Interest rates are going up. People want to buy a house and spend as little as they can. These are the conditions in which we see adjustable rate mortgage usage increase.

Therefore, we’d expect to see an increase in the usage of adjustable rate mortgages. Guess what! We have.

In 2020, adjustable rate mortgages made up on 3% of all loans. Last month, they made up 10%.

Adjustable rate mortgages are often blamed for the 2007 housing crisis. Therefore, the headlines have been asking if we are going to experience another crisis because of these mortgages.

As of now, the answer is no. As I mentioned above, adjustable rate mortgages are 10% of loans right now. In 2005 they were 35%!

The big question FitBUX members are asking right now is if they should use an adjustable rate mortgage to buy a house right now.

Below I detail what an adjustable rate mortgage is, when to use one, and when not to.

You can also download the podcast below:

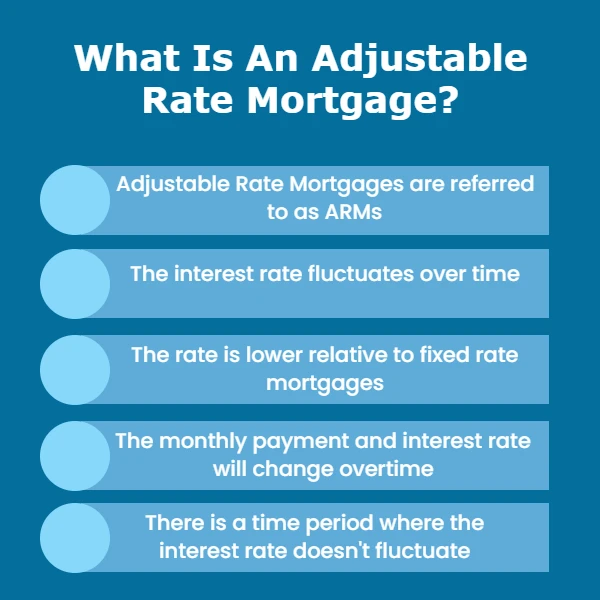

What Is An Adjustable Rate Mortgage?

- Adjustable rate mortgages are often referred to as ARMs.

- The key thing that makes them different than fixed-rate mortgages is the interest rate fluctuates.

- If you compare current rates between adjustable rate and fixed rate mortgages, adjustable rates are lower. This is what entices people to use them. Savvy borrowers however will use fixed rate loans and buy points to get a lower interest rate.

- The interest rate will change over time. Therefore, your monthly payment on an adjustable rate mortgage will fluctuate.

- Typically, the rate on the adjustable rate mortgage stays fixed for a given amount of time before adjusting. Below I will detail key terms of ARMs and the different types.

Key ARM Terms To Know

One big problem on adjustable rate mortgages is misinformation and a lack of understanding. For example, this article by one of the largest finance blogs is just flat out wrong.

They state, “The interest rate on an ARM is set below market rate on a comparable fixed-rate loan, and then the rate rises as time goes on. If the ARM is held long enough, the interest rate will surpass the going rate for fixed-rate loans.”

There are multiple items that are completely misguiding in the above quote. Below are the key terms that you need to know. You’ll see why the above quote is wrong.

Adjustment Frequency

After the fixed rate period ends, the interest rate will adjust. Typically this is monthly or yearly. For example, if you have a 3% interest rate now with a monthly adjustment. The next month your interest rate could go up to 3.25% or go down to 2.75%.

That is the one big fallacy of the quote above. ARM interest rates don’t always go up. They can go down!

Adjustment Index & Spread

This is a MUST KNOW if you are using an adjustable rate mortgage.

The interest rate isn’t randomly selected. It is tied to a benchmark. The most popular benchmarks are indexes. The most often used are the Secured Overnight Financing Rate (SOFR) or the London Interbank Offered Rate (LIBOR).

From there, the lender will add a ‘spread’ over the index. A spread is an amount over the index.

For example, the adjustable rate mortgage may be using LIBOR as a benchmark plus 3%. This means if LIBOR is 2% then the lender will add 3% to it. Therefore, your interest rate for that period is 5%.

