Young adults are being advised that higher education is a must for their futures. Statistics show this advice is indisputable. However, there is good debt vs bad debt. What young adults should be told is, “Just because the government is willing to write someone a blank check to attend college (specifically graduate programs) does not mean one should take the money.” Not heeding this advice can set you back financially for a long time, if not for the remainder of your life. In short, not all debt is created equal. This article…

- Going To School & Building Your Greatest Asset

- Student Loan Debt Versus Home Loans

- The Student Loan Ratio You Need To Know

- What Traditional School ROI Calculators Miss

Going To School & Building Your Greatest Asset

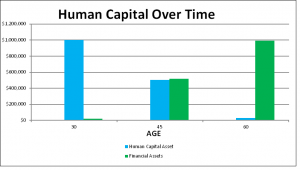

When we think of assets we think of tangible and financial assets. Financial assets are things such as a home, stocks, bonds, autos, etc… However, there is another type of asset that an individual possesses. In finance, we call this your human capital asset. At a high level, your future income and the risk to that income has a value today. That value is your human capital asset. Financial theory says that a young person’s number one asset is their human capital. The reason is young individuals have not had time to build financial assets. Over time, you will translate your human capital into financial capital through the receipt of pay checks, saving a portion of those pay checks, and investing those savings. In essence, over time our human capital asset decreases and should be used to increase our financial assets.  One of the determinants of our human capital is the level of education we obtain. All else equal, the higher the level of education we have, the greater our future income should be. Also, the more education we obtain, our income should have less risk (less risk do to unemployment, Greater future income and lower risk increases the value of our human capital today. Remember though, this assumes all else is equal. This assumption is important, and we will touch on why later in the article but first we will explain why student loan debt is not equal to other forms of debt. Human capital is so important that some student loan refinance companies have begun to use it to qualify you for refinancing. (Learn more about student loan refinancing by clicking here).

One of the determinants of our human capital is the level of education we obtain. All else equal, the higher the level of education we have, the greater our future income should be. Also, the more education we obtain, our income should have less risk (less risk do to unemployment, Greater future income and lower risk increases the value of our human capital today. Remember though, this assumes all else is equal. This assumption is important, and we will touch on why later in the article but first we will explain why student loan debt is not equal to other forms of debt. Human capital is so important that some student loan refinance companies have begun to use it to qualify you for refinancing. (Learn more about student loan refinancing by clicking here).

Student Loans Versus Home Loans

I’ve had students ask me, “Why are you saying I can’t afford $200,000 in students loans but the bank says I can use $200,000 in loans to buy a house?” I will use the example below to illustrate good debt vs bad debt. You have a limited amount of time to convert human capital to financial assets. For example, if you are 30 years old when you graduate and plan on retiring at 60, you only have 30 years to convert your human capital to financial assets. Using your human capital to pay off student loans is much different than using it to pay for a home loan. For example, let’s assume you recently obtained a graduate degree, receive a salary of $80,000, and have a student loan balance of $200,000. For illustration purposes only, lets say the student loan is expected to be paid off over 30 years. Thus, as you recognize your human capital asset in the form of wages, you will use it to pay off your student loans. After 30 years you are debt-free, but you also have not accumulated financial assets. Now compare that to a home loan. Assume you graduated with no student loans and bought a house with a $200,000 home loan and a 30 year term. Over time, when you recognize your human capital asset in the form of wages you are using those wages to pay off the home loan. At the end of 30 years, you would have no more debt, but you would also have a financial asset…your house. The moral of this story is just because an entity is willing to give you a blank check to go to school, that does not mean to go to school at any cost. There is a tipping point whereby the increase in human capital you receive from furthering your education is negated by how much you borrow. In essence, do not borrow blindly.

The Student Debt Ratio You Need To Know

You want your education to be a good investment. To make sure your student loans are “good debt” we use a general guideline of a 1:1 ratio. This means that your total loans should be less than or equal to your expected annual gross earnings upon graduation. For example, if you expect to make $80,000 per year, your student loans should be less than or equal to $80,000 once you graduate. When you go above that ratio, you run the risk of not having the ability to turn your human capital asset into enough financial assets in the future. This makes your education “not worth it” from a financial perspective. Many of you are probably thinking, “There is no way I can complete my studies and meet that ratio.” As harsh as it sounds, you should do everything you can do so. This could mean working part-time or full-time during your studies. It also means trying to get grants and scholarships. You may have to sacrifice “having a life” while in school but the sacrifice you make will be well worth it in the long run. You may even decide not to go to school! Deciding how much in student loans you should use for education is a hard question to answer. To make the decision making process even more challenging, many of the “helpful” tools available today may not be as valuable as they seem…

What Traditional School ROI Calculators Miss

Individuals contemplating an advanced degree will often times turn to return on investment (ROI) calculators to determine if getting their advanced degree is “worth it.” However, most of these simple calculators only look at the increase in income one would expect after graduating. Then they compare it to the cost of financing one’s education. By capturing the increase in one’s expected income, these calculators are capturing the increase in one’s human capital value. However, these calculators do not capture the decrease in risk with that expected earnings increase. They assume that the additional cash flows from obtaining higher education have no risk. This is not true. Thus, they paint an incomplete (and often inaccurate) picture of one’s overall future situation. For instance, many who pursue an advanced degree may be doing so to change industries. However, the new industry may be more susceptible to contractions during economic downturns, which increases the risk to one’s future cash flows. This risk is not captured by using simple averages of graduates. In addition, these calculators do not capture the risk of adding a fixed cost (your loan payments) to your financial outlook. They also don’t take into account other factors about your personal financial situation. These factors may include things like other debts such as a mortgage, an auto loan, or undergraduate student loans. Other factors also include things such as how stable your spouse’s job may be, how many children you have, or other expenses you might incur. In addition, there are many different factors that reduce or increase the risk to your “employability.” For example, hiring managers of MBA candidates have said they look for candidates who had 3 to 6 years of work experience before entering their MBA program. Therefore, the expected inrease in earnings post MBA may be more difficult for some graduates to obtain. Most of these factors are simply ignored by traditional ROI calculators.

OK, So Now What? Help Us, Help You! (Really)

All of the above are reasons why FitBUX is building a holistic financial engine that encompasses all of the factors discussed above. Our Tools answer questions like: “If I pursue an advanced degree, what effect does the amount of student loans I expect to take out have on my personal situation, taking my past, present, and future into account.” If you would like to get a holistic picture of your personal situation and how FitBUX can help you, sign-up for free. Want to learn more about money? Make sure to check out FitBUX’s finance blog.