A home equity line of credit (HELOC for short), is often times confused with a home equity loan. However, the two are completely different.

If you own a home, having a home equity line of credit should definitely be part of your financial profile. Having one drastically reduces the risk of your financial plan.

Understanding this financial product is key to using them. Below I detail the important details you need to know about home equity lines of credit. I also illustrate how to use them appropriately.

NOTE: HELOCs should be part of your financial profile if you own a home and have equity. However, just like any financial product, misuse of the HELOC can put you in a bad situation. Therefore, educate yourself as much as possible. If you have questions, use your free FitBUX membership and speak with a FitBUX Coach.

What A HELOC Is & What Its Not

As I mentioned above, a home equity line of credit is not the same as a home equity loan. The key difference is a HELOC is a revolving source of money.

In short, it works the same as a credit card. This has huge implications on your credit report as well as the cost relative to a loan. I discuss this more in detail below. However, before doing so I’ll provide you with more HELOC details.

Banks provide a number of different ways to access the money. For example, you can:

- Do an online transfer to your other accounts;

- Write a check; and

- Use a credit card connected to your account.

In addition, home equity lines of credit have low or no fees to open.

In regards to interest rates, most are variable interest. However, more and more banks/lenders are offering fixed rate HELOCs.

That is one of the reason why we’ve partnered with Neo Home Loans and Movement Mortgage. They both offer fixed rate loans which I personally tend to gravitate towards because they are less risky.

Why Have A Home Equity Line Of Credit

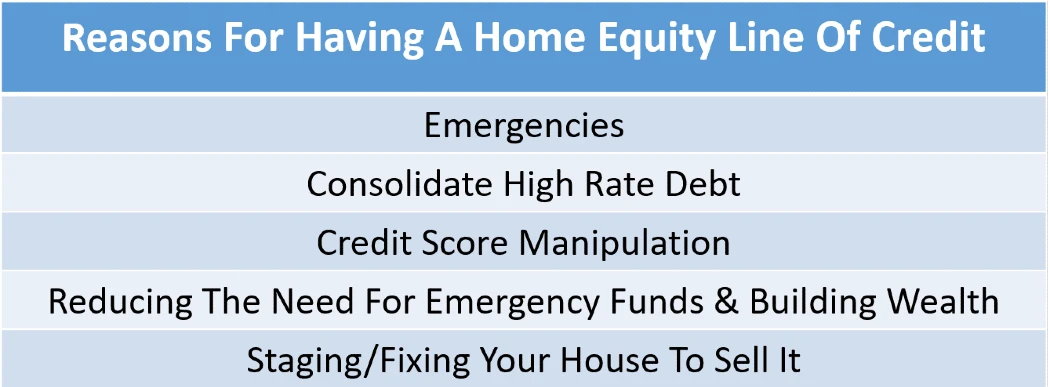

There are two primary financial planning reasons to have a HELOC and three secondary reasons.

Primary Reasons For Having A HELOC

The two primary reasons are:

- Emergencies; and

- Consolidation of high rate debt.

Like the saying goes, shit happens. For example, your house can burn down. If this happens you can’t get a loan against your house anymore because your house doesn’t exists.

Another common emergency is losing a job or a disability. Both of these situations may cause you to lose your income.

At that point you can’t qualify for a mortgage. Therefore, I’ve seen a lot of people panic. Then they ‘fire’ sell their homes so they can get the equity from it. When that happens you may not get the most value from your home.

However, you don’t have to panic if you have a line of credit. You can draw against it and take time to sell your house!

You may also have high interest rate debt such as credit cards. HELOCs have lower rates because they are backed against the equity in your house.

Also, you may have a previous loan at a high fixed rate and rates have dropped.

For example, you may have a car loan with a 7% interest rate. However, the current rate on your HELOC may be 3.5%. You could refinance your car loan but might have to pay fees. With the HELOC you simply draw against it and pay off your car loan.

Secondary Reasons For Having A HELOC

The three secondary financial planning reasons are:

- Credit score manipulation;

- Reducing the need for an emergency fund; and

- Staging/fixing your house to sell it.

I discuss credit score manipulation later in this article.

You can also use a home equity line of credit to build wealth. This is the case because having one reduces the need for an emergency fund.

You may be selling your house. There are a number of statistics that show staging a house will get you a higher sell price.

Maybe you do an analysis and realize that new paint will get you more money. Or maybe updating a bathroom will get you a higher sell price.

There are a number of ways to increase the value of your house prior to selling it. You can use cash for this but many opt to use a line of credit instead.

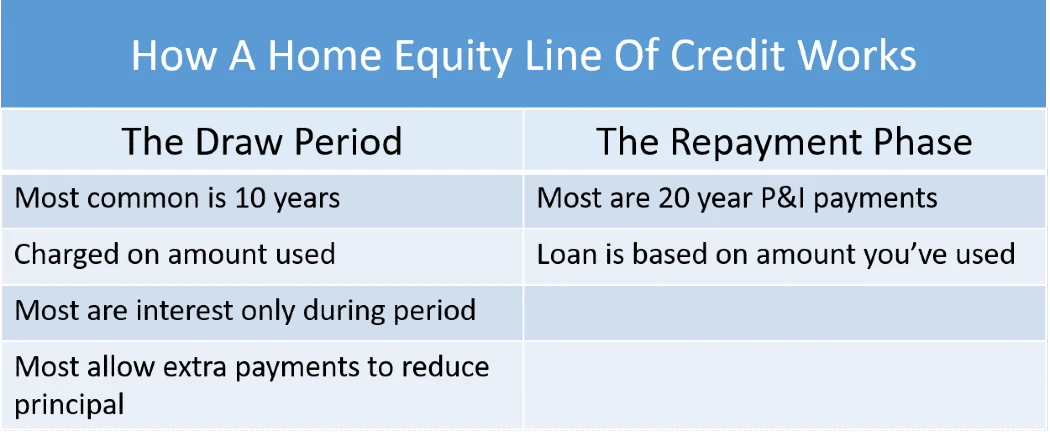

How A Home Equity Line Of Credit Works

Most of the time a home equity line of credit has two phases.

