In 2008, more than 3.1 million foreclosures were issued. That means one in fifty-four households.

Each of those households had qualified for a mortgage. However, how much house you can afford can be very different from what you qualify for.

….and the cycle continues.

More than 300,000 people search ‘how much house can I afford’ each month. The results that appear sadly don’t reflect how much house you can afford. Instead, they calculate how much of a mortgage you qualify for.

Buying a house solely based on how much you qualify for is common. Its also a monumental financial mistake.

I’m going to dive deeper into how much home you can afford so you can avoid this mistake.

However, before doing so I want to illustrate how following a well-built financial plan can save you millions in the long run. Especially, when it comes to buying a home.

A $2.2 Million Difference

Here is a real-life example from a FitBUX Member.

Mary is using an income-driven repayment plan as part of her student loan strategy. IDR plans allow you to reduce your required monthly payment when compared to a traditional loan repayment strategy.

The mistake many young professionals make is that they use the money they save from the lower monthly payment to take on additional forms of debt. Also, going on IDR allows you to take on more debt relative to a regular repayment plan.

How is that possible?

The lower monthly payments on IDR reduces your debt-to-income ratio, all else equal. In turn, you qualify for more debt. This can be great if handled correctly. It is a massive issue if not handled correctly.

Mary managed to qualify for a mortgage despite her significant amount of student loans.

Once she qualified for a mortgage, Mary used FitBUX’s home buying technology to determine how much home she could truly afford.

Mary could only afford about half of what she was qualified for. This was bad news for Mary because nothing in her area was priced in a range that she could afford.

She then used FitBUX’s financial planning technology to compare different financial plans and explore how to improve her situation.

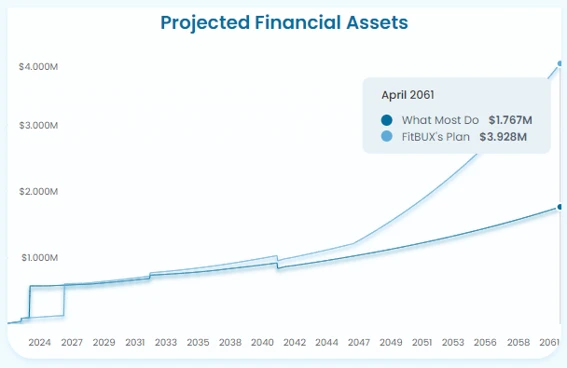

Mary’s First Financial Plan

In her first financial plan, she would purchase a home using mortgage she qualified for.

At retirement time in 2061 (her target date) she would have a total net wealth of $1.7 million.

She thought that was a good plan. Just to make sure though, she scheduled a call with her FitBUX Coach.

This helped her realize that:

- If she went through with the home purchase, she would virtually live paycheck to paycheck. Therefore, her financial stress would be high.

- Yes, she would have $1.7 million in net worth at retirement. However, only $500k of it was liquid assets. She would be house rich, cash poor.

- The $1.7 million net worth is in 2061 dollars. This is equivalent to $776k in today’s money. The $500k of liquid assets in 2061 is equivalent to only $230k in today’s money!

Mary’s Second Plan

Mary’s FitBUX Coach helped her build a second plan.

In this plan she would postpone buying the house for four years. In addition, she would aggressively pay off her car loan before buying the house.

The result is she:

- Would be able to afford more home in four years;

- Didn’t have to live paycheck to paycheck thanks to her lower debt load; and

- Be able to invest more.

The long-term impact would be:

- A net wealth by 2061 of $3.95 million.

- A better balance between liquid assets and real estate assets since she could invest more.

That is a $2.2 million increase relative to what she was going implement with her initial plan! This is the mistake hundreds of thousands of other young professionals are making!

Home Qualification vs Home Affordability: The Key Difference

The key difference between home affordability and home qualification is one of perspective. Let’s use an hypothetical example.

Let’s say you recently moved and are looking for people to be friends with. You meet someone at a local event. The first thing they say is, “We should be friends! However, to be friends you have to do my laundry, cut my grass, and pay for my dinner once a week.”

You then ask, “What is in it for me?”

The person responds, “My friendship!”

Would you be friends with this person? Probably not because the benefit of that relationship tremendously favors one person.

Home qualification works the same way. It is a set of standards used by lenders to determine risk.

This means when you qualify for a loan the lender is judging the odds that you will pay them back. If you don’t pay them back, how likely it is that they can get their money back through foreclosure.

In short, home qualification is determined from the view point of the lender and the point of view of the lender ONLY. The lender is saying that if you fit into what I’m looking for, then we can be friends.

Home affordability on the other hand looks at home buying from a financial planning point of view. The question you have to answer is, “Does that fit into my life and what I am looking for?”

I dive more into home affordability below but to summarize, you should treat getting a mortgage more like a mutual friendship instead of a one sided relationship.

Factors That Go Into Home Affordability

Home affordability looks at today and tomorrow.

Today

Below is a list of factors that go into your affordability today:

- Lenders look at three primary items to determine mortgage qualifications: Credit score, debt-to-income ratio, and loan to value. The only one that factors into affordability is debt to income. The other two you can ignore.

- Debt to income is a good starting point but its limited. You must factor in other items such as

- Child expenses;

- Your day-to-day expenses such as food and gas; and

- Insurance premiums you pay such as health care and life insurance.

- The largest item we see new grads ignore but is extremely important to home affordability applies to those on income-driven repayment plans. They forget to factor in two items:

- Saving for the tax liability; and

- They only look at the monthly payment on their student loans now. As your income increases so will your monthly payment.