You’ll also want to know the specific index. For example, LIBOR has 1 month rates, 3 months rates, 6 month rates, etc…

Usually the index is linked to the adjustment frequency. For example, if your adjustment frequency is monthly then the index used would be the LIBOR 1 month rate.

This makes a MASSIVE DIFFERENCE in your rate. For example, the one month LIBOR rate right now is 2.68%. The six month LIBOR rate is 3.70%!

Margin

Above I detailed the ‘spread’ above the index. Spread is also referred to as margin. Therefore, if you see the word margin when you are reviewing your adjustable rate mortgage docs, it’s the same thing as the spread.

Caps

This is another vital piece of information to know about adjustable rate mortgages.

As you now know, interest rates on adjustable rate mortgages have an adjustment frequency, i.e. monthly, yearly, etc. The interest rate can only adjust a certain amount at each adjustment period. This is called a cap.

For example, let’s say your current rate is 3% and you have an 1% cap. Fast forward one year and the index plus the spread/margin is 5.5%. This rate is above your current rate plus the cap. Therefore, your interest rate would be 4% not 5.5%.

Types Of Adjustable Rate Mortgages

There are two primary components of adjustable rate mortgages you need to be familiar with. The fixed period and if its an interest only mortgage or principal and interest mortgage.

Fixed Period

The most common fixed periods for ARMs are 3, 5, 7, and 10 years.

You’ll see them labeled as 3/1, 5/1, 7/1, and 10/1.

For example, you might hear or read mortgage docs that say you are looking at a 3/1. Therefore, the fixed period is three years, then the interest rate adjustment frequency is every year thereafter.

Typically the length of an adjustable rate mortgage is 30 years. Thus, in the example above you’d have a fixed rate for three years. Then the rate would adjust annually for the next 27 years.

The shorter the fixed period, the lower the fixed period interest rate will be.

Interest Only Or Principal & Interest

Most adjustable rate mortgages are interest only for a certain period of time. Then they convert to a principal and interest mortgage thereafter.

For example, you may be looking at a 3/1 whereby the first three years are interest only payments. After year three, your rate goes adjustable and it turns into a principal and interest payment.

One key. The fixed period and the interest only period do not have to be the same!

For example, you can have a 3/1 adjustable rate mortgage that is interest only for the first 10 years. For example, the rate is adjustable after the third year. However, your payment is still interest only for another 7 years.

When To Use An ARM & When Not To

Adjustable rate mortgages got a very bad rap because of the 2007 housing crisis. However, most financial products have a purpose.

Therefore, if you use the product for that purpose there is nothing wrong with them. Its when a product is misused that causes the problem.

Below I detail when you would want to use an adjustable rate mortgage vs when you’d want to avoid them.

When To Use An Adjustable Rate Mortgage

- If interest rates are high AND you believe rates are going to be staying flat or going down.

- You expect to sell the property before the fixed interest rate period is over. For example, if you expect to sell the property within 5 years, you could use a 5/1, 7/1, or a 10/1.

- YOU UNDERSTAND HOW ADJUSTABLE RATE MORTGAGES WORK!

One key to the above. Its not good enough to just have one of these boxes checked off. For example, if you think interest rates are high and are going to decrease, you wouldn’t want to use an adjustable rate mortgage just because of that. Reason being is that you could just refinance a fixed rate mortgage if the interest rates did indeed go down.

I highly recommend if you are going to use an ARM, that you believe rates are going down, you plan on selling the property before the fixed rate period is over, and you understand them!

Also, I like to be more cautious. If you plan on selling the property in 5 years, I would still recommend using a 7/1 or a 10/1. This gives you more time just in case something doesn’t go as planned.

If you do use an adjustable rate mortgage, I recommend using FitBUX’s partner Neo Home Loans. Check them out by clicking the banner below.

When Not To Use An Adjustable Rate Mortgage

- Interest rates are low. This is one of the biggest mistakes I saw over the past 10 years, i.e. people using an ARM when fixed rates were low. Now they want to refinance and all the rates have risen dramatically. They should’ve locked in the low fixed rate.

- You plan on holding the property long-term. This is especially true if this is going to be your primary residence. The only time this isn’t true is if you plan on paying off the entire mortgage before the fixed period is over.

