subsidy. Yes, it does!

IDR Calculator In A Financial Plan

Two major issues in the financial services industry are single point solutions and costs.

Single point solutions occur when a calculator or service helps you with only one area of your money.

For example, our income driven repayment calculator is great in showing all you need to know about IDR. However, you most likely have bigger questions. Questions such as:

- Which strategy, loan forgiveness or paying off my loans do I follow?

- If I go onto IDR how do I save for the tax?

- What is the impact of student loans on buying a house?

- Should I invest or pay off my student loans?

- What happens if I’m on IDR and I get married?

- and the list goes on and on.

Our financial planning technology answers these questions for you and is designed for 20 – 40 year olds. Also, it solves the second problem of cost because its free to use!

The financial planning technology includes the income-driven repayment calculator. In addition, you can build multiple plans and compare your options. One last item to note, if you need help you can schedule a call for free with an expert FitBUX Coach.

Implementing Your Plan & Saving For The Tax

Now that you know what your estimated tax liability will be, you need to develop a plan and implement it. Therefore, you need to know the minimum amount you need to save each month. We call this your “required minimum monthly savings amount.” You also need a way to implement the plan because the estimated tax liability will change over-time.

If you want an easy way of doing this, FitBUX’s premium membership makes it easy.

FitBUX’s technology provides you with a recommended minimum amount to save each month and update your progress towards your tax liability in real-time.

Saving For The Tax

We highly recommend setting up an account (bank account, online savings, investment account) and put at least the minimum monthly amount into it each month. From there, treat it like the money doesn’t exist anymore.

If you need help investing we can open an investment account for you through your membership.

Final Word

Making sure to use an income driven repayment calculator that provides you with the best information is essential. FitBUX’s calculator does just that.

Also, you can speak to a student loan expert once you become a member of FitBUX.

We look forward to chatting with you soon.