This is huge! Most people only look at income to help determine their debt-to-income ratio. However, you have to look at the characteristics of your income.

For example, someone that has salaried income in a profession with low unemployment can afford more than someone with commission income in an unstable industry such as a real estate agent.

Tomorrow

Below are the items you need to look at to determine home affordability in the future:

- Home upkeep is by far the biggest item young professionals under estimate. Homes are expensive.

- Future family situation, i.e. kids. Will you or your spouse stay home, reduce work hours, etc?

- How soon will you be paying off other debt?

- What other debt will you need such as buying a car?

- Will you be inheriting money?

One Thing That Isn’t A Factor

I often hear young professionals say they are buying a house because their rent is really expensive. Home affordability ignores rent. Thus, your current rent doesn’t change what you can afford or not.

What you are actually looking to decide in this situation is if you should rent vs buy.

The truth is, both buying and renting maybe unaffordable based on your income and location. Therefore, from a financial perspective I recommend moving to a place that is more affordable.

For those of you saying you can’t move, you are correct. You can’t and shouldn’t look into it. Others of you that can, if you live in an unaffordable place then its worth it to take a look elsewhere.

Red Flags On Things You Read Or Hear

Red Flags On Things You Read Or Hear

Almost all the content that is found on the internet, podcast, or things you hear from mortgage lenders centers on home qualification not home affordability.

Below are some red flag examples. If you see this type of language from others, be aware. They are talking about qualifications not affordability!

Note before going into the red flags. I personally don’t like lenders and am very picky who I use. I take this same approach with FitBUX members. Therefore, I’ve found and worked with two lenders throughout the years that are really good. Be sure to check them out once you start the home buying process: Neo Home Loans and Movement Mortgage.

Red Flag #1

What is your credit score? Credit scores were designed to measure fraud risk. They tell you nothing from a financial planning point of view. In fact, I know people that have 750s and 800s and they can’t afford to buy anything!

Red Flag #2

The next example is one of my favorites. I type in How Much Home Can I Afford into Google. Click one of the articles and the first line says, “When banks evaluate your affordability….”

They are literally telling you that everything you are about to read is from a banks perspective. Why the heck would you care what a bank is telling me you can afford. They aren’t there to determine that.

Yes, there are regulations saying banks and lenders have to look at affordability. However, the truth of the matter is that most of those laws are crap. In fact, many of those laws put people in homes they can’t afford.

Red Flag #3

Another article that made me laugh. The title is “Home affordability begins with your mortgage rate.” Que the face palm. This article is obviously written for search engine optimization with the goal of you using their market place to shop interest rates.

There are a number of quantitative factors to start with but I’d actually start with the qualitative factors. That is, what are the pros and cons of owning a house?

Red Flag #4

Speaking of face palms, this article I did a double face palm!

One of the sub-titles says, “How does your debt-to-income ratio impact affordability.”

Then the first sentence says, “An important metric that your bank uses to calculate the amount of money you can borrow is the DTI ratio.”

This isn’t bad. As I mentioned earlier in the article, the debt-to-income ratio is the only ratio the bank uses that factors into your ability to own a house.

The face palm comes from the section of that article that comes next…

“Loans backed by the FHA have more relaxed qualifying standards.”

This article was supposed to be about home affordability. However, they are literally saying with an FHA loan, you can qualify because of relaxed standards.

News flash. If you can truly afford a house, you don’t need relaxed qualifying standards!

This is one of those laws I told you about doing more harm than good. In fact, a majority of people that I’ve meet that have used FHA loans can not afford a house and should not have bought.

Red Flag #5

One last example is the popular 28%/36% rule.

This rule says you shouldn’t spend more than 28% of your gross monthly income on home related costs and 36% on total debts.

Rules like this are well intentioned but they ignore all the factors we discussed earlier that go into figuring out if you can afford a home or not.

Focusing On Qualifying Can Cost You A Lot

We’ve already seen how you can buy too much house if only focusing on qualifying for a mortgage. However, there is another way it can cost you.

When a lender tells people how much they qualify for, they often include the amount and interest rate. People think that is it, i.e. that is what they get.

People don’t realize they can get a lower interest rate by buying points. Buying points can make the home more affordable and you don’t always have to pay them out of pocket. You may also use seller concessions to buy points.

You should work with a good lender and use a mortgage point calculator to determine if they can make home buying more affordable.

How To Calculate How Much Home You Can Afford

There are literally hundreds if not thousands of factors that go into this calculation.

Even worse, if you search “how much home can I afford”, every search result discusses how much you qualify for.

Therefore, FitBUX decided to do something about it and make this easy for you.

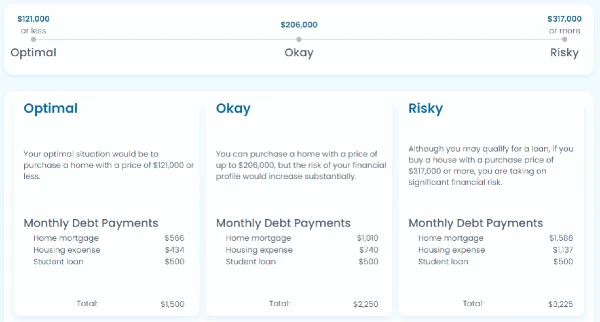

As part of our premium membership, we have a home affordability calculator that is customized to you. Simply make sure your FitBUX profile is up-to-date, click a button and we will show you the optimal purchase price, an OK price, and a Risky purchase price.

You can also include a home purchase in our financial planning technology. Therefore, you can visualize the impact of various home prices on your entire financial plan.

To get started, sign-up, build your profile, and go from there.

By Joseph Reinke, CFA