- Although you are reading this awesome article, you still are confused with how adjustable rate mortgages work. If you don’t understand it, keep life simple and don’t’ use them.

- If you do understand them, but like to have the certainty for financial planning purposes.

I typically advise against adjustable rate mortgages for most people because of #4 above. Knowing exactly what your interest rate and payment is going to be makes planning a lot easier. It also makes managing your money a lot easier.

One Big Mistake Too Avoid

I see people make this mistake constantly. In fact, its not just with mortgages but student loans as well. I’ll tell you the story of Bill to illustrate this mistake.

Bill wanted to buy a house and liked the adjustable rate mortgage because of the low rate and low payment. He’s young so he’s never really experienced normalized interest rates. By this I mean his experience with interest rates has always been in a low interest rate environment.

Although he was offered a low 3.5% fixed mortgage, he opted to use a 2.75% adjustable rate mortgage. Why? Because it was a lower interest rate and he could better afford the payment.

This was a mistake. However, the bigger mistake is what I see happen ALL THE TIME.

Bill’s loan came out of the fixed period and he freaked out because of how high his mortgage payment went. His interest rate after a couple of years was now in the 5% range. Again, had he been smart about it, he could have had a fixed rate of 3.5%.

Here is where the irrational part comes in. He calls me up and says he never wants an adjustable rate mortgage again and that he’s going to get fixed rate loan.

A few months go by before I speak to him again. What did he do? He got another adjustable rate mortgage!

I asked him why. His reasoning, “The fixed rate was 6% and the ARM rate was 5% so it was more affordable.”

Palm to face…. You just made the same mistake as before! I believe that is the definition of insanity.

An Alternative To ARMs Many Don’t Know About

I don’t personally use adjustable rate mortgages because I like certainty. However, that doesn’t mean I always use principal and interest loans.

There is another option that a lot of mortgage brokers and lenders get confused about. It is the 30 year interest only loan.

These are typically interest only for 10 years then convert to a 20 year principal and interest loan. However, the RATE STAYS THE SAME FOR ALL 30 YEARS.

Why Is The Interest Rate On An ARM Lower Than A Fixed Rate Mortgage?

Finance and investments is all about risk and return.

Lenders have a problem. They borrow money short-term but then lend it to you and I long-term. That is a lot of risk the lender is taking.

Therefore, they have to buy finance products to help reduce the risk. However, the more financial products they have to buy the more expensive the loan becomes.

Thus, the fixed interest rate on a mortgage encompasses risk and these costs.

Adjustable rate mortgages also solve this problem for lenders. The interest rate on the mortgage will adjust frequently and reflect current borrowing rates for the lender.

Therefore, the bank has lower risk and can charge lower interest rates.

In short, they can lower the interest rate because you are now taking on the risk!

Rapid Fire FAQ

How does an adjustable mortgage rate work?

There is a fixed period. Then after the fixed period the interest rate adjust up and down monthly, quarterly, annually, etc. Sometimes, there are interest only payments as well.

What is the danger of an ARM?

The primary danger of the ARM is that rates go up. Your monthly payment can become very costly. The secondary danger is you don’t understand them and misuse them. Therefore, putting yourself in a poor situation.

What happens at the end of an ARM Mortgage?

Your mortgage is paid off and you owe nothing just like a fixed mortgage.

Can you pay off an adjustable rate mortgage early?

Most allow you to pay them off early. However, some have prepayments if you pay off over a certain amount before an agreed upon date.

Who is a good candidate for an adjustable rate mortgage?

If you think you will sell the property before the mortgage rate begins to adjust. The other scenario you’d use an ARM for is if you’ll pay off the mortgage before the rate adjust.

What are the disadvantages of an ARM mortgage?

They are complex and since the rate changes, its hard to build a financial plan when using one.

Can you refinance from an ARM to Fixed Rate mortgage?

Yes you can if you have enough equity in your house. In 2008, people tried to refinance but housing prices decreased. Therefore, they couldn’t refinance and got foreclosed on because they couldn’t afford the higher payments.

Can I pay points on an adjustable rate mortgage?

Yes you can. However, the benefits of points is often from long-term savings. Therefore, if you use an ARM most of the time you wouldn't use points.

By Joseph Reinke, CFA