The Draw Period

The first phase is called the draw period.

- The most common draw period is ten years.

- During the draw period, you can borrow against you HELOC at any time. Any money you don’t take is not charged interest similar to a credit card. For example, if you have a $50,000 home equity line of credit but have not used it, i.e. the balance you owe is $0, then you are not charged anything.

- During the draw period, most HELOC payments are interest only. For example, if I’ve drawn $10,000 on my line of credit and have a 6% interest rate, then my monthly payment would be $50

- Most banks allow you to make extra payments during the draw period that are used to reduce principal.

The Repayment Phase

After the draw period ends you can take one of two actions. If your bank allows it, you can extend the draw period.

If your bank doesn’t allow you to extend the draw period or you don’t want to then you enter the repayment phase.

There are a number of repayment options. However, the most common is a standard 20 year principal and interest loan.

This means whatever you have outstanding on the home equity line of credit must be repaid over 20 years. Of course you can make prepayments and pay it off sooner if you’d like.

An example of the repayment phase would be something like the following.

You have a $50,000 home equity line of credit. It has a 6% interest rate and you only used $20,000 of it.

Therefore, once it enters the repayment phase, you would have a $20,000 principal and interest loan at 6%. The loan is then paid over 20 years. In addition, you would no longer be able to access the additional $30,000 of credit.

If you do not know what I’m referring to in regards to principal and interest payments, then check out the video below.

Why Knowing It’s Like A Credit Card Is Important

Using a home equity line of credit properly is great for reducing risk in your financial plan. However, you must understand why it being treated like a credit card is so important.

The credit utilization ratio is one of the biggest factors in the computation of your credit score. For example, if you have $10,000 of credit available to you via credit card and have $1,000 used. Your credit utilization ratio is 10%.

Therefore, if I have a $50,000 home equity line of credit but have nothing drawn it looks like an unused $50,000 credit card. The credit scoring companies like this and your credit score will shoot up all else equal.

In fact, this is one way I’ve manipulated my credit score up to an 835. I have a home equity line of credit that I’ve never used.

But there is also a flip side to this. Once you get above a 5% utilization ratio, your credit score starts to go down. Once you hit 20% your credit score goes down a lot!

We saw this play out in the mortgage crisis of 2008. People were buying housing with 100% financing.

However, they weren’t using 100% equity loans. Often times 90% would be a loan. The other 10% of the purchase price would be a home equity line of credit.

In short, their credit utilization on the line of credit was 100%. Therefore, their credit scores tanked. This is one reason why many people were unable to refinance which added fuel to the mortgage crisis fire.

Frequently Asked HELOC Questions

How much can I take out?

This varies by lender but the absolute max you can take out is the equity you have in your house. For example, if your house is worth $500,000 and your mortgage balance is $400,000 then the largest HELOC you can have is $100,000. However, most lenders will only give you a fraction of that based on combined loan-to-value (CLTV). If the max CLTV is 90% then using the example above you could have a HELOC of $50,000.

What is the purpose of a home equity line of credit?

The primary reasons are: 1. To reduce the risk to your financial plan; 2. Reduce high interest rate debt; and 3. Strategically building your net wealth.

Do you have to pay back a home equity line of credit?

If you still own the property yes. There are two ways not to ‘repay it.’ 1) Get a home equity loan and use the proceeds to pay off the HELOC; and 2) Sell the home and use the proceeds to pay off the HELOC.

What is the difference between a home equity loan and home equity line of credit?

Home equity loans cost more in regards to fees when you get one and they are reported on your credit report as an installment loan. Home equity lines of credit are cheaper, easier to qualify for, and are reported on your credit report as a revolving line of credit, i.e. they are treated like a credit card.

Can you pull equity out of your home without refinancing?

Yes, via a home equity line of credit. They are easier to qualify for relative to refinancing and are cheaper.

Does a HELOC affect your credit score?

Yes. Depending on how you use it and how much you have available will primarily affect your credit utilization ratio. This can positively or negatively impact your credit score.

What happens if I don't use my HELOC?

Nothing. You aren’t charged any interest. However, its good to have because it reduces the risk to your financial plan.

Can you walk away from a home equity line of credit?

Yes, you can tell the bank you don’t want it anymore. Whatever is outstanding would then have to be repaid.

How much equity can you borrow from your home?

Most banks will allow you to have a combined loan to value ratio of 90%. This means if your home is worth $500,000, the most you can have outstanding between home equity loans and home equity lines of credit is $450,000.

How long is a home equity line of credit good for?

The typical draw period on a home equity line of credit is 10 years with a 20 year repayment term thereafter.

Do I need an appraisal for a HELOC?

What credit score do I need to qualify for a HELOC?

Every lender is different. However, FitBUX’s partners will go as low as a 640 for owner occupied homes. For investment homes they will go as low as 680.

What do I need for a home equity line of credit?

All are difference but here is one example from one of our lending partners: • FICO of 640+ • Min loan amount of $15k • Home must have been bought 90+ days prior • Max debt-to-income ratio of 50% • Max combined loan-to-value ratio between 70% and 90%

By Joseph Reinke, CFA